Business

What Is Mortgage Refinancing? A Florida Guide

Mortgage refinancing is defined as replacing your existing home loan with a new mortgage that carries different terms, a lower interest rate, or access to your home’s equity. For Florida homeowners, this single financial move can reduce monthly payments by hundreds of dollars, eliminate years from a loan term, or unlock tens of thousands in equity for renovations or debt payoff. The process works the same way as your original mortgage application: you apply, qualify, and close on a new loan that pays off the old one. Understanding how it works, what it costs, and when it makes sense puts you in control of one of the largest financial decisions you will make as a homeowner.

Why do homeowners in Florida refinance their mortgage?

The motivations behind refinancing are specific and financial, not vague or aspirational. Florida homeowners refinance for five core reasons, and knowing which one applies to you determines which loan product you should pursue.

- Lower monthly payments. Securing a lower interest rate directly reduces what you owe each month, freeing up cash for other priorities. A homeowner with a $350,000 loan at 7.5% who refinances to 6.25% saves roughly $280 per month. That is $3,360 per year back in your pocket.

- Reduce total interest cost. A lower rate means less interest paid over the life of the loan. On a 30-year mortgage, even a 1% rate reduction can save over $60,000 in total interest. This is the benefit most borrowers underestimate.

- Shorten the loan term. Refinancing from a 30-year to a 15-year mortgage increases your monthly payment slightly but cuts your total interest cost dramatically. Many Florida homeowners approaching retirement use this strategy to own their home outright sooner.

- Switch from an adjustable-rate to a fixed-rate mortgage. Switching from ARM to fixed rate locks in stable monthly payments and protects you from future rate increases. In a volatile rate environment, this stability has real financial value.

- Access home equity through a cash-out refinance. Cash-out refinance lets you borrow against your home's equity at mortgage rates, which are typically far lower than credit card or personal loan rates. Florida homeowners commonly use this for hurricane-resistant upgrades, pool installations, or consolidating high-interest debt.

Pro Tip: Before you decide why you want to refinance, write down your specific financial goal. “I want to lower my rate” is not a goal. “I want to reduce my monthly payment by $200 so I can pay off my car loan faster” is a goal. Specificity leads to better loan decisions.

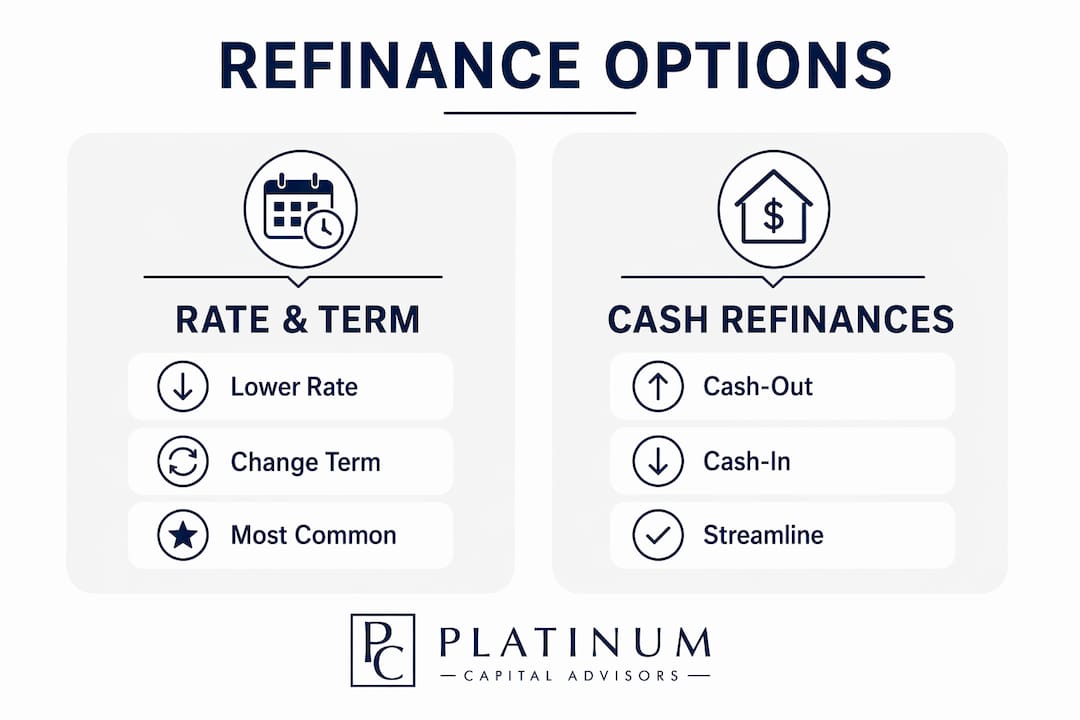

What are the main mortgage refinancing options?

Not every refinance product serves the same purpose. The five primary types differ in structure, qualification requirements, and financial outcome.

Rate-and-term refinance is the most common type. You replace your current loan with a new one at a better rate or different term, without changing the loan balance. This is the go-to option when rates drop significantly below what you currently pay.

Cash-out refinance replaces your mortgage with a larger loan and gives you the difference in cash. If your home is worth $450,000 and you owe $250,000, you may be able to borrow up to $360,000 and receive $110,000 in cash, depending on lender limits. The tradeoff is a higher loan balance and, potentially, a higher monthly payment.

Cash-in refinance works in reverse. You bring cash to closing to pay down the principal, which lowers your loan-to-value ratio and can eliminate private mortgage insurance (PMI). This option suits homeowners who have extra savings and want to qualify for better rates.

Streamline refinance programs through the FHA and VA reduce paperwork and often waive appraisal requirements. Florida veterans and FHA borrowers should evaluate this option first because the qualification bar is lower and the process is faster.

No-closing-cost refinance rolls fees into the loan balance or accepts a slightly higher interest rate in exchange for zero upfront costs. This works well if you plan to sell or refinance again within a few years, but it costs more over the long term.

What does refinancing cost in Florida?

Refinancing closing costs typically range from 2% to 6% of the new loan amount. On a $300,000 loan, that means $6,000 to $18,000 in fees before you see a single dollar of savings. This number surprises most borrowers who focus only on the new interest rate.

Florida adds a few location-specific factors. Documentary stamp taxes on new mortgages, county recording fees, and title insurance rates all vary by county and loan size. Miami-Dade, Broward, and Palm Beach borrowers often see higher title costs than those in smaller markets like Ocala or Pensacola. Costs vary by location and lender, which is why shopping at least three lenders is not optional. It is the only way to know whether the quote in front of you is competitive.

Pro Tip: Request a Loan Estimate from every lender you contact. Federal law requires lenders to provide this document within three business days of your application. Compare Section A (origination charges) and Section B (services you cannot shop for) line by line across all quotes.

How do you decide if refinancing is worth it?

Refinancing is a math problem that requires you to evaluate all costs and savings together, not just the new monthly payment. Here is the framework Florida homeowners should use before signing anything.

- Calculate your break-even point. Divide your total closing costs by your monthly savings. If closing costs are $6,000 and you save $200 per month, your break-even point is 30 months. You must stay in the home longer than 30 months for refinancing to pay off.

- Check the rate difference. A 1% rate reduction is the common benchmark that makes refinancing worthwhile, though a 0.5% drop can still benefit borrowers with large loan balances or long remaining terms. Run the actual numbers rather than relying on the benchmark alone.

- Consider your remaining loan term. If you have 8 years left on a 30-year mortgage, refinancing into a new 30-year loan restarts the clock and costs you more in total interest, even at a lower rate. A shorter-term refinance may serve you better.

- Evaluate your credit profile. Your credit score directly determines the rate you qualify for. A score of 760 or above typically unlocks the best available rates. A score below 680 may result in a rate that makes refinancing financially neutral or worse.

- Think about total interest cost, not just monthly payments. Smart refinancing focuses on long-term interest cost management, not short-term cash flow relief. A lower monthly payment that extends your loan by 10 years often costs more overall.

“Refinancing only makes sense if you plan to stay in the home past the break-even point. Homeowners who move before that date lose money on the transaction, even if the new rate was genuinely better.”

Avoiding costly financial mistakes in real estate starts with treating every major financial decision as an investment calculation, not an emotional one.

Practical tips to maximize your refinancing outcome

Preparation before you apply determines the rate you receive. These steps give Florida homeowners a measurable advantage.

- Improve your credit score before applying. Credit score improvement several months before applying can lower your rate more than waiting for a minor market rate drop. Pay down revolving balances, dispute errors on your credit report, and avoid opening new accounts for at least six months before you apply.

- Compare multiple lenders, including Florida specialists. National banks, credit unions, and local mortgage brokers all price loans differently. A broker with deep Florida market knowledge often accesses wholesale rates that retail lenders do not offer directly.

- Understand the PMI impact. If your current loan carries private mortgage insurance and your home has appreciated, refinancing may eliminate PMI entirely if your new loan-to-value ratio falls below 80%. That alone can save $100 to $200 per month.

- Watch the timing. Refinancing when rates are falling makes obvious sense, but personal financial timing matters equally. Refinancing during a period of stable income, low debt, and strong credit gives you the best negotiating position with lenders.

- Do not extend your term without a clear reason. Resetting to a 30-year loan when you have 20 years remaining adds 10 years of payments. If your only goal is a lower monthly payment, calculate whether a 20-year refinance achieves the same result at a lower total cost.

Pro Tip: Lock your rate as soon as you receive a competitive offer. Florida’s market moves quickly, and a rate that looks good today may be 0.25% higher by the time your appraisal comes back. Most lenders offer 30 to 60-day rate locks at no additional cost.

Key takeaways

Mortgage refinancing pays off when the math supports it, your credit is strong, and you plan to stay in the home past the break-even point.

Why I think most Florida homeowners refinance at the wrong time

Chuck Barnes here. After working with Florida homeowners across every market cycle, the single most common mistake I see is refinancing reactively instead of strategically. A rate drops in the news, a neighbor mentions they just refinanced, and suddenly everyone is calling their lender without running a single number.

The homeowners who come out ahead treat refinancing like an investment decision. They know their break-even point before they apply. They have spent three to six months improving their credit score. They have compared at least three lenders and read every line of the Loan Estimate. They are not chasing a lower monthly payment. They are reducing their total cost of homeownership.

Florida’s market has specific dynamics worth understanding. Property values in markets like Tampa, Orlando, and Jacksonville have appreciated significantly over the past several years. That appreciation creates real equity, and a cash-out refinance at a reasonable rate can be a smarter move than a personal loan or home equity line of credit for major expenses. But tapping equity carelessly, without a clear repayment plan, turns an asset into a liability. The homeowners I have seen struggle are the ones who treated their home like an ATM rather than a long-term wealth-building tool. Think like an investor. Every refinancing decision should make your balance sheet stronger, not just your monthly cash flow.

— Chuck Barnes

Ready to refinance? Platinumcapitalfinancial can help

Platinumcapitalfinancial specializes in mortgage refinancing for Florida homeowners and buyers across the state. Whether you want to lower your rate, shorten your term, or access your home’s equity, the team at Platinumcapitalfinancial works with multiple lenders to find competitive options tailored to your financial profile and goals.

Florida’s mortgage market moves fast, and having a local broker in your corner means you get access to loan products and wholesale rates that most borrowers never see. Platinumcapitalfinancial handles the comparison shopping, paperwork, and lender negotiations so you can focus on making the right decision, not managing the process. Connect with the team at Platinumcapitalfinancial today to get a personalized refinancing analysis and find out exactly what your numbers look like.

FAQ

What is mortgage refinancing in simple terms?

Mortgage refinancing is the process of replacing your current home loan with a new one, typically to get a lower interest rate, reduce monthly payments, or access your home’s equity. The new loan pays off the old one, and you begin making payments under the new terms.

How much does it cost to refinance a mortgage in Florida?

Refinancing costs typically range from 2% to 6% of the loan amount, covering fees like appraisal, origination, title insurance, and Florida-specific recording charges. On a $300,000 loan, expect to pay between $6,000 and $18,000 at closing.

When is refinancing worth it?

Refinancing is worth it when your new rate is meaningfully lower than your current rate, your closing costs can be recovered within your planned time in the home, and your credit profile qualifies you for competitive terms. A 1% rate reduction is the standard benchmark most lenders and advisors reference.

What is a cash-out refinance?

A cash-out refinance replaces your existing mortgage with a larger loan and gives you the difference in cash, drawn from your home’s equity. Florida homeowners commonly use this for home improvements, debt consolidation, or major expenses at rates lower than credit cards.

How long does the mortgage refinancing process take?

The refinancing process typically takes 30 to 45 days from application to closing, depending on the lender, loan type, and appraisal timeline. Streamline refinance programs for FHA and VA loans can close faster because they often waive the full appraisal requirement.

Recommended

- What is mortgage origination? Florida homebuyer's guide

- What Is Mortgage Lock? a Florida Buyer's Guide

- How to Apply for a Mortgage in Florida: 2026 Guide

- Mortgage term explained: A clear guide for Florida buyers

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)