Mortgage News

How to calculate your Florida mortgage rate and save

Figuring out your mortgage rate in Florida can feel like solving a puzzle with missing pieces. You see advertised rates online, but your actual number looks different once a lender runs your details. That gap between what you expect and what you get is where first-time buyers lose confidence and sometimes make costly decisions. This guide walks you through exactly what drives your rate, what information you need to gather, how to run the numbers yourself, and how to spot errors before they cost you. By the end, you will know how to approach any Florida lender with clarity and confidence.

Table of Contents

- What affects mortgage rates in Florida?

- Requirements and tools for calculating your rate

- Step-by-step: How to calculate your Florida mortgage rate

- Common pitfalls and how to verify your mortgage calculation

- Our take: What most first-time buyers get wrong when calculating mortgage rates

- Ready for expert help? Get your personalized Florida mortgage rate

- Frequently asked questions

Key Takeaways

What affects mortgage rates in Florida?

Now that you know why calculating your mortgage rate matters, let’s break down the specific elements driving rates in Florida.

Florida is not just any housing market. It carries its own set of financial variables that can push your rate up or down compared to what you might see quoted nationally. Mortgage rates in Florida vary based on credit score, loan amount, type of loan, and market trends. Understanding each factor gives you real leverage when shopping for a loan.

The core factors that shape your rate:

- Credit score: This is the single biggest lever you control. A score above 740 typically unlocks the best available rates. Drop below 680, and lenders will price in more risk, which means a higher rate for you.

- Loan type: Conventional loans, FHA loans, VA loans, and USDA loans all carry different base rates. FHA loans are popular with first-time buyers because they allow lower down payments, but they also require mortgage insurance premiums that add to your monthly cost.

- Down payment: Putting down 20% or more removes the need for private mortgage insurance (PMI), a monthly fee that protects the lender if you default. Less than 20% down means PMI gets added to your payment.

- Loan amount and term: A 30-year fixed loan carries a higher rate than a 15-year fixed loan because the lender is exposed to risk for twice as long. Jumbo loans, which exceed conforming loan limits, also carry slightly higher rates.

- Property location: Rates can vary by county within Florida. Lenders factor in local property values, foreclosure rates, and economic conditions.

- Current market conditions: The Federal Reserve's benchmark rate, inflation data, and bond market movements all influence where mortgage rates land on any given day.

Florida also has some unique financial considerations that national calculators often miss. Homeowners insurance in Florida is significantly more expensive than in most other states, driven by hurricane risk, flooding exposure, and a challenging insurance market. Property taxes vary widely by county, with some areas offering homestead exemptions that reduce your assessed value. These costs do not change your interest rate, but they absolutely change your total monthly payment, which is what truly determines affordability.

Florida rate factors vs. national standard rate factors:

Recent data shows Florida average mortgage rates for a 30-year fixed loan have been hovering between 6.5% and 7.5% in 2026, closely tracking national trends but with local variation depending on the lender and the borrower’s profile.

Requirements and tools for calculating your rate

Understanding the factors helps. Now let’s gather everything you need to start the calculation process efficiently.

Before you open a single calculator, you need the right data in front of you. Having essential information on hand speeds up the calculation process and prevents you from getting inaccurate estimates that could mislead your planning.

Information you need to gather before calculating:

- Your current credit score (pull a free report from AnnualCreditReport.com)

- Gross monthly income (before taxes, all sources)

- Estimated purchase price of the home

- Planned down payment amount and percentage

- Estimated annual property taxes for the specific property

- Estimated annual homeowners insurance premium

- Whether flood insurance will be required

- Any existing monthly debts (car payments, student loans, credit cards)

That last item matters more than most first-time buyers realize. Lenders use a calculation called the debt-to-income ratio (DTI), which compares your total monthly debt payments to your gross monthly income. Most conventional lenders want your total DTI below 43%, and ideally below 36%.

Reliable tools for calculating Florida mortgage rates:

Pro Tip: Before you sit down to calculate, gather your two most recent pay stubs, your last two years of tax returns, and your most recent bank statements. This is the same documentation a lender will request, so having it ready means you can verify your inputs are accurate rather than estimated.

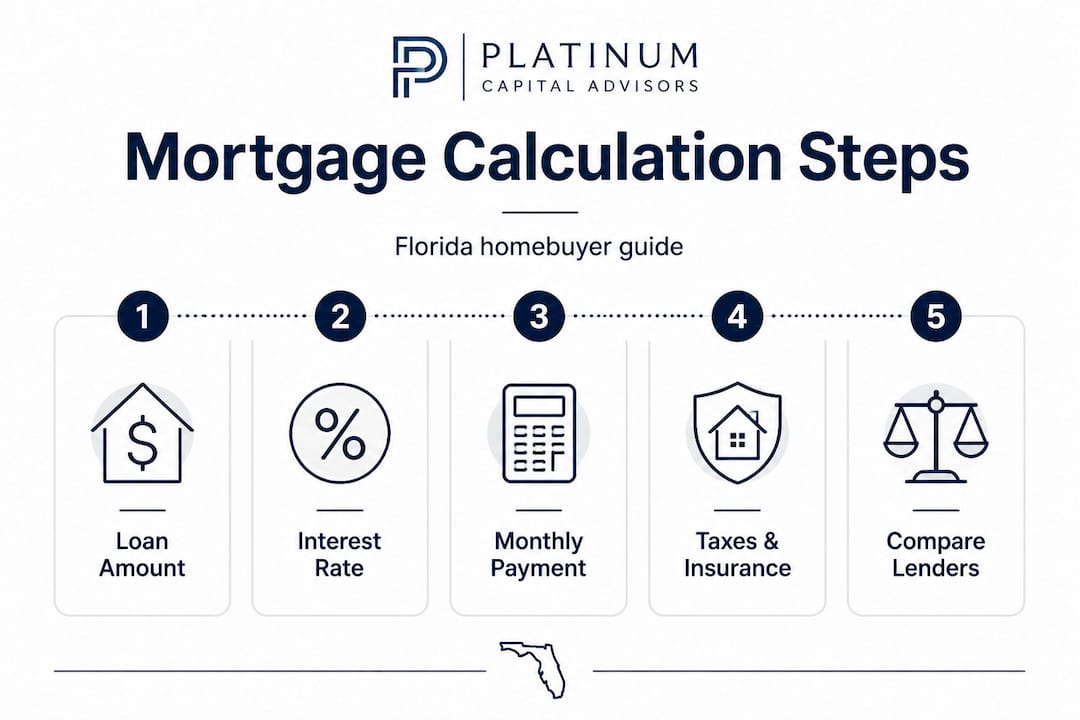

Step-by-step: How to calculate your Florida mortgage rate

With your information and tools in hand, it’s time to walk through the actual calculation steps so you can get transparent on your options.

Let’s use a realistic Florida scenario. You are purchasing a home for $300,000 in Collier County. You have a 20% down payment ($60,000), leaving a loan amount of $240,000. Your credit score is 720, and the current rate offered to you is 7.0% on a 30-year fixed loan. Annual property taxes are estimated at $3,600, and homeowners insurance runs $2,400 per year.

Step 1: Confirm your loan amount Subtract your down payment from the purchase price. In this case, $300,000 minus $60,000 equals $240,000. This is your principal.

Step 2: Identify your interest rate Your lender quotes you 7.0% annually. Divide by 12 to get your monthly rate: 7.0% divided by 12 equals 0.5833% per month, or 0.005833 as a decimal.

Step 3: Apply the amortization formula The standard formula for a fixed-rate mortgage payment is:

M = P × [r(1+r)^n] / [(1+r)^n - 1]

Where M is your monthly payment, P is the principal ($240,000), r is the monthly interest rate (0.005833), and n is the number of payments (360 for a 30-year loan). Plugging in those numbers gives you a principal and interest payment of approximately $1,597 per month.

Step 4: Add taxes and insurance Divide annual property taxes by 12: $3,600 / 12 = $300 per month. Divide annual insurance by 12: $2,400 / 12 = $200 per month. Your total monthly payment (often called PITI: principal, interest, taxes, insurance) becomes roughly $2,097 per month.

Step 5: Compare across multiple lenders Online calculators can help estimate rates, but knowing the calculation formula is valuable when you want to verify a lender's quote by hand. Run the same scenario on at least two or three lender websites to see how their quoted rates change your monthly payment.

Pro Tip: Even a 0.25% difference in rate on a $240,000 loan adds up to roughly $10,000 to $15,000 over the life of a 30-year mortgage. Always compare at least three lenders before committing.

Florida homebuyers with similar profiles in 2026 are seeing total monthly payments (PITI) ranging from roughly $1,900 to $2,400 on a $300,000 purchase, depending on their rate, insurance costs, and local tax rates. Coastal properties with flood insurance requirements can push that range even higher.

Common pitfalls and how to verify your mortgage calculation

Once you’ve calculated a sample rate, it’s crucial to check for accuracy and be aware of common missteps.

First-time homebuyers often overlook property insurance and taxes in their monthly calculations, which leads to a nasty surprise when the actual payment is hundreds of dollars higher than expected. Knowing what to watch for keeps you from making a decision based on incomplete numbers.

Top mistakes first-time buyers make when calculating mortgage rates:

- Using only the advertised rate: Advertised rates are often based on ideal borrower profiles (760+ credit score, 20% down). Your actual rate may be higher.

- Forgetting PMI: If your down payment is under 20%, PMI typically adds $80 to $200 per month to your payment on a $240,000 loan.

- Ignoring flood insurance: In many Florida counties, flood insurance is mandatory and can cost $1,000 to $3,000 per year or more, especially in coastal zones.

- Using outdated tax estimates: Property tax rates change, and online listings sometimes show old figures. Always verify with the county property appraiser's website.

- Not accounting for HOA fees: Many Florida communities have homeowners association fees that are separate from your mortgage but still affect your monthly budget.

“Always double-check your lender’s assumptions for fees and taxes. A quote that looks affordable on paper can change significantly once all the real costs are added in.”

To verify your calculation, use a second independent calculator and compare the output. If the numbers differ by more than $50 to $100 per month, dig into which inputs are different. Lenders are required to provide a Loan Estimate document within three business days of your application. This document itemizes every cost, including estimated taxes, insurance, and fees, giving you a standardized way to compare offers side by side.

Pro Tip: When navigating Florida mortgage calculations, always request the Annual Percentage Rate (APR) alongside the interest rate. The APR includes lender fees and gives you a more complete picture of the true cost of the loan.

Our take: What most first-time buyers get wrong when calculating mortgage rates

Here is something we see constantly working with Florida buyers: people obsess over the interest rate percentage and completely ignore everything surrounding it. Someone will spend two weeks negotiating a rate down from 7.1% to 6.9% and then accept a loan with $5,000 in unnecessary origination fees, wiping out any savings they gained.

The rate is just one number in a larger equation. The real question is what your all-in monthly payment looks like and whether it fits your life. A buyer in Naples with a 7.0% rate but low property taxes and reasonable insurance might actually pay less per month than a buyer in Miami with a 6.75% rate but sky-high insurance premiums and HOA fees.

We have also seen buyers get pre-approved based on a rate they saw advertised, then feel blindsided when their actual rate comes back higher. That gap usually comes down to credit score tiers, loan-to-value ratio, and sometimes the property type itself (condos often carry slightly higher rates than single-family homes).

The buyers who navigate this process best are the ones who focus on the total monthly payment number, not just the rate. They ask lenders to show them the full PITI breakdown from day one. They also understand that local Florida mortgage expertise matters because a broker who works in the Florida market daily knows which lenders are competitive right now and which ones are not.

One more thing worth saying directly: the calculation itself is not the hard part. The hard part is making sure the numbers you plug into the formula are accurate and current. Garbage in, garbage out. Spend the extra time verifying your insurance estimates and tax figures before you fall in love with a payment that does not reflect reality.

Ready for expert help? Get your personalized Florida mortgage rate

You now have a solid foundation for understanding and calculating your Florida mortgage rate. But knowing the formula is different from knowing which lenders in Florida are offering the best terms for your specific credit profile and loan size right now.

At Platinum Capital Financial, we work with first-time buyers across Florida every day, helping them cut through the noise and find affordable Florida mortgage guidance that fits their real budget. We compare multiple lenders on your behalf, explain every line of your Loan Estimate, and make sure your monthly payment reflects all the real costs, not just the rate. Whether you are buying in Naples, Fort Myers, or anywhere in between, we can help you move forward with confidence. Reach out today and let’s find the right loan for your situation.

Frequently asked questions

What is the current average mortgage rate in Florida?

Mortgage rates in Florida fluctuate with market conditions, but in 2026, 30-year fixed rates are generally ranging from 6% to 7.5% depending on the borrower’s credit profile and lender.

How does my credit score impact my mortgage rate?

Mortgage rates vary based on credit score, and a higher score typically qualifies you for a lower rate, which can save you tens of thousands of dollars over the life of a 30-year loan.

Are property taxes and insurance included in mortgage rate calculations?

Homebuyers often overlook property insurance and taxes because they are not part of the base interest rate, but they are essential components of your total monthly payment and should always be factored in from the start.

Can I lock in a mortgage rate in Florida before closing?

Yes, most lenders offer a rate lock option that protects you from rate increases between your application and closing, though the lock period and any associated fees will vary by lender.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)