Business

Best mortgage types for Florida first-time homebuyers

Buying your first home in Florida is exciting, but the mortgage process can feel like walking into a room full of acronyms and fine print with no map. FHA, USDA, VA, Conventional, PMI, MIP, DTI — it’s a lot to absorb before you’ve even found the house you love. The good news is that once you understand what each loan type is designed to do, the right choice becomes much clearer. This guide breaks down every major mortgage option available to Florida first-time buyers, shows you how to match each one to your finances, and explains the long-term cost differences that most people don’t discover until it’s too late.

Table of Contents

- Overview of mortgage types for first-time buyers in Florida

- How to assess your eligibility and fit for each mortgage type

- Florida-specific programs and restrictions to know

- Comparing long-term costs, fees, and exit strategies

- A seasoned lender's take: What most guides miss about choosing the right mortgage

- Connect with expert mortgage advisors in Florida

- Frequently asked questions

Key Takeaways

Overview of mortgage types for first-time buyers in Florida

Florida’s real estate market is one of the most active in the country, and lenders have tailored multiple loan programs to meet the needs of buyers across a wide range of incomes, credit backgrounds, and locations. Understanding your Naples mortgage products and statewide options starts with knowing the four core loan types.

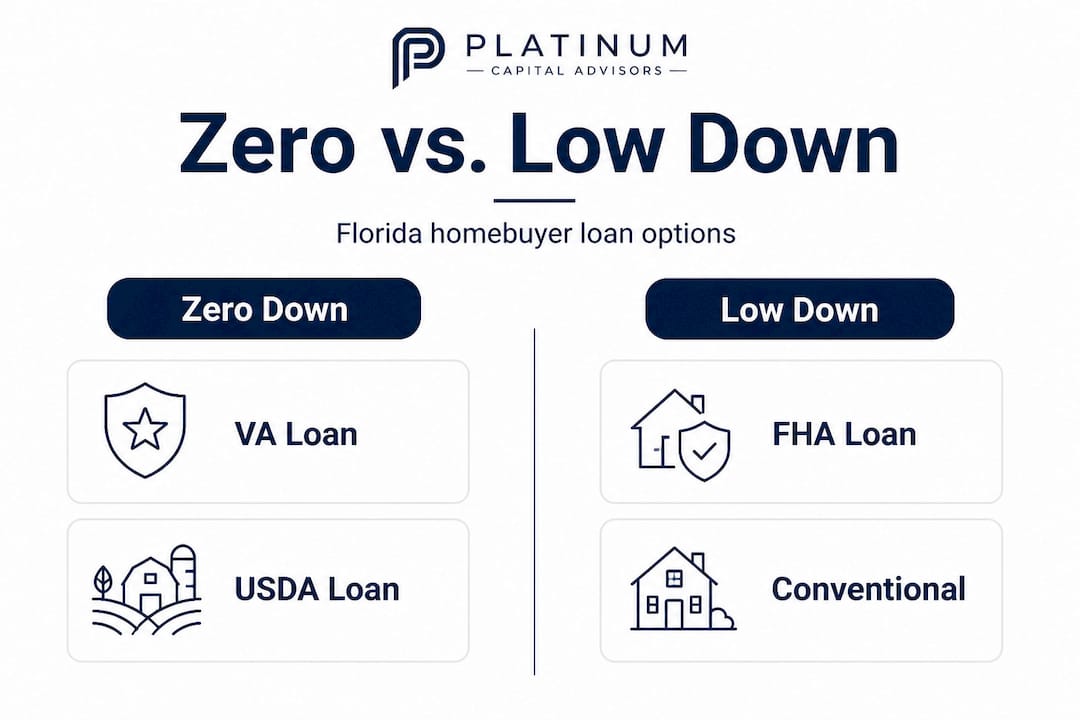

The main mortgage types for first-time homebuyers in Florida are FHA (3.5% down, minimum credit 580), Conventional (3-5% down, minimum 620), VA (0% down for eligible veterans), and USDA (0% down in rural areas with income limits). Each was built for a different buyer profile, and none of them is universally “best.”

Here is a quick side-by-side comparison to make the differences concrete:

A few things stand out in that table. VA and USDA loans require no down payment at all, which is a significant advantage for buyers who haven’t had years to save. However, both carry eligibility restrictions that immediately rule them out for many people. VA loans require military service, while USDA loans are tied to geographic location and household income. That’s why most first-time buyers in Florida end up looking closely at FHA and Conventional loans.

One factor many buyers overlook is student debt. If you’re carrying a high student loan balance, it raises your debt-to-income ratio (DTI), which is the percentage of your monthly income that goes toward debt payments. Review an income-driven repayment guide before you apply, because restructuring those payments could meaningfully improve your DTI and expand your loan options.

Key things to keep in mind when comparing loan types:

- FHA loans are federally insured, which is why lenders accept lower credit scores

- Conventional loans follow guidelines set by Fannie Mae and Freddie Mac and tend to reward stronger financial profiles

- VA loans are one of the most powerful benefits available to veterans, offering competitive rates without requiring mortgage insurance

- USDA loans serve a niche but important market, particularly for buyers targeting smaller towns and communities outside major metro areas

How to assess your eligibility and fit for each mortgage type

Once you know your options, the next step is pinpointing which loans you genuinely qualify for and which meet your needs. This isn’t just about credit score. Your full financial picture matters.

FHA suits lower credit borrowers at 580 and above, with limited savings and a flexible DTI up to 50%, but the lifetime mortgage insurance premium (MIP) increases your long-term costs considerably. Meanwhile, Conventional works best for buyers with a credit score of 680 or higher, because PMI (private mortgage insurance) can be canceled once you reach 20% equity, and the stricter DTI limit of around 43% keeps monthly obligations more controlled.

Here’s a quick table to map your situation to the most likely fit:

Use this numbered checklist before you start any application:

- Pull your credit report. Get your free report from all three bureaus. Look for errors that could be dragging your score down, because disputing even one wrong account can bump your score enough to shift your loan options.

- Calculate your DTI. Add up all your monthly debt payments (car loan, student loans, credit cards) and divide by your gross monthly income. A DTI above 43% will limit your Conventional options, though FHA allows up to 50%.

- Count your savings. Know your down payment amount and factor in closing costs, which typically run 2-5% of the purchase price in Florida. Many buyers forget about closing costs and come up short.

- Check your income stability. Lenders want to see two years of consistent income history. Frequent job changes or self-employment income require extra documentation.

- Confirm your location eligibility. If you're considering USDA, check whether the property address qualifies using the USDA's online eligibility map before you fall in love with a home.

Pro Tip: Calculate your DTI before talking to any lender. Most buyers discover their DTI is higher than expected because they forget to include minimum credit card payments and income-based student loan amounts. If you’re recently married, be aware that DTI changes for married buyers can affect how your joint finances are assessed.

Exploring minimum down payment options early in the process is also smart. Some buyers discover they qualify for down payment assistance programs that reduce the upfront cash required, effectively expanding which loan types make sense.

Florida-specific programs and restrictions to know

Knowing your eligibility is essential, but Florida adds unique programs and boundaries that can make or break your loan search. The state isn’t just a single market. A rural community in the Panhandle has completely different lending options than a buyer in downtown Tampa.

Here’s what you need to know about the Florida landscape:

- FHA and Conventional loans are the most flexible because they can be used to buy homes in virtually any location across the state, from urban condos in Miami to single-family homes in Gainesville

- VA loans remain the single strongest option for eligible buyers. Zero down payment, no private mortgage insurance, and competitive interest rates make this a benefit worth using if you've served

- USDA loans cover more of Florida than many people expect, but they are firmly excluded from major urban centers. If you're planning to buy in Miami, Orlando, Tampa, or Jacksonville proper, USDA is off the table

- Florida Hometown Heroes is a state-backed program that provides down payment and closing cost assistance to working Floridians in specific occupations like teachers, nurses, law enforcement officers, and firefighters

The Hometown Heroes program deserves a closer look. Funding for Hometown Heroes is approximately $50 million in 2026 and is distributed on a first-come, first-served basis. That sounds like a lot of money, but it disappears faster than most buyers expect once the program opens. Missing the window can mean waiting an entire year for the next funding cycle.

Pro Tip: If you work in a qualifying occupation and plan to buy in Florida this year, don’t treat Hometown Heroes as a backup plan. Treat it as your primary strategy and start your paperwork early, because when the funds run out, they’re gone.

One important distinction worth noting is that Hometown Heroes does not work as a standalone loan. It works alongside an FHA, Conventional, VA, or USDA loan, essentially layering down payment assistance on top of your primary mortgage. Your base loan still needs to meet all normal qualification standards.

Comparing long-term costs, fees, and exit strategies

Beyond eligibility and local programs, the true impact happens in your monthly bill and your long-term exit plan. This is where buyers frequently make costly assumptions.

Here’s a direct cost comparison between the main loan types:

The FHA MIP is permanent versus Conventional PMI, which can be removed. USDA excludes urban areas but charges lower fees than FHA overall. Hometown Heroes is occupation-specific, not available to all workers. These distinctions have real dollar consequences over time.

“The cheapest loan today is not always the cheapest loan over ten years. A Conventional loan with PMI that drops off at 20% equity will almost always cost less in total than an FHA loan where MIP stays for the life of the loan, even if the FHA rate starts lower.”

Three questions you should answer before making a decision based on fees alone:

- How long do you plan to stay? If you expect to sell or refinance within five years, the permanent nature of FHA's MIP matters less than it would over a thirty-year hold.

- Will you reach 20% equity quickly? If you're buying in an appreciating market (and much of Florida qualifies), a Conventional loan with PMI could see that insurance removed in just a few years.

- What is your realistic refinancing timeline? Many FHA buyers plan to refinance into a Conventional loan once their credit and equity improve. That's a legitimate strategy, but it comes with new closing costs, so factor that into your total cost math.

A seasoned lender’s take: What most guides miss about choosing the right mortgage

Most articles on this topic walk you through the basics and leave you to figure out the hard part on your own. Here’s a candid perspective from someone who works in Florida mortgages every day.

The most common mistake first-time buyers make is fixating on the interest rate and the down payment while ignoring how insurance fees compound over time. A 0.85% annual MIP on a $350,000 FHA loan adds nearly $3,000 per year to your cost, every year, with no expiration. Over ten years, that’s $30,000 more than a Conventional loan where PMI was canceled after year four. The difference between the two loans might feel invisible at closing and devastating at year seven.

Here’s the contrarian view: if you have a 650 credit score and plan to stay in your home long-term, putting more effort into improving your credit score by 30 points before applying could save you more money than any state assistance program ever would. A 680 credit score opens Conventional loan eligibility, and that single change can eliminate lifetime MIP entirely.

The Hometown Heroes program is genuinely valuable, but the urgency around funding is real. We’ve seen buyers hesitate for three months trying to gather perfect documentation, only to find the funding pool depleted when they were finally ready. Apply early. Ask your lender for an amortization scenario, not just a monthly payment quote. That scenario will show you exactly how much you’re paying in insurance, principal, and interest each year, and it makes the total cost differences between loan types immediately visible.

Buyers who plan to refinance or move within five to seven years should strongly favor Conventional loans even when they qualify for FHA. The cleaner exit and cancellable PMI provide flexibility. FHA loans can trap buyers in an insurance obligation they didn’t fully understand on day one.

Connect with expert mortgage advisors in Florida

Choosing a mortgage type is one of the most consequential financial decisions you’ll make. The right loan structure can save you tens of thousands of dollars over the life of the loan.

Our team of Naples mortgage advisors works with Florida first-time buyers every day, helping them navigate FHA, Conventional, VA, USDA, and Hometown Heroes options with clarity and confidence. We don’t just show you the monthly payment. We map out the full cost picture so you can compare loans the right way. Whether you’re just starting to explore or ready to move forward, we can match your credit profile and goals to the loan structure that genuinely fits your situation, not just the one that’s easiest to qualify for.

Pro Tip: When you meet with an advisor, ask for a side-by-side amortization comparison across at least two loan types. That single document will tell you more about the true cost of each option than any rate quote alone.

Frequently asked questions

What is the minimum credit score required for an FHA loan in Florida?

The minimum required credit score for an FHA loan in Florida is 580, which allows you to put just 3.5% down. Borrowers with scores between 500 and 579 may still qualify but are required to put down 10%.

How is mortgage insurance different between FHA and Conventional loans?

FHA MIP is permanent for most borrowers, while Conventional PMI can be canceled once your equity reaches 20%. This difference in cancelability often makes Conventional loans significantly less expensive over a full loan term.

Are USDA loans available in cities like Miami?

No, USDA excludes urban centers like Miami, and the loan is limited to rural and select suburban areas. You can check a specific property address on the USDA’s official eligibility map before factoring this program into your plans.

Does Florida offer special mortgage programs for first responders or teachers?

Florida’s Hometown Heroes program provides down payment and closing cost assistance to eligible occupations, but Hometown Heroes funding is limited to approximately $50 million in 2026 and is distributed on a first-come, first-served basis. Applying early is essential because funds typically deplete quickly once the program opens.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)