Business

The Real Role of Loan Applications for Home Buyers

Most people treat a loan application like a formality. Fill in your name, paste in your income numbers, hit submit, and wait. But the role of loan application goes far deeper than paperwork. It is the single most important document your lender uses to decide whether you get the keys to your next home or investment property, and on what terms. Get it right, and you unlock competitive rates and faster approvals. Get it wrong, and you face delays, denials, or a loan that costs you thousands more than it should.

Table of Contents

- Key Takeaways

- The role of loan applications in home financing

- How lenders evaluate your application

- Paper applications vs. digital applications

- Steps to prepare and fill out your loan application

- My take on what most borrowers get wrong

- Work with Platinumcapitalfinancial on your Florida mortgage

- FAQ

Key Takeaways

The role of loan applications in home financing

When you apply for a mortgage, you are not just asking for money. You are handing a lender a complete financial portrait and asking them to trust it. The loan application process is the structured framework lenders use to capture that portrait. Every section, from your Social Security number to the address of the property you want to buy, feeds directly into a risk decision.

This matters more for real estate loans than for almost any other loan type. Property values are high, loan terms stretch across decades, and the financial consequences of a wrong lending decision are enormous for both sides. That is why the importance of loan applications in this context cannot be overstated. Your application is not just a form. It is your case.

What lenders actually look for in your application

A standard mortgage application collects several layers of information:

- Personal identification. Your full legal name, current address, Social Security number, and date of birth. Even a single digit error in your SSN can trigger a verification failure.

- Employment and income. Lenders want to see stable, verifiable income. W-2s, recent pay stubs, and two years of tax returns are standard. If you are self-employed or have rental income from investment properties, expect additional scrutiny.

- Credit history. Your credit score is pulled directly, but lenders also review the full report for missed payments, outstanding balances, and the age of your accounts.

- Assets and liabilities. Bank statements, retirement accounts, and investment holdings prove you can cover a down payment and reserves. Outstanding debts factor directly into your debt-to-income ratio.

- Property details. For real estate loans, the property address, estimated value, and intended use (primary residence versus investment) all affect underwriting decisions.

Pro Tip: Before you submit anything, compile all your financial documents into a single folder. Bank statements, tax returns, pay stubs, and your most recent mortgage statement if you own property already. Lenders increasingly use automated bank statement analysis to verify income, and inconsistent deposit patterns can raise red flags even when your credit score looks great.

How lenders evaluate your application

Once your application is submitted, it moves into underwriting. This is where the loan application requirements you filled out get stress-tested against real data. Understanding this step changes how you prepare.

The first thing lenders do is verify your identity through Know Your Customer (KYC) checks. Your name, address, and SSN are matched against official databases. From there, a hard credit inquiry is pulled. A hard inquiry reduces your FICO score by 5 to 10 points. It sounds minor, but if your score is sitting right on the edge of a pricing tier, that small drop could shift your interest rate.

The debt-to-income ratio, known as DTI, is one of the most decisive factors in the entire review. Your DTI ratio directly shapes whether a lender approves your loan and at what price. Most conventional mortgage lenders want to see a DTI below 43%. Investment property loans often require lower ratios because the income from those properties is viewed as less reliable than a salary.

Here is the actual sequence of what happens after submission:

- Data normalization. Your application fields are matched against official records. Mismatches trigger flags and slow everything down.

- Automated underwriting. Automated engines evaluate hundreds of data points from your file: credit lines, payment history, income trends, and debt patterns. Most decisions at major lenders are automated.

- Manual review. When the automated system cannot reach a confident decision, a human underwriter steps in. This typically happens with borderline DTI ratios or unusual credit patterns.

- Conditional approval. Most borrowers receive a conditional approval first. This means the loan is approved pending specific items, like an updated pay stub or a property appraisal.

- Final approval and closing. Once conditions are met, the file moves to final approval and then to closing.

“Credit scores are not the sole predictor of loan approval. Stable income and consistent payment patterns weigh heavily in lender decisions.” —

Common reasons applications stall or get denied include income that cannot be verified, debts the borrower did not disclose, and errors in personal data. Documentation errors like mismatched SSNs are among the most frequent causes of delays, and they are entirely preventable.

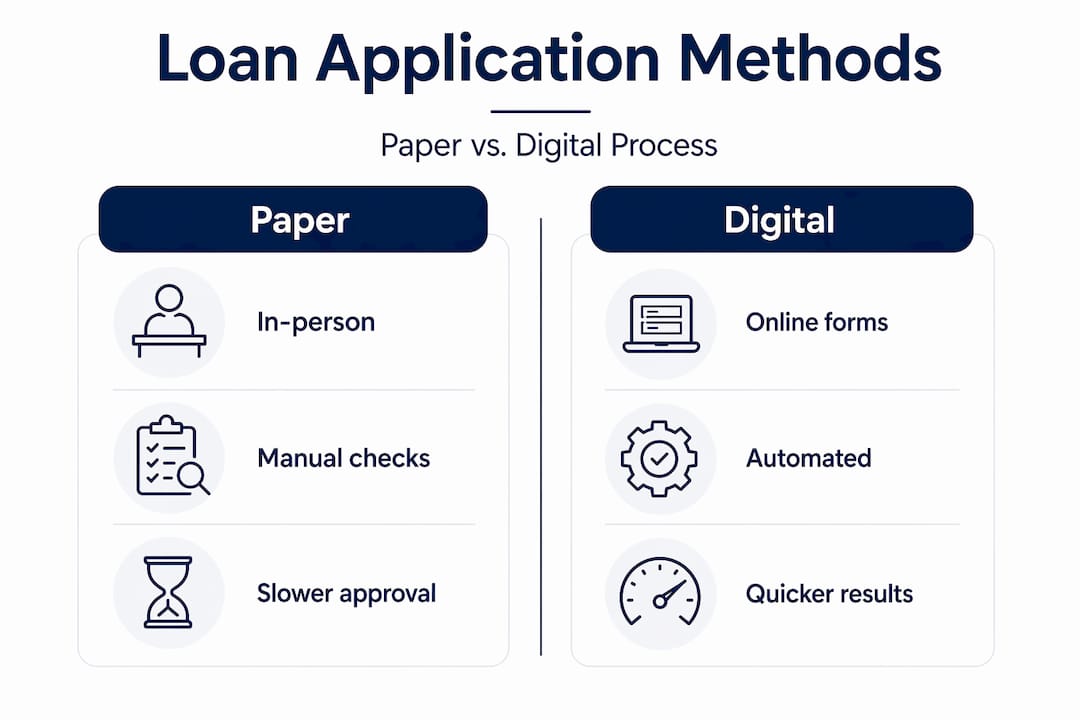

Paper applications vs. digital applications

The difference between a traditional paper application and a modern digital submission is not just convenience. It changes the entire timeline of your loan.

For mortgage loans specifically, digital applications have compressed timelines dramatically. That said, complex real estate transactions and investment property purchases often still require human review at some stage, so planning for two to four weeks from application to closing is realistic for most Florida borrowers.

One benefit of the digital process is that prequalification has become much easier. A soft credit pull during prequalification does not affect your score at all, and prequalifying before applying can save the average borrower thousands over the life of a loan by allowing real rate comparisons before you commit.

Pro Tip: If you plan to shop multiple lenders, submit all your formal applications within the same 14-day window. FICO treats all mortgage inquiries in that period as a single inquiry, so you protect your score while still comparing offers.

Steps to prepare and fill out your loan application

The difference between a strong application and a weak one usually comes down to preparation, not luck. Here is how to approach the loan application process the way experienced buyers do:

- Pull your own credit report first. Review it for errors before any lender sees it. Dispute anything inaccurate at least 60 days before you plan to apply.

- Calculate your DTI before you apply. Add up all monthly debt payments, divide by your gross monthly income. If you are above 43%, pay down revolving debt before submitting.

- Gather documents in advance. Two years of W-2s or tax returns, 60 days of bank statements, recent pay stubs, and current mortgage or lease statements. For investment properties, include rental agreements and Schedule E forms.

- Match your application data exactly to your documents. If your W-2 lists your name as Robert and your application says Bob, that mismatch can slow your file.

- Prequalify with two or three lenders. This gives you a realistic rate range and tells you which lender's loan application requirements you can realistically meet.

- Be transparent about income variability. If you have freelance income, seasonal bonuses, or rental income, document it thoroughly rather than leaving it unexplained. Document completeness signals financial reliability to lenders.

Pro Tip: For investment property applications, have your property analysis ready alongside your personal financials. Lenders want to see that you understand the asset, not just that you can afford the down payment.

My take on what most borrowers get wrong

I have seen hundreds of loan applications cross the desk, and one pattern stands out above everything else. People do not treat the application as a first impression. They treat it like a tax return, something to just get through.

Here is what I have learned: a lender cannot see you, cannot hear your reasoning, and cannot give you the benefit of the doubt. All they have is the data you provide. When that data has a typo, a missing document, or an unexplained income dip, they have no choice but to pause the file and ask questions. Every pause adds days to your timeline and raises doubt.

What actually works is thinking like the underwriter before you apply. Ask yourself what questions your file will raise. Freelance income? Attach a client letter. A past late payment? Write a brief explanation. A large deposit in your bank account? Source it clearly. The borrowers I have seen get the best outcomes are not always the ones with perfect credit. They are the ones whose files are complete, consistent, and easy to approve.

The other mistake I see constantly is overapplying. People get anxious and submit applications to five or six lenders outside of a rate-shopping window, damaging their score right when they need it most. Focus matters. Prepare once, apply strategically, and let a knowledgeable mortgage broker help you target the right lenders for your specific financial profile.

Work with Platinumcapitalfinancial on your Florida mortgage

If you are buying a home or investment property in Naples or Collier County, the loan application process does not have to be a guessing game.

Platinumcapitalfinancial works with buyers across Florida to make the mortgage process clear, efficient, and focused on your actual goals. Whether you are a first-time buyer trying to understand what lenders need or an investor building a portfolio of rental properties, the team at Platinumcapitalfinancial guides you through every stage of your mortgage loan application with personalized support and competitive loan solutions tailored to the Florida market. Reach out today and find out exactly what your application needs to get approved.

FAQ

What is the role of a loan application in mortgage approval?

The loan application gives lenders the financial data they need to assess your creditworthiness, calculate your debt-to-income ratio, and determine what loan terms you qualify for. It is the foundation of every mortgage decision.

How does credit history affect my loan application?

Your credit history shows lenders how reliably you have managed debt. A strong history supports approval and better rates, but stable income and payment patterns also carry significant weight in the final decision.

What are the most common loan application mistakes?

The most frequent mistakes are data entry errors like mismatched SSNs, missing income documentation, and undisclosed debts. About 15 to 20 percent of applications contain errors that cause delays or denials.

Does applying to multiple lenders hurt my credit score?

Only if you space them out. Submitting mortgage applications within a 14-day window counts as a single FICO inquiry, so you can compare lenders without damaging your score.

What is the difference between prequalification and a formal loan application?

Prequalification uses a soft credit pull and provides an estimate of what you may qualify for. A formal application triggers a hard inquiry and starts the official underwriting process.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)