Business

Why mortgage rates fluctuate: a Florida homebuyer's guide

You’ve probably heard someone say “the Fed cut rates, so mortgages should be cheaper now” — and then watched your rate quote stay exactly the same or even go up. That confusion is incredibly common, and it costs homebuyers real money. Understanding why mortgage rates fluctuate means looking past the headlines and into the bond market, inflation data, and lender behavior that actually move the numbers you see on your loan estimate. If you’re buying a home in Florida right now, this guide gives you the real picture.

Table of Contents

- How mortgage rates relate to Treasury yields and inflation

- The lender's spread and how credit risk affects your mortgage rate

- Why Federal Reserve actions don't directly set mortgage rates

- How geopolitical events and inflation affect mortgage rate volatility in 2026

- Practical tips for Florida homebuyers to navigate mortgage rate fluctuations

- The overlooked truth about mortgage rates no one tells Florida homebuyers

- Explore mortgage loan options tailored for Florida homebuyers

- Frequently asked questions

Key Takeaways

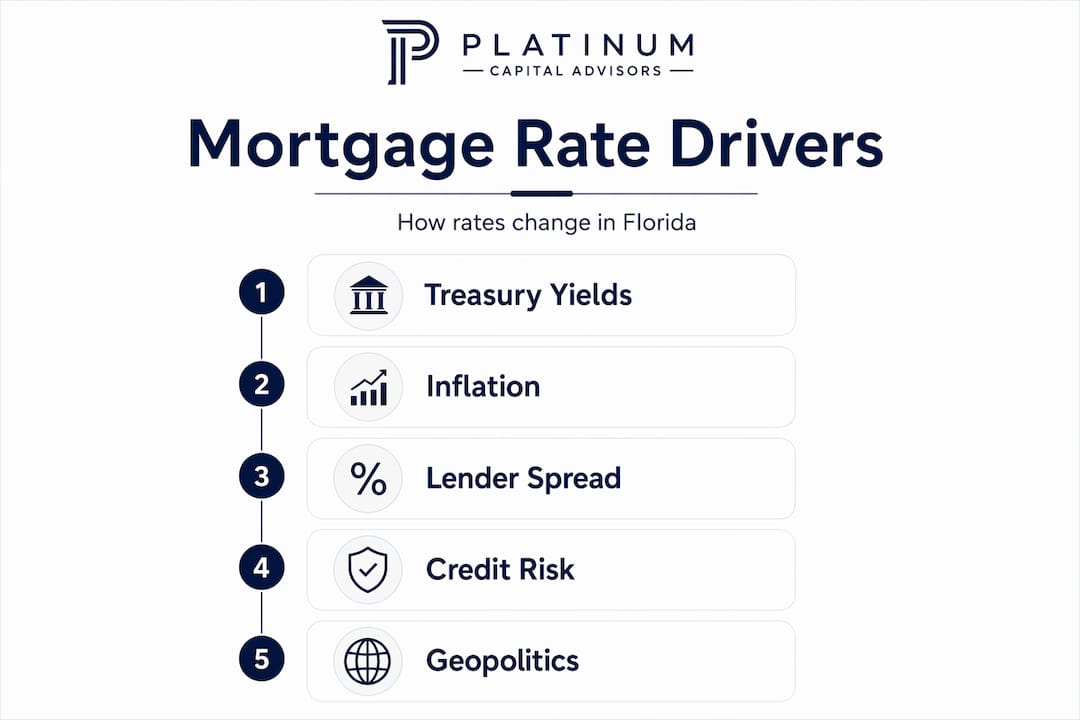

How mortgage rates relate to Treasury yields and inflation

Mortgage rates don’t come from Washington. They come from Wall Street, specifically from the bond market. Mortgage rates are primarily driven by the 10-year U.S. Treasury yield, which reflects what investors expect from inflation and economic growth over the next decade.

Here’s the logic: when investors worry about inflation eating into their returns, they demand higher yields on long-term bonds. Mortgage lenders price their loans based on those same yields, so when Treasury yields climb, so do mortgage rates. It’s a direct chain reaction, not a government decision.

The Consumer Price Index (CPI) is the number to watch. In early 2026, energy prices climbed sharply, partly due to geopolitical instability, and that pushed CPI higher. Investors responded by demanding better compensation on long-term bonds, and mortgage rates felt that pressure quickly.

Key inflation and rate drivers to monitor:

- CPI readings released monthly by the Bureau of Labor Statistics

- Energy prices, especially oil and natural gas, which feed directly into inflation

- Employment data, since strong job growth can signal rising wages and spending (which fuels inflation)

- Federal Reserve statements about future inflation expectations

If you’re shopping for mortgage loans in Naples Florida or anywhere across the state, keeping an eye on CPI release dates can help you understand why your rate quote changed between last Tuesday and today.

Pro Tip: Sign up for free CPI alerts through the Bureau of Labor Statistics website. When inflation comes in higher than expected, expect mortgage rates to move up within days, sometimes hours.

The lender’s spread and how credit risk affects your mortgage rate

Once you understand the Treasury yield as the foundation, the next piece is the spread. Lenders add a spread typically between 1.5% and 2.5% on top of the Treasury yield to cover their risk and make a profit. That spread is not fixed. It expands when lenders feel nervous about the economy and tightens when competition among lenders is fierce.

Two borrowers could get completely different rate quotes on the same afternoon, not because of anything the Fed did, but because their individual risk profiles tell lenders very different stories.

Borrower factors that shape your final mortgage rate:

- Credit score: A score above 760 consistently earns the lowest available rates. Below 680, expect your rate to climb noticeably.

- Down payment: Putting 20% or more down eliminates private mortgage insurance and signals lower default risk to lenders.

- Loan-to-value ratio (LTV): The lower your LTV, the less exposure the lender carries. Lower exposure means lower rate.

- Debt-to-income ratio (DTI): Lenders want to see your total monthly debt payments at or below 43% of your gross income.

*Estimates based on early 2026 market conditions with a 10-year Treasury near 4.5%.

Pro Tip: Before you start seriously shopping for a home in Florida, pull your credit report and resolve any errors. A 20-point score increase can drop your rate by 0.25% or more, which adds up to thousands of dollars over the life of the loan.

Explore your Florida mortgage loans options with a clear picture of where your credit profile puts you in this table. Knowing your tier before you apply prevents unpleasant surprises.

Why Federal Reserve actions don’t directly set mortgage rates

This is the misconception that trips up most homebuyers. The Federal Reserve controls the federal funds rate, which is the overnight lending rate between banks. That rate influences your credit card APR and home equity line of credit. It does not set your 30-year fixed mortgage rate.

Mortgage rates do not move in lockstep with the federal funds rate. They follow the 10-year Treasury yield, which is priced by bond market investors based on where they think inflation and economic growth are headed over years, not days.

Here’s what makes this confusing: the market often anticipates Fed decisions months in advance. By the time the Fed actually cuts rates, that expectation is already baked into Treasury yields. If the economy still looks inflationary, bond investors might push yields higher even as the Fed eases, pulling mortgage rates up rather than down.

How the Fed indirectly influences mortgage rates:

- Fed rate decisions shift expectations about future inflation

- Investors adjust long-term bond yields based on those expectations

- Mortgage lenders reprice loans based on where Treasury yields land

- Market-wide confidence also affects the spread lenders charge above Treasury yields

“The relationship between Fed policy and mortgage rates is indirect and often counterintuitive. Investors in the bond market are constantly recalibrating their expectations, and those expectations can diverge sharply from what the Fed is actually doing with short-term rates.” — Mike Fratantoni, Chief Economist, Mortgage Bankers Association

Florida mortgage lending insights from experienced local brokers reflect this reality. A broker who understands bond market dynamics can help you interpret rate movements rather than just react to them.

How geopolitical events and inflation affect mortgage rate volatility in 2026

The world outside your home purchase matters enormously to your mortgage rate. In early 2026, the conflict in Iran drove oil prices higher. That energy spike fed directly into CPI inflation, which reached 3.3% year-over-year in March 2026, well above the Federal Reserve’s 2% target. Bond investors responded by demanding higher yields, and mortgage rates climbed with them.

The 30-year fixed rate fluctuated between 6.09% and 6.57% across early 2026. That nearly half-point swing represents a significant monthly payment difference on a Florida home purchase.

How a geopolitical event becomes a higher mortgage rate:

- A conflict or supply disruption pushes oil and energy prices higher.

- Energy costs feed into the CPI, raising the official inflation reading.

- Bond investors demand higher yields to preserve their real returns against inflation.

- The 10-year Treasury yield rises.

- Mortgage lenders, who price off the Treasury yield, raise their base rates.

- Market uncertainty causes lenders to widen their spread further, compounding the increase.

- Borrowers see a higher rate on their loan estimate.

That entire chain can happen within days. Florida homebuyers shopping in a volatile stretch of the market are not imagining things when rates change from week to week. The market is genuinely responding to real global events.

When you’re looking at mortgage options in Florida during a period of geopolitical tension, building in a buffer for rate movement is smart planning, not pessimism.

Practical tips for Florida homebuyers to navigate mortgage rate fluctuations

You can’t control what happens in Iran or what the bond market does on a Tuesday morning. But you can control several things that have an equally large impact on the rate you actually pay.

Shopping three or more lenders can save 0.25 to 0.50 percentage points on your rate. That’s more money than most homebuyers gain by trying to time the market. It’s also more reliable. Experts consistently recommend focusing on long-term affordability rather than chasing short-term rate swings that can reverse overnight.

What Florida homebuyers can do right now:

- Get quotes from at least three lenders on the same day, since rates change daily and comparing across different days distorts the picture

- Ask each lender for a Loan Estimate, which gives you a standardized format for comparing costs side by side

- Watch Treasury yield trends rather than news headlines about the Fed

- Consider a rate lock once you have a contract, especially in volatile stretches like early 2026

- Keep your credit utilization below 30% in the months leading up to application to maximize your score

Rate lock timing matters. If Treasury yields have been falling steadily and CPI is coming in below expectations, locking early could cost you. If yields are climbing and inflation data is running hot, locking the moment you’re in contract protects you.

Pro Tip: Trying to time mortgage rates the way you might time a stock purchase almost never works. The most reliable path to a better rate is shopping multiple lenders and showing up with strong credit and a solid down payment. Those two things are within your control. The bond market is not.

Explore your Florida mortgage loan options with the perspective that preparation beats prediction every single time.

The overlooked truth about mortgage rates no one tells Florida homebuyers

Here’s a perspective most people won’t offer: 2026 is not a market where waiting pays off. A growing view among housing economists is that the U.S. mortgage market is in a “stuck rate” environment, where rates are unlikely to move materially higher or lower for the foreseeable future. Persistent inflation and geopolitical uncertainty have created a floor. The Fed’s caution prevents a ceiling from dropping fast either.

What this means practically: homebuyers who are waiting for rates to fall back to 5% or below are making a speculative bet against a market that has already priced in those expectations. That bet has been losing for longer than most people expected.

The more productive question isn’t “when will rates drop?” It’s “how do I get the best rate available to me right now?” Those are very different questions, and the second one actually has answers you can act on.

“Rate forecasts have consistently been wrong in both directions since 2022. Borrowers who built financial flexibility into their loan choices have generally fared better than those who delayed in hopes of a better market.” — Housing economist commentary, Mortgage Bankers Association conference, 2026

Lender competition is also real and underused. In a market where many buyers are sitting on the sidelines, lenders are competing more actively for qualified borrowers. That means spreads can vary meaningfully from lender to lender, and a borrower who shops aggressively can find rates that don’t reflect the most pessimistic headline numbers.

Pro Tip: Before you call a lender, run your own numbers. Know your credit score, your approximate LTV, and your DTI. Walk into that conversation as an informed buyer and you’ll negotiate differently. Lenders respond to prepared borrowers. Learn more about Florida mortgage options and pricing to approach that conversation from a position of knowledge.

Explore mortgage loan options tailored for Florida homebuyers

Understanding why mortgage rates fluctuate puts you ahead of most buyers walking into a lender’s office. Now the goal is finding a lender who matches that understanding with real options suited to your situation.

Platinum Capital Financial works with Florida homebuyers across a range of credit profiles and down payment levels, offering mortgage loan options that account for the rate environment you’re actually navigating, not a hypothetical one. Whether you’re a first-time buyer in Naples or refinancing in Miami, getting a personalized rate quote from a local broker means your numbers reflect current Florida market conditions, not national averages. Start the conversation early. The more time you have to compare options and strengthen your profile, the better position you’re in when it’s time to lock. Explore your loan options at mortgage loans in Naples Florida and get guidance built around your specific goals.

Frequently asked questions

What causes mortgage rates to fluctuate so often?

Mortgage rates fluctuate mainly because bond investors continuously adjust yields based on inflation expectations, economic growth forecasts, and geopolitical events. Rates are driven primarily by the 10-year Treasury yield, not directly by Federal Reserve decisions.

Does the Federal Reserve lowering rates mean mortgage rates will drop?

Not necessarily. Mortgage rates follow long-term Treasury yields, which respond to inflation outlooks and can move in the opposite direction of a Fed rate cut if investors remain concerned about inflation.

How can I get the best mortgage rate as a Florida homebuyer?

Shop multiple lenders for competing quotes, maintain a strong credit score, save for a meaningful down payment, and lock your rate when market conditions align with your timeline. Shopping three or more lenders can save 0.25 to 0.50 percentage points on your rate.

Why do mortgage rates sometimes rise even when the Treasury yield stays flat?

Lenders widen the spread over Treasury yields during periods of market uncertainty or elevated credit risk, which pushes mortgage rates higher independent of what Treasury yields are doing.

What impact do geopolitical events have on mortgage rates?

Geopolitical conflicts can drive energy prices higher, feeding inflation and prompting bond investors to demand better yields. Geopolitical tensions led to spiked oil prices in 2026 that increased inflation and pushed mortgage rates upward across the market.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)