Business

Fixed Rate Mortgage Explained: Benefits and How It Works

A fixed rate mortgage is a home loan where the interest rate stays the same for the entire life of the loan, giving you a predictable principal and interest payment every month. According to the CFPB, the interest rate on a fixed rate mortgage “will not change,” which separates it from adjustable rate mortgages that can shift up or down over time. That single feature makes it the most popular home loan product in the United States. Federal Reserve Bank of St. Louis data cited by CNBC shows 92% of U.S. mortgages are fixed rate. That number tells you most American homebuyers prioritize payment certainty above all else.

What is a fixed rate mortgage and how does it work?

A fixed rate mortgage locks your interest rate at loan origination. From that point forward, your rate never moves regardless of what the broader market does. Your lender calculates your monthly principal and interest payment using that locked rate and your loan balance, then spreads it across the full loan term through a process called amortization.

Early in the loan, most of each payment covers interest. Over time, the balance shifts and more of each payment reduces the principal. This is standard amortization, and it applies to every fixed rate home loan regardless of term length.

The most common loan terms are 15, 20, and 30 years. A 30-year term produces lower monthly payments but higher total interest paid. A 15-year term costs more each month but builds equity faster and reduces total interest significantly.

One critical distinction: your principal and interest payment is fixed, but your total monthly payment may not be. Freddie Mac notes that property taxes and homeowners insurance are included in most mortgage payments through an escrow account, and those costs can rise each year. Two borrowers with identical loans can end up with different total monthly payments because their local tax rates or insurance premiums differ.

Pro Tip: Ask your lender to break down your estimated monthly payment into its four components: principal, interest, taxes, and insurance. This gives you a realistic picture of what you will actually pay each month, not just the rate.

Here is what makes up a typical fixed rate mortgage payment:

- Principal: The portion that reduces your loan balance

- Interest: The cost of borrowing, calculated on the remaining balance

- Property taxes: Collected monthly and held in escrow by your lender

- Homeowners insurance: Required coverage, also typically escrowed

- PMI (if applicable): Private mortgage insurance for down payments below 20%

What are the benefits of a fixed rate mortgage?

The core benefit of a fixed rate mortgage is protection from interest rate volatility. Freddie Mac describes fixed rate loans as providing inflation and interest rate protection. If the Federal Reserve raises rates after you close, your payment does not change. That protection has real dollar value over a 30-year loan.

Predictable payments make budgeting straightforward. You know exactly what your principal and interest payment will be in year one, year ten, and year twenty-nine. That consistency lets you plan other financial goals around a stable housing cost.

“A fixed rate mortgage removes interest rate uncertainty because the rate is set and will not change.” — CFPB

Fixed rate loans also build equity on a predictable schedule. Every payment reduces your balance by a known amount, which matters if you plan to tap home equity later through a refinance or home equity line of credit.

The key benefits at a glance:

- Rate stability: Your interest rate never increases, no matter what markets do

- Budget certainty: Principal and interest payment stays constant for the full term

- Inflation protection: Rising rates in the economy do not affect your locked rate

- Term flexibility: 15, 20, and 30-year options let you match the loan to your financial plan

- Equity growth: Fixed amortization means steady, predictable equity accumulation

What are the drawbacks of a fixed rate mortgage?

Fixed rate mortgages carry a higher initial interest rate than adjustable rate mortgages. Lenders price in the risk of locking your rate for decades, so you pay a premium for that certainty upfront. In a low-rate environment, that premium is small. When rates are elevated, the gap between fixed and adjustable rates can be more noticeable.

Higher initial rates mean higher monthly payments in the early years compared to an ARM. For borrowers who plan to sell or move within five to seven years, paying that premium for long-term stability they will never use is a real cost.

Your total payment can still rise even with a fixed rate. Property taxes in Florida, for example, can increase as home values rise, pushing up your escrow payment. Homeowners insurance premiums have also climbed sharply in Florida in recent years, adding to total monthly costs.

Here are the main limitations to weigh:

- Higher starting rate: Fixed rates are typically higher than the initial rate on an ARM

- Less flexibility for short-term owners: If you move in five years, you paid for stability you did not need

- Refinancing required to capture rate drops: If market rates fall, your payment stays the same unless you refinance

- Refinancing has costs: CNBC notes that refinancing requires qualification and entails closing costs, so it is not automatic or free

- Escrow increases: Taxes and insurance can push total monthly payments higher over time

Pro Tip: If you plan to stay in the home for fewer than seven years, run the numbers on an ARM before committing to a fixed rate. The initial savings may outweigh the rate risk for a shorter holding period.

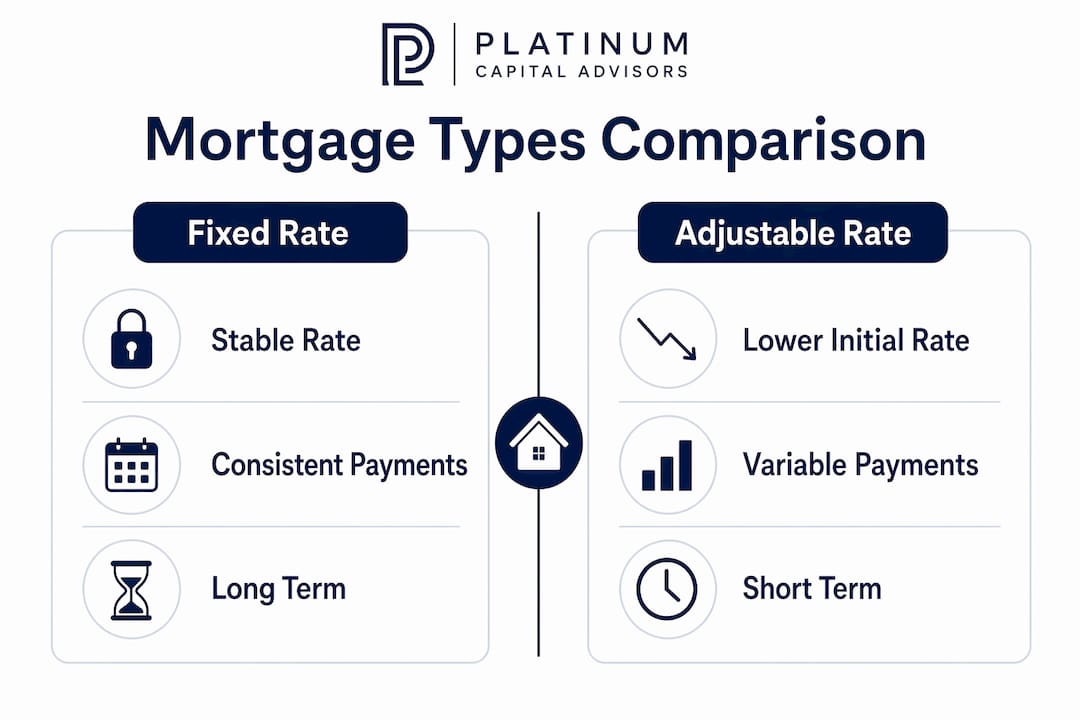

Fixed rate mortgage vs. adjustable rate mortgage: which is right for you?

An adjustable rate mortgage, or ARM, starts with a lower interest rate that is fixed for an initial period, typically 5, 7, or 10 years, and then adjusts periodically based on a market index. CNBC and Freddie Mac both highlight that ARMs offer lower initial rates but carry the risk of payment increases after the fixed period ends.

The lower starting rate on an ARM is real. It can mean meaningfully lower payments in the first years of the loan. The risk is that once the adjustment period begins, your rate and payment can rise, sometimes significantly, depending on market conditions.

Fixed rate loans suit borrowers who value certainty and plan to stay in the home long-term. ARMs suit borrowers who expect to sell or refinance before the adjustment period kicks in, or who believe rates will fall before their loan adjusts. You can also explore ARM loan options in Florida if a shorter-term strategy fits your situation.

FeatureFixed Rate MortgageAdjustable Rate MortgageInterest rateLocked for full termFixed initially, then adjustsMonthly payment stabilityHighLower initially, variable laterBest forLong-term homeownersShort-term owners or rate-drop bettorsRate riskNone after closingIncreases possible after fixed periodInitial rateHigher than ARMLower than fixed rateRefinancing needed to lower rateYesAdjusts automatically (up or down)

The right choice depends on how long you plan to stay, your tolerance for payment uncertainty, and where interest rates are heading. Most buyers in Florida who plan to own their home for ten or more years choose the fixed rate option for its simplicity and protection.

When should you choose a fixed rate mortgage?

Freddie Mac recommends fixed rate mortgages for homeowners planning to stay long-term who value predictable payments and budget certainty. That guidance covers the majority of first-time buyers and families purchasing a primary residence.

A fixed rate home loan makes the most sense when:

- You plan to stay in the home for seven or more years. The stability premium pays off over a long holding period.

- You are buying when rates are relatively low. Locking in a low rate protects you if rates rise later.

- You want a simple, predictable budget. No surprises from rate adjustments means easier long-term financial planning.

- You are risk-averse. If payment volatility would cause financial stress, the fixed rate removes that variable entirely.

- You are buying in a rising rate environment. Locking now protects you from future increases.

Refinancing remains a tool even after you lock a fixed rate. If market rates drop significantly, you can refinance into a lower fixed rate. The process requires qualifying again and paying closing costs, so the rate drop needs to be large enough to justify the expense. A common rule of thumb is that refinancing makes sense when you can lower your rate by at least 1 percentage point and plan to stay long enough to recoup the closing costs.

Key Takeaways

A fixed rate mortgage is the most reliable tool for long-term homeowners who need payment stability, and 92% of U.S. borrowers choose it for exactly that reason.

Why the “fixed payment” myth costs borrowers money

Most borrowers I work with come in believing their total monthly payment is locked forever once they sign. That belief leads to budget surprises in year two or three when their escrow payment jumps because property taxes were reassessed or their homeowners insurance premium increased.

The fixed rate is real and valuable. The fixed total payment is a myth. Freddie Mac is clear that the “fixed” label applies to principal and interest only. Taxes and insurance sit in a separate escrow bucket that your lender recalculates annually. In Florida, where property values and insurance costs have moved sharply, this distinction matters more than in most states.

My advice: when you receive a loan estimate, look at the full payment breakdown, not just the rate. Ask your lender what the escrow estimate is based on and whether it accounts for a potential tax reassessment after purchase. A home that was taxed at the previous owner’s assessed value will often see a significant tax increase in the first year after you buy it.

Refinancing is also misunderstood. Borrowers sometimes wait for rates to drop and assume they will automatically benefit. They will not. Refinancing requires a new application, a new appraisal in most cases, and closing costs that typically run into the thousands. The math only works if you stay in the home long enough to recover those costs through the lower payment. Plan that calculation before you refinance, not after.

— Chuck Barnes

Fixed rate home loans in Florida: how Platinumcapitalfinancial can help

Platinumcapitalfinancial works with home buyers across Florida, with deep experience in Naples, Collier County, and the surrounding Gulf Coast communities. Whether you are buying your first home or refinancing an existing loan, the team helps you compare fixed rate options across multiple lenders to find competitive rates that match your timeline and budget.

Platinumcapitalfinancial offers access to a wide range of fixed rate loan terms, from 15-year to 30-year products, along with refinancing guidance when market conditions shift in your favor. If you are weighing a fixed rate mortgage in Collier County or exploring your options as a Florida home buyer, connect with the Platinumcapitalfinancial team for a personalized rate consultation. You can also visit the mortgage broker Florida page to learn more about available loan programs and get started.

FAQ

What is the fixed mortgage definition in simple terms?

A fixed rate mortgage is a home loan where the interest rate is set at closing and never changes for the life of the loan. Your principal and interest payment stays the same every month until the loan is paid off.

How does a fixed rate mortgage differ from an ARM?

A fixed rate mortgage keeps the same interest rate for the full loan term, while an adjustable rate mortgage starts with a lower rate that can change periodically after an initial fixed period. ARMs carry the risk of higher payments if market rates rise.

Can my monthly payment change on a fixed rate mortgage?

Yes. Your principal and interest payment is fixed, but your total monthly payment can increase if property taxes or homeowners insurance premiums rise, since both are typically collected through an escrow account.

What are the most common fixed rate mortgage terms?

The most common terms are 15, 20, and 30 years. A 30-year term offers lower monthly payments, while a 15-year term costs more per month but reduces total interest paid and builds equity faster.

When does refinancing a fixed rate mortgage make sense?

Refinancing makes sense when market rates drop significantly below your current rate and you plan to stay in the home long enough to recover the closing costs through the lower monthly payment. CNBC notes that refinancing requires qualification and has costs, so the savings need to justify the process.

Recommended

- FRM FAQ's

- Mortgage term explained: A clear guide for Florida buyers

- Fixed Rate Mortgage vs ARM in Naples Florida

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)