Business

Step-by-Step Home Loan Florida: 2026 Guide

Securing a home loan in Florida is a structured process that moves from financial preparation through closing, with each stage building on the last. The step by step home loan Florida process covers credit readiness, loan selection, pre-approval, underwriting, and a closing day that includes Florida-specific requirements like title insurance and the Homestead Exemption. This guide covers every milestone in order, with real numbers, named programs, and practical tips drawn from Florida’s actual market conditions. Whether you are buying your first home in Naples or refinancing in Orlando, the same core sequence applies.

How do you prepare financially for a florida home loan?

Financial preparation is the foundation of a smooth mortgage approval in Florida. Lenders evaluate your credit score, income stability, and debt load before they approve a single dollar. Getting these three factors in order before you apply saves time and money.

Start by pulling your free annual credit report from annualcreditreport.com. Review it for errors, unpaid collections, or accounts that are dragging your score down. Disputing errors before you apply can raise your score by 20–40 points, which directly affects your interest rate.

Budgeting for a Florida home requires more than a national mortgage calculator. Experts recommend the 28/36 budgeting rule: keep housing costs under 28% and total debt under 36% of your gross monthly income. Florida’s homeowners insurance market is volatile, and national online calculators routinely underestimate local premiums. Always use actual Florida insurance quotes when calculating your monthly payment.

Documents you need before applying

Florida lenders require a specific set of documents at application:

- W-2s and federal tax returns from the past two years

- Last 30 days of pay stubs

- Two months of bank statements

- Government-issued photo ID

- Gift letters if any portion of your down payment is a gift

Self-employed borrowers must also provide personal and business tax returns plus a year-to-date profit and loss statement. Gathering these documents before you contact a lender puts you days ahead of most buyers.

Pro Tip: Do not open any new credit cards, auto loans, or personal lines of credit in the 90 days before you apply. New credit inquiries lower your score and change your debt-to-income ratio, both of which can trigger a denial or a higher rate.

What mortgage loan options are available in florida?

Florida borrowers have access to five main loan categories, and choosing the right one affects your down payment, monthly cost, and long-term flexibility. The table below compares the core options.

The Florida Housing Finance Corporation offers down payment assistance programs and below-market interest rates for qualifying first-time buyers. These programs stack on top of FHA or conventional loans, reducing the cash you need at closing.

FHA loans require a minimum credit score of 580 for the 3.5% down payment option. They carry mortgage insurance premiums, but they remain the most common path for buyers with credit scores in the 580–650 range. You can review FHA loan eligibility details to see if you qualify.

VA loans are the strongest option for eligible veterans. They require no down payment and no private mortgage insurance. The Florida VA loan step by step process mirrors the standard VA process nationally, but Florida’s property appraisal timelines can run slightly longer in high-demand markets like Miami-Dade and Broward counties.

USDA loans cover more of Florida than most buyers realize. Large portions of Central and North Florida qualify as rural under USDA definitions. Florida USDA mortgage loans offer zero-down financing for buyers in eligible zip codes.

For refinancing, the loan type choice carries an extra consideration. Refinancing with your original lender in Florida can avoid documentary stamp and intangible taxes that typically add $1,500–$3,000 in costs when you switch lenders. That tax difference can outweigh a slightly better rate from a new lender.

If you prefer payment stability, a fixed-rate mortgage locks your rate for the life of the loan. If you plan to sell or refinance within 5–7 years, an adjustable-rate mortgage may offer a lower initial rate.

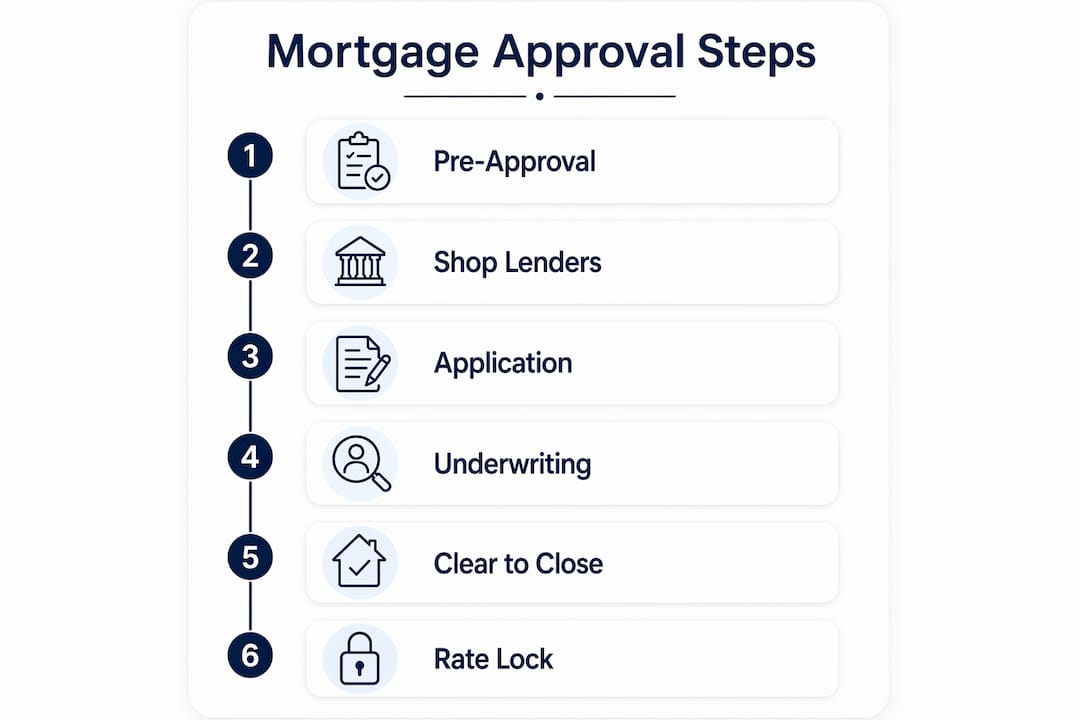

What is the step-by-step mortgage approval process in florida?

The step by step mortgage approval Florida process follows a defined sequence. Understanding each phase prevents surprises and keeps your closing on schedule.

Step 1: Get Pre-Approved

Pre-qualification is a soft estimate based on self-reported numbers. Pre-approval is a formal review with a hard credit pull and verified income and assets. Florida sellers disregard pre-qualification letters in competitive markets. Pre-approval is the only document that signals you are a serious buyer.

Step 2: Shop at Least Three Lenders

Lender fees including origination, appraisal, underwriting, and title services vary widely. Shopping among at least three lenders can save $5,000–$15,000 over the life of a loan. Compare APRs, not just interest rates, because APR includes fees that the base rate hides.

Step 3: Submit Your Full Application

Once you have a signed purchase contract, submit your complete loan application with all required documents. Your lender issues a Loan Estimate within three business days. Review every line item, because origination fees are negotiable and buyers can save 25–50% by pushing back on those charges.

Step 4: Underwriting and Appraisal

Underwriting typically takes 2–4 weeks. The appraiser confirms the property value supports the loan amount. Florida’s AS-IS contract structure means appraisal contingencies are not automatic. You must negotiate them explicitly into your contract to protect yourself if the appraisal comes in low.

Step 5: Clear to Close

The full Florida closing timeline runs 30–60 days from contract to closing. Underwriting accounts for 2–4 weeks of that window. Every day you delay responding to a document request adds an equal day to your closing date. Speed during underwriting is the single most controllable factor in your timeline.

Step 6: Lock Your Rate

Rate locks typically last 30–60 days. Lock too early and you may pay a fee to extend. Lock too late and rates may move against you. Watch the 10-year Treasury yield as a leading indicator of mortgage rate direction in Florida’s market.

Pro Tip: Respond to every underwriter request within 24 hours. Borrowers who treat document requests as urgent close on time. Those who treat them as optional routinely push their closing date back by a week or more.

How does the closing process work in florida?

Florida’s closing process has several steps that differ from other states, and knowing them in advance prevents last-minute surprises.

- Review the Closing Disclosure: Your lender must deliver this document at least three business days before closing. Compare every fee to your original Loan Estimate. Flag any new charges or increases above the allowed tolerance limits.

- Final walkthrough: Conduct this 24 hours before closing to confirm the property condition matches the contract. Document any issues in writing before you sign.

- Title insurance: Florida sellers traditionally pay for the owner's title insurance policy in most counties, though this is negotiable. The buyer pays for the lender's title policy. Review the Florida closing process details to understand exactly what each party covers.

- Closing day documents: Bring your government-issued ID, a certified or cashier's check for closing costs, and proof of homeowners insurance. Wire fraud is common in Florida real estate. Always verify wire instructions by phone with your title company before sending funds.

- File the Homestead Exemption: The Florida Homestead Exemption must be filed by March 1 of the year following your purchase. Missing this deadline means waiting a full year for the property tax savings. Set a calendar reminder the day you close.

Key takeaways

A successful Florida home loan requires financial preparation, the right loan program, fast document responses during underwriting, and attention to Florida-specific closing requirements.

What i’ve learned after years of florida mortgage deals

The single biggest mistake I see Florida buyers make is treating the mortgage process as a background task while they focus on house hunting. The loan is the transaction. The house is the result.

Two things consistently separate buyers who close on time from those who don’t. First, the buyers who close on time have their documents ready before they need them. They are not scrambling for a 2024 tax return the week underwriting opens. Second, they respond to lender requests the same day. I have watched closings slip by two weeks because a buyer waited three days to send a bank statement.

On lender shopping: most buyers contact one lender, get a quote, and move forward. That is the most expensive decision in the process. Comparing three lenders takes two hours and can save you more money than a year of skipping vacations. The difference in origination fees alone is often $2,000–$4,000 on a typical Florida purchase.

Florida’s insurance market deserves its own conversation. I have seen buyers budget $150 per month for homeowners insurance based on a national calculator, then discover the actual quote is $400 per month. That gap can push your debt-to-income ratio over the lender’s limit and kill the deal. Get real quotes from Florida-licensed insurers before you make an offer.

Finally, the Homestead Exemption is free money that a surprising number of new Florida homeowners miss. File it. Do it the week after closing if you can.

— Chuck Barnes

Work with Platinumcapitalfinancial on your florida home loan

Platinumcapitalfinancial works with Florida homebuyers and homeowners every day, from first-time purchases to step by step mortgage refinancing Florida situations where the numbers need to work harder.

As a Florida mortgage broker, Platinumcapitalfinancial compares loan options across multiple lenders so you get the best available rate and terms for your situation. Whether you need an FHA loan in Collier County, a VA loan, a USDA program, or a conventional purchase loan, the team matches you to the right program and walks you through every step. Contact Platinumcapitalfinancial to start your pre-approval, compare lenders, and move toward closing with a clear plan and no surprises.

FAQ

What credit score do you need for a florida home loan?

Most conventional Florida lenders require a minimum score of 620, while FHA loans accept scores as low as 580 with a 3.5% down payment. VA and USDA loans have no official minimum but most lenders set a practical floor of 580–620.

How long does the florida mortgage process take?

The full timeline from pre-approval to closing typically runs 2–6 months, with the contract-to-closing window averaging 30–60 days. Underwriting alone takes 2–4 weeks, and delays in document submission extend that window day for day.

What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate based on self-reported data. Pre-approval involves a hard credit pull and verified income and assets, and it is the only letter Florida sellers treat as credible in competitive markets.

Can first-time buyers in florida get down payment help?

Yes. The Florida Housing Finance Corporation offers down payment assistance programs that pair with FHA or conventional loans, reducing the upfront cash required at closing for qualifying first-time buyers.

Does refinancing in florida cost more than in other states?

Refinancing with a new lender in Florida triggers documentary stamp and intangible taxes that typically add $1,500–$3,000 to closing costs. Refinancing with your original lender avoids most of these charges, making it the financially smarter path in many cases.

Recommended

- What Is the Home Loan Process: A 2026 Guide

- Florida Home Loan Approval Workflow: 2026 Guide

- How to Apply for a Mortgage in Florida: 2026 Guide

- Florida first-time homebuyer mortgage guide: your roadmap

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)