Mortgage News

Interest-only mortgages: smart strategies for Florida homebuyers

Interest-only mortgages carry a reputation for being risky products reserved for wealthy investors or reckless borrowers chasing homes they can’t afford. That reputation isn’t entirely wrong, but it’s not entirely right either. For the right Florida homebuyer, an interest-only loan can be a genuinely powerful tool for managing cash flow, maximizing investment returns, or bridging a period of income growth. The key word is “right.” This guide walks you through exactly how these loans work, what they cost in real numbers, who actually qualifies, and the situations where they make sense versus when they can seriously hurt you.

Table of Contents

- What is an interest-only mortgage?

- How do payments and equity work with interest-only loans?

- Who qualifies for an interest-only mortgage?

- Interest-only vs. traditional mortgages: key differences

- When does an interest-only mortgage make sense?

- The uncomfortable truth about interest-only mortgages in Florida

- Explore your Florida mortgage options

- Frequently asked questions

Key Takeaways

What is an interest-only mortgage?

An interest-only mortgage is exactly what the name says. For an initial period, your monthly payment covers only the interest charged on the loan. You pay nothing toward the actual loan balance. As Bankrate explains, an interest-only mortgage is a loan where borrowers pay only the interest portion for an initial period, typically 5 to 10 years on a 30-year term, after which payments increase to include principal and interest, or a balloon payment is due.

That shift at the end of the initial period is where many borrowers get into trouble. The payments don’t just nudge upward. They can jump dramatically because you’re now repaying the same loan balance in a compressed timeframe.

Here’s what the structure typically looks like:

- Interest-only period: 5 to 10 years of lower, interest-only payments

- Repayment period: Remaining 20 to 25 years with fully amortized payments (principal plus interest)

- Balloon option: Some loans require the full remaining balance paid at once at the end of the interest-only term

- Rate structure: Most are adjustable-rate mortgages (ARMs), meaning the rate can change after the initial fixed period

“Most interest-only loans are structured as ARMs, not fixed-rate loans. That means your rate risk and payment risk can both hit at the same time when the initial period ends.”

Pro Tip: If you’re considering an interest-only loan, always ask the lender for a full payment schedule showing what your monthly costs look like in year 1, year 5, and year 11. Seeing those numbers side by side is a reality check that saves surprises later.

With the basics outlined, let’s look at how payments on an interest-only loan actually compare to traditional options.

How do payments and equity work with interest-only loans?

The appeal of interest-only loans is immediate and obvious when you look at the monthly payment difference. According to Bankrate’s mortgage data, on a $350,000 loan at 6.5%, an interest-only payment runs approximately $1,896 per month during the initial period, compared to roughly $2,610 per month on a fully amortizing loan. That’s over $700 in monthly savings.

Here’s a simplified comparison table for a $350,000 loan at 6.5%:

Those savings look attractive. But the equity column tells the other side of the story. Every dollar of that $700 monthly savings comes at the cost of zero equity growth from your required payments. You’re essentially renting money from the bank.

The risks compound in a few specific ways:

- No equity cushion: If Florida home values drop even modestly, you could owe more than the home is worth

- Payment shock: When the interest-only period ends, your payment can jump 37% or more overnight

- Compressed repayment: You're paying off the full original balance in 20 or 25 years instead of 30, which inflates the post-reset payment

- Rate reset risk: If your ARM rate adjusts upward at the same time, the payment increase is even steeper

You can explore Naples mortgage payment examples to see how these numbers play out in Florida’s specific market conditions.

Pro Tip: If you take an interest-only loan, consider making voluntary principal payments during the interest-only period whenever cash flow allows. Even $200 to $300 extra per month reduces the balance and softens the payment shock later.

Now that you’ve seen the numbers in action, let’s tackle the requirements to actually get approved for an interest-only mortgage in Florida.

Who qualifies for an interest-only mortgage?

Interest-only mortgages are not available through standard government-backed programs like FHA, VA, or USDA loans. They fall under what lenders call non-QM (non-qualified mortgage) products, meaning they don’t meet the standard federal lending guidelines. That alone tells you something important: lenders take on more risk with these loans, so they require borrowers who are financially strong.

According to Bankrate’s qualification criteria, typical requirements include a credit score of 700 or higher, a debt-to-income ratio (DTI) of 43% or less, a minimum 20% down payment, and documented proof of future income or substantial assets.

Here’s what lenders typically look for in Florida:

- Credit score: 700 minimum, with better terms available above 720 or 740

- Down payment: At least 20%, with no private mortgage insurance (PMI) exceptions

- DTI ratio: Total monthly debts divided by gross income must stay under 43%

- Asset documentation: Bank statements, investment accounts, or proof of future income (bonuses, commissions, business revenue)

- Property type: More commonly approved for higher-value properties, investment properties, or second homes

“Non-QM lenders in Florida can offer more flexibility on income documentation, which is why interest-only loans appeal to self-employed borrowers and real estate investors who have strong assets but variable income.”

As noted by Starr Mortgage, these loans are available in Florida through non-QM lenders and are especially common in high-value markets like Miami, where buyers use them to access larger homes or maximize investment cash flow.

To understand how Florida-specific lender requirements apply to your situation, reviewing Florida mortgage lender requirements can help you gauge where you stand before applying.

Understanding qualification is critical, but what exactly are the trade-offs between interest-only and traditional loans? Let’s compare.

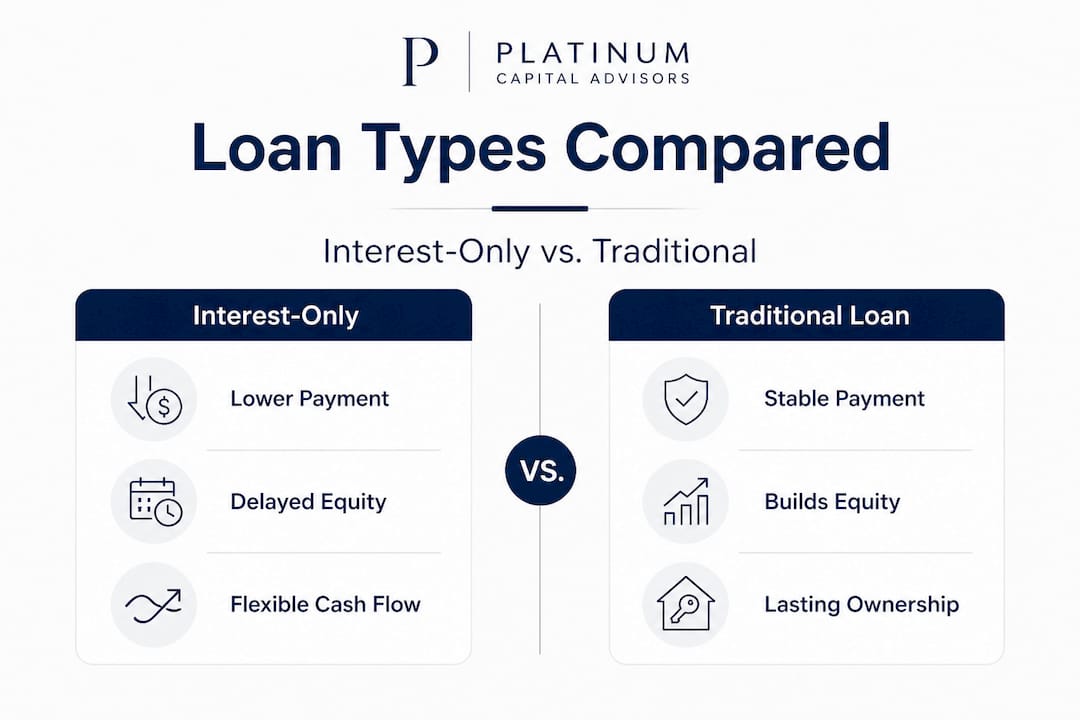

Interest-only vs. traditional mortgages: key differences

Choosing between an interest-only loan and a traditional mortgage isn’t just about the monthly payment. It’s about your financial goals, your timeline, and your tolerance for risk. Here’s a direct comparison:

As Bankrate’s mortgage analysis points out, interest-only loans are often structured as ARMs with a fixed introductory rate that later adjusts, and repayment options after the initial period include amortizing over the remaining term, refinancing, selling, or a balloon payment.

The pros are real. According to NerdWallet’s research, lower payments boost cash flow for investments, increase buying power, and offer flexibility for short-term holds or periods of income growth.

But the cons are equally real. Bankrate’s data shows that payment shock can hit 37% or more at reset, and the combination of no equity buildup with potential home value declines creates genuine negative equity risk.

Key decision factors:

- Planning to sell within 5 to 7 years? Interest-only may work well

- Want a stable primary home for 20+ years? Traditional fixed-rate is almost always better

- Investing in rental properties in Florida? Interest-only can improve monthly cash flow

- First-time buyer or tight on reserves? Avoid interest-only products

You can compare ARM vs. fixed-rate mortgages in more detail to understand which structure fits your specific Florida purchase.

You’ve seen how they compare. Now let’s explore real-world scenarios where an interest-only mortgage may or may not be the right fit.

When does an interest-only mortgage make sense?

The honest answer is: for fewer people than the marketing suggests, but more people than the critics admit. Context matters enormously.

According to NerdWallet’s guidance, interest-only loans work best for investors maximizing cash flow, borrowers with variable or bonus-heavy income, and buyers with short-term plans to sell or refinance. They are not appropriate for long-term primary residence buyers, first-time homebuyers, or risk-averse borrowers.

Scenarios where interest-only can make sense in Florida:

- A real estate investor buying a short-term rental in Naples who wants to maximize monthly cash flow during the first 7 years of ownership

- A physician or attorney early in their career with a low current salary but a clear trajectory toward significantly higher income within 3 to 5 years

- A buyer purchasing a second home in South Florida who plans to sell their primary residence within 5 years and use the proceeds to pay down or pay off the second property

- A developer or investor doing a value-add renovation who plans to refinance into a conventional loan once the property appreciates

Red flags that suggest interest-only is the wrong choice:

- You're buying your forever home and don't have a concrete exit strategy

- Your income is already at or near its peak with little expected growth

- Your emergency fund is thin, meaning payment shock could be catastrophic

- You're counting on Florida home values to keep rising to protect your equity position

As Miami mortgage experts note, these loans suit Miami and high-cost Florida buyers seeking larger homes or investment properties, but they work best when paired with a clear refinance or sale strategy given the market’s volatility.

Pro Tip: Write down your exit strategy before you sign. Literally write it down. “I will refinance into a 30-year fixed in year 6 when my income reaches X” or “I will sell this property before year 8 when the interest-only period ends.” Vague plans become expensive regrets.

“The Florida market can move fast in both directions. An interest-only loan in a rising market feels like genius. In a flat or declining market, it can feel like a trap. Your exit strategy is your insurance policy.”

With all the evidence and advice laid out, it’s time for a candid perspective on what most homebuyers, especially in Florida, really tend to miss about interest-only mortgages.

The uncomfortable truth about interest-only mortgages in Florida

Most articles about interest-only mortgages focus on the payment math. We want to talk about the psychology, because that’s where most borrowers go wrong.

When you’re sitting across from a lender and the interest-only payment is $700 lower per month than the traditional option, it’s easy to rationalize. “I’ll invest the difference.” “My income will be higher in five years.” “Florida real estate always goes up.” These statements might all be true. But they’re also the exact things people said in 2005, right before the market showed everyone just how wrong comfortable assumptions can be.

Here’s what we’ve seen repeatedly in Florida: buyers treat the interest-only period as a grace period rather than a strategic window. They spend the monthly savings instead of deploying them intentionally. They don’t build an emergency reserve. They don’t make voluntary principal payments. And then year 7 or year 8 arrives, and the payment jump feels like an ambush.

The single biggest mistake is entering an interest-only loan without a written, realistic exit plan. Not a vague intention to refinance “someday,” but a specific plan with a timeline, a target credit score, a target income level, and a target home value that makes the refinance math work.

Florida’s property markets add another layer of complexity. Markets like Miami, Naples, and Orlando can appreciate rapidly, which makes interest-only loans look brilliant in hindsight. But they can also stagnate or correct, particularly in the condo market or in areas dependent on tourism and seasonal demand. Timing and local expertise aren’t just helpful. They’re essential.

Interest-only loans are tools, not shortcuts. Used with discipline and a real plan, they can genuinely expand what’s possible for Florida buyers. Used as a way to afford more home than you can realistically handle, they’re a slow-moving financial problem.

Explore your Florida mortgage options

Deciding whether an interest-only mortgage fits your situation isn’t something you should figure out alone, especially in a market as dynamic as Florida’s.

At Platinum Capital Financial, we work with Florida homebuyers and investors across Naples, Collier County, and beyond to find loan structures that match real financial goals, not just the lowest initial payment. Whether you’re exploring interest-only options, comparing ARM versus fixed-rate products, or simply trying to understand what you qualify for, our team can walk you through the numbers honestly. Visit Platinum Capital Financial to connect with a Florida mortgage specialist who understands the local market and can help you build a strategy that holds up when the interest-only period ends.

Frequently asked questions

Do interest-only mortgages build equity over time?

No, you don’t build equity through required payments during the interest-only period. As Bankrate confirms, no principal is reduced unless you make additional voluntary payments toward the balance.

Are interest-only mortgages available for first-time buyers in Florida?

Generally, they are not recommended or available for first-time buyers. Bankrate’s qualification standards show that lenders require a 700+ credit score, 20% down payment, and documented assets, which most first-time buyers don’t yet have.

What happens when the interest-only period ends?

Your monthly payment jumps significantly as you begin repaying principal on the remaining balance, or you may face a large balloon payment if you haven’t refinanced or sold. Bankrate’s loan structure data confirms that payments increase to include both principal and interest, or a balloon payment becomes due.

Are interest-only loans common in Florida now?

They are less common than before 2008 due to tighter federal regulations, but they remain available through non-QM lenders. According to Starr Mortgage, these products are available via non-QM lenders and are most active in Florida’s high-value and investment property segments.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)