Business

Home inspections and mortgage loans: a Florida buyer's guide

Many Florida homebuyers assume that if the lender orders an appraisal, the home inspection is just optional paperwork. That assumption can cost you thousands. The truth is that home inspections and appraisals serve completely different purposes, and understanding that difference can change how smoothly your mortgage closes. Whether you are buying a waterfront condo in Naples or a single-family home in Fort Myers, knowing exactly how inspections fit into the loan process gives you a serious advantage.

Table of Contents

- What is a home inspection and why does it matter in loans?

- The role of home inspection in the loan approval process

- What to expect during a home inspection in Florida

- How to leverage your inspection report for loan approval

- The uncomfortable truth about home inspections and loans

- Trusted mortgage solutions for Florida homebuyers

- Frequently asked questions

Key Takeaways

What is a home inspection and why does it matter in loans?

A home inspection is a thorough, visual evaluation of a property’s physical condition. A licensed inspector examines the structure, mechanical systems, electrical wiring, plumbing, roofing, and more. The goal is to identify existing problems or potential safety hazards before you sign on the dotted line.

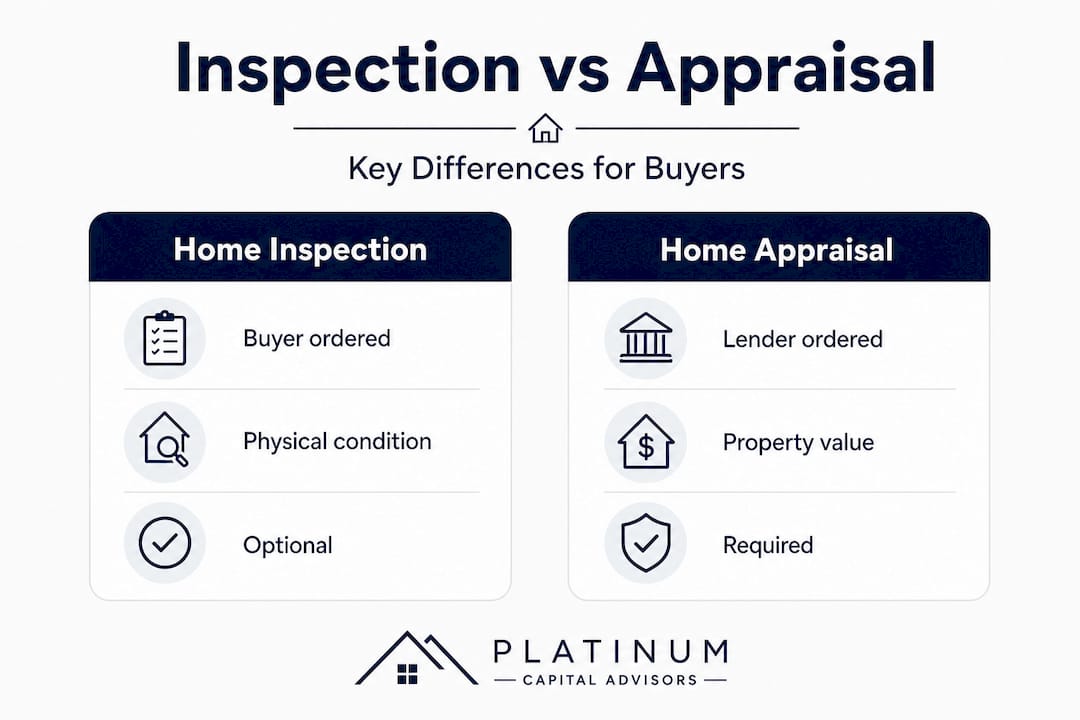

People confuse inspections with appraisals all the time. An appraisal determines the market value of the property so the lender knows how much to loan against it. An inspection tells you and your lender what condition the property is actually in. Both matter, but they answer very different questions.

Here is a quick look at what a typical Florida home inspector evaluates:

- Roof condition: Age, missing shingles, flashing integrity

- Foundation and structure: Cracks, settling, water intrusion signs

- Electrical systems: Panel condition, outdated wiring, GFCI outlets

- Plumbing: Pipe material, water pressure, signs of leaks

- HVAC systems: Age, condition, airflow, and filter status

- Windows and doors: Seals, operation, hurricane protection

- Pest and termite presence: Common in Florida's humid climate

Lenders care about inspections because a home in poor condition represents a financial risk. If you default on the loan, the lender needs to sell that property. A house with a failing roof or outdated electrical system will not sell easily or at full value.

Pro Tip: Ask your inspector for a verbal walkthrough while they work, not just a written report afterward. You will understand the findings much better, and you can ask specific questions about severity in real time.

The Naples mortgage loan process requires buyers to coordinate several steps, and knowing that the inspection is separate from the appraisal helps you plan your timeline without confusion. Skipping the inspection to save $300 to $500 is one of the costlier mistakes Florida buyers make each year.

The role of home inspection in the loan approval process

Understanding where the inspection fits in the overall mortgage timeline prevents delays and nasty surprises at closing. Here is the typical order of events for a Florida home loan:

- Pre-approval: Lender reviews your credit, income, and assets.

- Offer accepted: You sign a purchase contract with an inspection contingency built in.

- Inspection period: Usually 10 to 15 days in Florida. You hire an inspector and review findings.

- Appraisal: Lender orders this after the inspection contingency is resolved.

- Underwriting: Lender reviews all documents including any required repairs.

- Clear to close: Final approval issued, and closing is scheduled.

The type of loan you are getting dramatically changes how inspections affect approval. Conventional loans follow Fannie Mae and Freddie Mac guidelines, which do not technically require a home inspection. However, FHA and VA loans are different. FHA loans require that the property meet specific safety and livability standards, and the appraiser will flag issues that could trigger a mandatory inspection or repair demand. VA loans go even further, with the VA appraiser checking for minimum property requirements on behalf of the veteran borrower.

A statistic worth noting: according to real estate industry data, roughly 11% of home sales fall through due to inspection-related issues. That figure matters because it means one in nine deals hit a serious snag right at this stage. Buyers who understand what lenders need from the inspection report are far less likely to become part of that statistic.

The key distinction is between mandatory and optional inspections. Lenders using government-backed loan programs are bound by property standards. Private conventional lenders have more flexibility, but most experienced loan officers will strongly encourage you to complete a thorough inspection anyway. A missed structural defect can become the lender’s problem if the loan defaults and the house is worth less than expected.

Now that the timeline is clear, let’s look at what happens during a typical inspection and what buyers should expect.

What to expect during a home inspection in Florida

Florida has some unique inspection considerations that buyers from other states often overlook. The humid subtropical climate creates conditions that accelerate certain types of property damage. Mold, wood rot, termite activity, and hurricane-related wear are far more common here than in most other parts of the country.

Here is what a standard Florida home inspection looks like from start to finish:

- Scheduling: You hire a licensed Florida inspector, typically within two to three days of the offer being accepted. Cost ranges from $300 to $600 depending on home size.

- Day of inspection: The inspector spends two to four hours on site. You should attend in person whenever possible.

- Common Florida-specific findings: Flat or low-slope roof issues, older aluminum wiring, aging AC systems (Florida units work harder and wear out faster), signs of water intrusion around windows and sliding doors, and polybutylene or cast-iron plumbing in older homes.

- Report delivery: Most inspectors deliver a detailed written report with photos within 24 hours of the inspection.

- Review period: You and your real estate agent review the report and decide which issues to request the seller address before closing.

“In Florida, never skip the wind mitigation and 4-point inspection add-ons. Your insurance company will ask for them anyway, and combining them with your general inspection saves time and money before your mortgage closes.” This is advice that experienced Florida mortgage brokers share with nearly every buyer they work with.

Home inspection tips for Florida buyers often emphasize the “4-point inspection” specifically. This report covers the four systems that Florida insurance carriers scrutinize most: roof, electrical, plumbing, and HVAC. Many insurers will not issue a homeowner’s policy, which your lender requires, without a recent 4-point inspection on homes older than 25 years. Without insurance, there is no loan approval. It is a critical piece of the puzzle.

Pro Tip: If the inspector finds evidence of prior water damage, ask for a separate mold assessment. Mold remediation in Florida can run from $1,500 to $15,000 depending on the extent of the problem. Finding this before closing keeps you in a strong negotiating position and prevents a financial shock after you move in.

The inspection report is not a pass/fail document. It describes conditions ranging from minor maintenance recommendations to serious structural concerns. The challenge is knowing which findings your lender will flag as deal-breakers and which ones you can negotiate directly with the seller.

How to leverage your inspection report for loan approval

Receiving a lengthy inspection report full of red and orange flags can feel overwhelming. But buyers who approach that report strategically rather than emotionally consistently have better loan outcomes. Here is a step-by-step approach that works:

- Categorize findings by severity. Separate issues the lender will likely require to be fixed (safety hazards, structural problems, active leaks) from cosmetic items the lender does not care about (scuffed paint, dated fixtures).

- Share relevant findings with your loan officer immediately. Your loan officer can tell you whether specific issues could trigger an underwriting condition before you spend time negotiating. This saves days of back-and-forth.

- Submit a formal repair request to the seller. Work with your real estate agent to request that critical repairs be completed before closing, or ask for a credit toward your closing costs so you can handle repairs yourself.

- Get repair receipts and completion photos. Lenders do not take your word for it. Document every repair with permits when required, contractor invoices, and before-and-after photos.

- Order a re-inspection if major repairs were completed. For significant work, a re-inspection confirms the fix was done properly. The cost is typically $100 to $150 and it gives your lender, and you, peace of mind.

Mortgage negotiation strategies that work best are the ones that focus on lender requirements first, then personal preferences. Buyers sometimes make the mistake of asking sellers to fix every item in the inspection report, which can kill goodwill and stall negotiations. Focus on what matters to loan approval, then handle minor items after closing.

Industry data shows that buyers who proactively address lender-flagged inspection issues close on schedule at a significantly higher rate than those who leave issues unresolved until the final days before closing. Waiting creates panic, rushed contractor work, and paperwork delays. Addressing issues early gives everyone time to do things correctly.

Pro Tip: When requesting seller credits instead of repairs, frame the amount as the actual cost of the repair plus a 10% contingency buffer. Contractors in Florida are in high demand, and bids often come in higher than online estimates. Protect yourself by building a cushion into your credit request.

Having uncovered practical ways to use your inspection report, let’s step back and consider some deeper truths about home inspections and their impact.

The uncomfortable truth about home inspections and loans

Here is what most articles about home inspections will not tell you: the inspection is not really for your lender. It is for you. Lenders care about the property as collateral. You are the one who has to live in it for the next 20 or 30 years.

The problem we see repeatedly as Florida mortgage brokers is that buyers treat the inspection like a hurdle to clear for the lender, then move on. They focus on whether the lender will approve the loan rather than whether the home is actually a sound investment for their family. Those are two completely different questions.

A lender may approve a loan on a home with an aging roof because it is not technically a safety hazard yet. But you, as the buyer, might be looking at $18,000 to $25,000 in roof replacement costs within three to five years. Florida insurance companies are already pulling out of the state or dramatically raising premiums, and a roof over 15 years old can make your home nearly uninsurable at a reasonable rate.

Florida homebuyer advice from people who have worked hundreds of closings points to one consistent theme: the buyers who protect themselves best are the ones who use the inspection to make an independent, well-informed decision, not just a loan approval decision.

Treating inspections as a checkbox is a mindset that lenders actually encourage without realizing it, because lenders are thinking about risk over the next few years while you should be thinking about your family’s financial security over decades. Be smarter than the process. Use the inspection to understand exactly what you are buying, not just to satisfy the underwriter.

Trusted mortgage solutions for Florida homebuyers

Florida’s real estate market moves fast, and having an experienced mortgage broker in your corner makes the difference between a smooth closing and a stressful scramble. A knowledgeable broker helps you understand which inspection findings matter for your specific loan type, what lenders in Naples and Collier County typically require, and how to structure your offer and negotiations to protect your timeline.

If you are working through the home inspection process and want clear guidance on how it affects your loan approval, we are here to help. Our team at Platinum Capital Financial specializes in Florida mortgage loan services for buyers across Collier County and beyond. From your first pre-approval to your final closing disclosure, we walk you through every step so nothing catches you off guard.

Frequently asked questions

Is a home inspection required for mortgage loans in Florida?

Home inspections are strongly recommended but not always required for conventional loans in Florida. FHA, VA, and USDA loan programs have property condition standards that effectively make thorough inspections essential.

How does a home inspection affect loan approval?

Inspection findings affect approval when lenders identify safety hazards or structural issues that must be resolved before the loan can close. Buyers who address flagged items quickly keep their closing on schedule.

What happens if problems are found during a home inspection?

Significant problems may require seller repairs or credits before closing, and lenders may issue conditions tied to inspection findings that must be satisfied before final approval is granted.

Can I use the inspection report to negotiate my mortgage terms?

You can use the report to negotiate repairs or credits with the seller, which reduces your out-of-pocket costs after closing. The report itself does not directly change your interest rate or loan amount.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)