Business

The Role of Mortgage Documents in Home Loans

Most people dread mortgage paperwork. The stack of forms at closing looks overwhelming, and the legal language does not make it easier. But the role of mortgage documents goes far beyond bureaucratic formality. Each document serves a specific legal and financial purpose, protecting both you and the lender throughout one of the largest transactions of your life. If you understand what these documents do and why they exist, you stop being intimidated by them and start using them as tools that work in your favor.

Table of Contents

- Key takeaways

- The role of mortgage documents in your loan

- How mortgage documents work through the loan lifecycle

- Common pitfalls in the mortgage documentation process

- Organizing and storing your mortgage documents post-closing

- My take on mortgage paperwork after years in the industry

- Ready to move forward with confidence?

- FAQ

Key takeaways

The role of mortgage documents in your loan

When you apply for a home loan, you are not just filling out forms. You are creating a legally binding financial relationship between yourself and a lender. The role of documentation in mortgage transactions is to define that relationship with precision, so there is no ambiguity about what either party owes, owns, or is responsible for.

Here are the core documents you will encounter and what each one actually does:

- Mortgage or deed of trust. This is the security instrument. It gives the lender the legal right to foreclose on the property if you stop making payments. Florida uses the mortgage document rather than a deed of trust, which is an important distinction for state residents to understand.

- Promissory note. This is your written promise to repay the loan. It spells out the loan amount, interest rate, repayment schedule, and what happens if you default. The promissory note is the lender's primary evidence of your debt.

- Closing Disclosure. This five-page document details your final loan terms, monthly payment, closing costs, and any credits or fees. Borrowers frequently overlook this document, but it deserves careful review before you sign anything else at the closing table.

- Loan application (Form 1003). The Uniform Residential Loan Application collects your financial history, employment, income, assets, and debts. Lenders use this to determine whether you qualify and at what terms.

- Government-required disclosures. These include the Loan Estimate, the Right of Rescission notice (for refinances), and HMDA data forms. They exist to protect you from predatory lending and ensure transparency.

- Supporting verification documents. Think W-2s, recent pay stubs, two months of bank statements, tax returns, and a property appraisal. These verify that the information on your loan application is accurate.

Pro Tip: Request a copy of your Closing Disclosure at least three business days before your closing appointment. Compare it line by line against your Loan Estimate to catch any unexpected fee changes before you are at the table.

The importance of mortgage paperwork becomes clear when you realize that these documents do not just record a transaction. They define your legal rights, your obligations, and your recourse if something goes wrong.

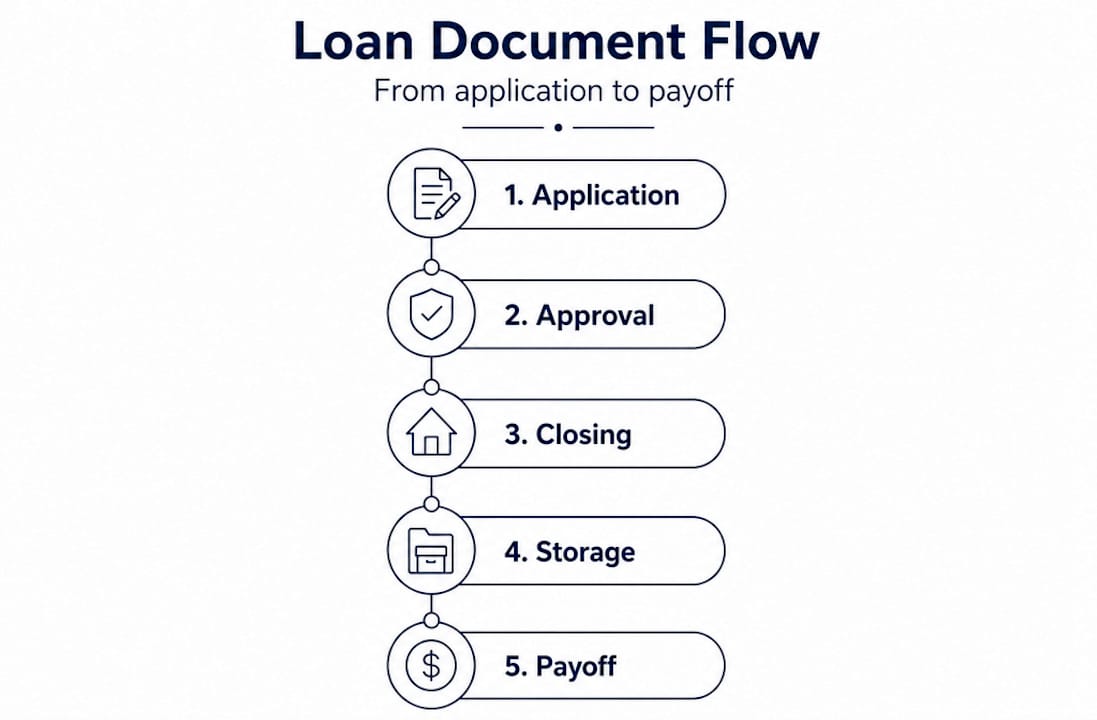

How mortgage documents work through the loan lifecycle

Understanding the types of mortgage documents is one thing. Knowing when they appear and why they matter at each stage is where real clarity comes from.

- Application stage. You submit your loan application along with income and asset documents. Within three business days, your lender is federally required to send you a Loan Estimate that shows your projected interest rate, monthly payment, and closing costs. This timeline is not a courtesy. It is mandated under TRID (TILA-RESPA Integrated Disclosure) regulations.

- Underwriting stage. Your file goes to an underwriter who verifies every claim on your application. The mortgage approval process can take up to 60 days and requires thorough verification of income, assets, debts, and employment. Appraisal reports, title searches, and flood certifications also arrive during this phase. Any gap in your documentation stops the clock.

- Conditional approval. The underwriter typically issues approval with conditions, meaning you must provide additional documents before final clearance. This is where automated systems help lenders track outstanding items and notify borrowers of what is still needed. The mortgage documentation process at this stage is methodical and specific.

- Closing stage. You sign the mortgage, promissory note, Closing Disclosure, and a package of other documents at your loan closing appointment. Signing errors cause funding delays that can affect your locked interest rate and closing schedule. This is why loan signing agents are so valuable. They are trained to catch missing initials, unsigned pages, and incorrect dates before the package leaves the room.

- Post-closing. Your lender packages and delivers your loan file to the investor who purchases the loan on the secondary market. There is a specific stacking order required for this delivery, and misordering documents can trigger investor rejection and repurchase demands. Your responsibilities at this stage are simpler: keep your copies organized and make your payments on time.

Pro Tip: At closing, bring a government-issued photo ID and a certified or cashier’s check if your lender requires it. Personal checks are rarely accepted at the closing table.

Common pitfalls in the mortgage documentation process

The role of mortgage disclosure is not just informational. It is a compliance function, and the consequences of getting it wrong are significant for lenders and borrowers alike.

Lenders face serious regulatory exposure when disclosures are mishandled. Compliance violations in mortgage lending are heavily concentrated in a small number of statutes, with 75% of cited issues in 2025 stemming from just five laws. The Home Mortgage Disclosure Act (HMDA) is one of the most common sources of trouble. Inaccurate data fields account for 82% of HMDA violations, often because loan officers enter information inconsistently during the application stage.

For borrowers, the pitfalls are less about regulatory fines and more about practical consequences. Here is what commonly goes wrong and how to avoid it:

- Missing or incomplete signatures. A single unsigned line can send your entire closing package back to the title company, delaying funding by days. Review every page before you hand it back.

- Outdated income documents. Lenders typically require documents dated within 30 to 60 days. If your pay stubs or bank statements are older than that, get fresh ones before submitting.

- Inconsistent information. If your application says you have been at your job for two years but your W-2 shows otherwise, the underwriter will flag it and request a letter of explanation. Consistency matters.

- Late disclosure delivery. If a lender sends your Closing Disclosure fewer than three business days before closing, you have the legal right to postpone signing until the waiting period is satisfied.

Automated document management reduces loan processing time by 40 to 70% by eliminating manual classification errors and speeding up data extraction. For borrowers working with tech-forward lenders, this translates to faster approvals and fewer requests for the same documents twice.

Organizing and storing your mortgage documents post-closing

Once the loan closes, most borrowers file their documents in a drawer and forget about them. That is a mistake. The importance of mortgage paperwork does not end at closing.

Keep mortgage records for up to seven years post-closing to support tax filings, refinancing applications, and insurance claims. Here is what to prioritize:

- Promissory note and mortgage. Keep these for the life of the loan plus seven years. They prove the original loan terms and are critical if a dispute arises with the servicer.

- Closing Disclosure. This document shows what you actually paid at closing, including points, prepaid interest, and escrow deposits. It is useful for tax deductions and future refinancing comparisons.

- Deed. Your county records office holds the official copy, but keep a personal copy as well.

- Payment history. Request an annual mortgage statement from your servicer and keep it. This protects you if a payment is ever disputed.

- Insurance and title documents. Store your title insurance policy and homeowner's insurance declarations page with your mortgage files.

For digital storage, use an encrypted cloud service and name files clearly (for example, “Closing Disclosure 2024” or “Promissory Note Signed”). Physical copies should go in a fireproof safe or a safe deposit box at your bank.

Pro Tip: When you pay off your mortgage, request a Satisfaction of Mortgage document from your lender and make sure it gets recorded with your county. Without it, the lien technically still shows on your property title.

Knowing how to organize mortgage documents also pays dividends when you refinance. A lender can pull up your original terms, compare them against current rates, and move through underwriting faster because well-prepared borrowers reduce underwriting review time significantly.

My take on mortgage paperwork after years in the industry

I have worked with hundreds of borrowers in Florida, and the pattern I see most often is this: people spend months saving for a down payment but zero hours understanding the documents they will sign at closing. Then they sit at the table for two hours, signing things they have never seen before, hoping everything is correct.

That gap between financial preparation and document literacy is where most of the stress and many of the delays originate. The borrowers who move through the process smoothly are the ones who ask for their Closing Disclosure early, compare it against their Loan Estimate, and flag any discrepancy before closing day. They are not mortgage attorneys. They just paid attention.

What I have learned is that the document review process is not about catching your lender doing something wrong. In most cases, lenders are operating in good faith. It is about knowing what you agreed to, because once you sign, you own those terms. Technology has made it easier to manage documents electronically, but it has not replaced the value of a borrower who reads before they sign.

If you are working with an experienced mortgage professional, lean on them. Ask them to walk you through the Closing Disclosure before closing day. Ask what each line means. That conversation costs you thirty minutes and can save you years of confusion.

Ready to move forward with confidence?

At Platinumcapitalfinancial, we work with homebuyers and real estate investors across Naples and Collier County who want a lender that explains the process, not just hands you a stack of papers. Our team walks you through every document, answers every question before closing day, and makes sure your file is complete from day one to avoid the delays that come from missing or incorrect paperwork.

If you are ready to apply or just want to understand what your mortgage loan options look like in Florida, we are here to help. Working with a knowledgeable mortgage broker means fewer surprises at the closing table and a smoother path to getting your loan funded on time.

FAQ

What does the role of mortgage documents include?

Mortgage documents define the legal and financial terms of your home loan, protect both borrower and lender rights, and satisfy federal compliance requirements such as TRID and HMDA disclosure rules.

What are the main types of mortgage documents?

The core documents are the mortgage or deed of trust, the promissory note, the Closing Disclosure, the Loan Estimate, and supporting verification records like tax returns, pay stubs, and bank statements.

How long should you keep mortgage documents?

You should keep key mortgage documents for the life of the loan plus up to seven years after payoff to support tax filings, refinancing applications, and any potential disputes with your servicer.

What happens if mortgage documents have errors?

Missing signatures or incorrect data can delay loan funding, put your locked interest rate at risk, and in some cases require a new closing appointment to correct the issue before the lender releases funds.

When must a lender send the Loan Estimate?

Under TRID regulations, lenders must deliver the Loan Estimate within three business days of receiving your completed mortgage application, giving you time to compare loan offers before committing.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)