Mortgage News

Mortgage term explained: A clear guide for Florida buyers

Buying your first home in Florida is exciting, but mortgage paperwork can stop you cold when you hit terms you don’t fully understand. Many first-time buyers assume the “mortgage term” simply means how long they’ll be paying off their home loan. That assumption is mostly right for standard loans, but it can be dangerously wrong for others. Confusing mortgage term with loan amortization has caused real buyers to face unexpected lump sum payments they weren’t prepared for. This article breaks down exactly what mortgage term means, how different term lengths affect your wallet, and what questions to ask before you sign anything.

Table of Contents

- Defining mortgage term: What it really means

- How mortgage term length affects your payments and choices

- Balloon mortgages and hidden term surprises

- Essential questions to ask about your mortgage term

- What most first-time buyers miss about mortgage terms

- How we help Florida buyers make smart mortgage choices

- Frequently asked questions

Key Takeaways

Defining mortgage term: What it really means

A mortgage term is the specific period during which your loan agreement is in effect under its current rules, interest rate, and payment schedule. Think of it as the active contract window for your loan. When the term ends, the loan either reaches full payoff or you owe whatever balance remains.

This is not the same as amortization, which is the total timeline used to calculate how your payments chip away at the loan principal over time. For most standard home loans in Florida, these two numbers match perfectly. A 30-year fixed-rate mortgage has a 30-year term and a 30-year amortization schedule. Done. But that tidy match doesn’t always exist, and that’s where buyers get into trouble.

Here’s a quick breakdown of the two concepts:

- Mortgage term: The length of the current loan contract, when your interest rate and payment terms apply

- Amortization period: The full schedule for paying down your loan principal to zero

- Standard alignment: On a 15 or 30-year fixed loan, term and amortization are the same

- Nonstandard structure: On balloon loans or certain program structures, the term can be much shorter than amortization

As

, a loan can have a shorter contract term than the amortization schedule, such as in balloon mortgages or certain program structures. This distinction is critical for any buyer who doesn’t want a surprise bill at the end of their loan period.

In the United States, the most common mortgage terms are 15 years and 30 years. Some lenders also offer 20-year or 10-year options. For most Florida buyers using a conventional fixed-rate loan, the term and amortization will be the same. But the moment you step outside that standard structure, you need to slow down and ask questions.

If you’re exploring mortgage loans in Naples or anywhere in Florida, understanding this distinction before you compare loan offers is essential. Not every loan product is structured the same way, and a lower monthly payment doesn’t always tell the whole story.

How mortgage term length affects your payments and choices

With a clear definition in mind, it’s important to see how your choice of mortgage term directly influences your finances. The term you choose is one of the most powerful levers you have over your monthly payment and the total amount of interest you’ll pay over the life of the loan.

Fixed-rate mortgages keep the interest rate consistent for the entire life of the loan, which means the term directly determines how long those payments last before the loan is fully repaid or refinanced. This predictability is a major reason why fixed-rate loans remain the most popular choice among Florida first-time buyers.

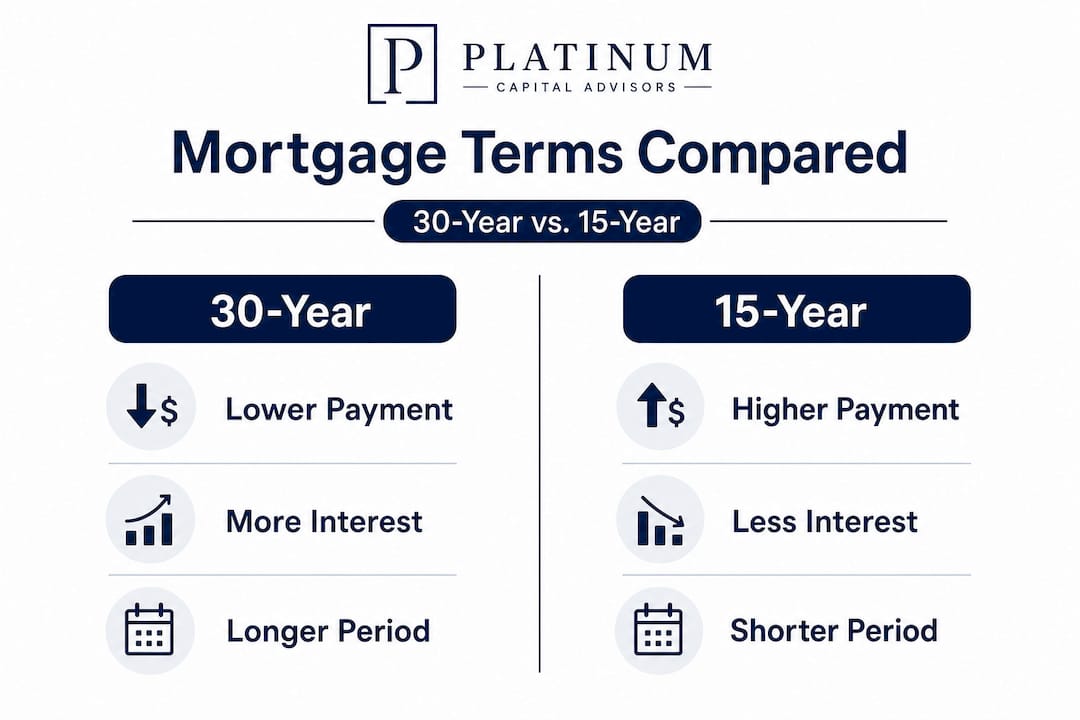

Here’s a comparison of common term options based on a $350,000 home loan at a hypothetical 6.75% interest rate:

The numbers tell a clear story. A 30-year term saves you about $830 per month compared to a 15-year term. But you’ll pay roughly $259,000 more in interest over time. That’s a significant financial trade-off.

Here’s how to think through which term fits your situation:

- Assess your monthly budget first. A 15-year loan saves you a large amount in interest, but only if you can comfortably make the higher payments each month without stretching your finances too thin.

- Consider your income stability. If your income varies or you're early in your career, the flexibility of a lower 30-year payment can provide a safety net.

- Factor in your long-term goals. Planning to stay in the home for decades? A shorter term accelerates equity building. Thinking you may move in 7 to 10 years? A longer term may preserve more cash flow for other goals.

- Look at Florida-specific programs. Some state housing assistance programs are designed around specific loan term structures, so reviewing all mortgage options available in Florida matters before you commit.

One important point many buyers overlook: a shorter term doesn’t just mean higher payments. It also often comes with a lower interest rate. Lenders typically offer better rates on 15-year loans because they carry less repayment risk. So the real savings are even greater than the table above suggests.

Balloon mortgages and hidden term surprises

Not every mortgage works the same way. Let’s look at situations where the stated term could leave you owing more than you expect.

A balloon mortgage is a loan structure where you make regular payments for a set number of years, but the loan is not fully paid off by the end of that term. Instead, a large lump sum called the balloon payment becomes due. As Investopedia confirms, a loan can have a shorter contract term than the amortization schedule, which is exactly what happens in balloon mortgage structures.

Here’s a real-world scenario to illustrate the risk:

Example: You take out a balloon mortgage with a 7-year term but a 30-year amortization. Your payments for 7 years are calculated as if you have a 30-year loan, keeping them relatively affordable. But at the end of year 7, the remaining balance (which is still substantial because you’ve only paid down 7 years’ worth of a 30-year schedule) becomes due in full.

For a first-time buyer in Florida, this structure is dangerous if you’re not planning for it. Most balloon mortgage borrowers plan to either sell the home or refinance before the balloon payment comes due. But life doesn’t always cooperate. Property values can drop, your credit score can change, and refinancing isn’t always guaranteed.

Pro Tip: Before you agree to any mortgage, ask your lender directly: “Will this loan be fully paid off by the end of the stated term, or will a balance remain?” Get that answer in writing. If a balance remains, find out exactly how much and what your options are.

Beyond balloon loans, some government or specialized program loans can include deferred structures or interest-only periods that affect how much of your principal you’ve actually paid at any given point. If you want to dig deeper into how these loan structures work during the approval process, reviewing underwriting insights can help clarify what lenders look for and how loan structures are evaluated.

Essential questions to ask about your mortgage term

Having seen common structures and pitfalls, here’s how you can be proactive when discussing terms with your lender or broker. Walking into a loan conversation armed with the right questions separates buyers who close with confidence from those who discover surprises after the fact.

Always ask these questions before you sign your loan documents:

- Is this loan fully amortizing? A fully amortizing loan means your regular payments will bring the balance to exactly zero by the end of the term. If the answer is anything other than a clear yes, ask for a detailed explanation.

- When does the term officially end? Get the exact date. This matters for planning refinances, sales, or any major life event around your loan.

- What happens at the end of the term? For standard loans, the answer is simple: the loan is paid off. For balloon or non-standard loans, you need a specific plan.

- Is there any deferred interest or interest-only period? These structures can make payments look low early on while hiding how slowly you're building equity.

- What rate or terms will apply if I refinance at term end? If your loan has a shorter term than amortization, refinancing is often the plan. Know the conditions.

As Investopedia recommends, it’s worth confirming during underwriting whether the loan is fully amortizing to the end of the stated term or whether there is a balloon or deferred structure in place. Don’t assume your loan officer will volunteer this information unprompted.

Pro Tip: Always get written confirmation of the loan structure before closing. Ask for a loan summary document that clearly states whether the loan is fully amortizing and what the balance will be at term end. If the lender is reluctant to provide this clearly, that’s a red flag.

Understanding underwriting considerations specific to Florida can also give you a clearer picture of what documentation and loan structure details to request early in the process.

What most first-time buyers miss about mortgage terms

Here’s what guides rarely explain but can make all the difference: buyers tend to focus almost entirely on interest rate and monthly payment when comparing loans. Those are important numbers, but they don’t tell you what happens at the end of your loan contract. That’s the gap where expensive surprises live.

Conventional wisdom in the mortgage world says that a lower rate is always better. But a lower rate on a balloon mortgage can still leave you scrambling for a lump sum payment in 7 years if you haven’t planned for it. We’ve seen buyers come to us after committing to a loan structure they didn’t fully understand, genuinely believing their loan worked just like a standard 30-year mortgage.

The uncomfortable truth is that loan documents are dense and use language designed for legal precision, not reader clarity. Most buyers don’t read every line. That’s understandable. But the term structure section is one you genuinely can’t afford to skip.

What protects you isn’t just being smart. It’s asking the specific questions laid out in this guide and insisting on clear, written answers. A good mortgage broker won’t make you feel foolish for asking. In fact, a broker who welcomes those questions is one you can trust.

We also believe that buyers who explore real-life loan scenarios before committing to a loan type arrive at closing with far less stress. Understanding how different structures play out in real situations is genuinely protective.

The buyers who regret their mortgage choices almost always say the same thing: “I wish I had asked more questions before signing.”

How we help Florida buyers make smart mortgage choices

Understanding mortgage term structures is exactly the kind of knowledge that can save you from a costly mistake down the road. But knowing the concepts is only part of the journey.

At Platinum Capital Financial, we specialize in helping Florida buyers like you navigate the full range of mortgage term options, from standard 15 and 30-year fixed loans to more complex structures. We take time to walk through your specific loan’s amortization, term end scenarios, and payment structure so you know exactly what you’re signing. If you’re ready for expert Florida mortgage guidance tailored to your situation, our team is here to help you close with confidence and clarity.

Frequently asked questions

Is mortgage term the same as loan amortization?

No, the mortgage term is the agreed length of your contract, while amortization refers to how long it takes to pay off the loan in full. As Investopedia explains, a loan can have a shorter contract term than the amortization schedule, which is common in balloon mortgage structures.

What happens when my mortgage term ends?

If your loan is fully amortizing, it’s simply paid off at term end. But if there’s a remaining balance, as with a balloon mortgage structure, you’ll need to refinance or pay off that balance as a lump sum.

Can I change my mortgage term after closing?

You can’t directly change the term mid-loan, but you may refinance into a new mortgage with a different term. For fixed-rate mortgages, the term is locked in at closing, and refinancing is the primary way to adjust it.

Are shorter mortgage terms always better?

Not always. Shorter terms mean less total interest paid over the life of the loan, but they come with higher monthly payments. The right choice depends on your budget and financial goals. Fixed-rate loan terms should match both your current income and your long-term housing plans.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)