Business

How to Prepare for Mortgage Closing: 2026 Guide

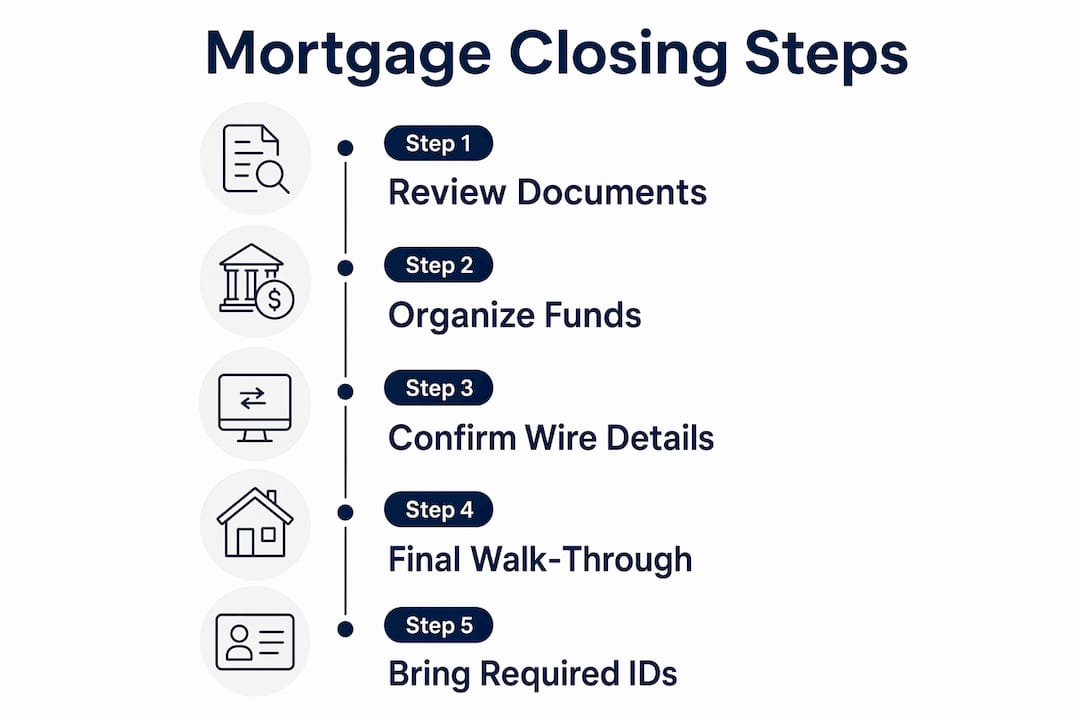

Mortgage closing preparation is the process of completing every required step before you sign your loan documents and take ownership of your home. It covers document review, securing certified funds, confirming homeowner’s insurance, and completing a final property inspection. The CFPB’s TRID rule mandates that your Closing Disclosure arrives at least 3 business days before closing. Skipping any step in this process risks delays, unexpected costs, and even wire fraud. Knowing how to prepare for mortgage closing puts you in control of one of the largest financial transactions of your life.

What are the essential documents to review before mortgage closing?

The Closing Disclosure is the most critical document in your mortgage closing checklist. Under the CFPB’s TRID rule (12 CFR 1026.19(f)), your lender must deliver this 5-page mandatory document at least 3 business days before your closing date. If you do not receive it on time, your closing will be delayed. That 3-day window exists so you can read it carefully, not just sign it.

Closing Disclosure vs. Loan Estimate

Your Loan Estimate arrived early in the loan process and showed projected costs. The Closing Disclosure shows the final, binding numbers. Turn directly to page 3, the “Calculating Cash to Close” section, and compare it line by line against your Loan Estimate. Some fees carry zero tolerance for increases between the two documents. Any unexplained increase is a red flag you must address before signing.

Other documents to review in advance

Beyond the Closing Disclosure, your closing package includes several other documents that deserve careful attention:

- Promissory note: Your legal promise to repay the loan, including the exact interest rate and repayment schedule.

- Deed of trust or mortgage: The document that secures the lender's interest in your property.

- Initial escrow statement: Shows projected monthly escrow payments for taxes and insurance.

- Right of rescission notice: Applies to refinances only, giving you 3 business days to cancel.

- Title documents: Confirm the property transfers to you free of liens or ownership disputes.

Closing meetings move fast, so reviewing these documents days before your appointment reduces errors and increases your confidence at the table. Ask your lender or closing agent to send the full package as early as possible.

Pro Tip: Request your complete closing package at least 48 hours before your appointment. If anything looks unfamiliar or incorrect, call your loan officer immediately. Do not wait until you are sitting at the closing table.

How to organize your funds and payment methods for closing

Confirming your exact cash-to-close amount is a non-negotiable step in preparing for home closing. Pull the final number from your Closing Disclosure and verify it with your lender or escrow agent at least 48 hours before your appointment. That number can shift slightly due to prorated taxes, insurance adjustments, or last-minute lender credits.

Accepted payment methods

Not all payment forms are welcome at the closing table. The rules are clear:

- Wire transfer: The most common method for large amounts. Funds must arrive before or on closing day.

- Cashier's check: Accepted at most title companies. Make it payable to the title company or escrow agent as instructed.

- Personal checks: Not accepted. Do not bring one expecting it to work.

Arrange your funds at least 2 business days before closing to give your bank time to process the transaction. Notify your escrow agent once the wire is sent so they can confirm receipt.

Wire fraud: the threat you cannot ignore

Wire fraud is a major and growing risk in real estate closings. Hackers spoof emails from title companies and redirect your funds to fraudulent accounts. Once the money leaves your bank, recovery is nearly impossible. Always call the title company directly at a phone number you found independently, not one listed in an email, to verify wiring instructions before sending a single dollar.

Independently verify wiring instructions by calling the title company at a trusted number you located yourself. Never rely solely on emailed instructions, even if the email looks legitimate.

Pro Tip: Set up a dedicated call with your title company to confirm wire details verbally. Write down the confirmed account number and routing number, then cross-check them against the written instructions before initiating the transfer.

What to expect at the final property walk-through

The final walk-through is your last chance to inspect the property before it becomes yours. Schedule it 24–48 hours before closing to give yourself time to address any issues that come up. This step is separate from your home inspection, which happened weeks earlier. The walk-through confirms the property’s current condition, not its general structural soundness.

Here is what to check during your final walk-through:

- Confirm agreed repairs are complete. Bring your repair addendum and verify each item was addressed. Ask for receipts or warranties if major work was done.

- Test all appliances and utilities. Run the dishwasher, check the HVAC, turn on every faucet, and flip every light switch. A non-working appliance that was included in the sale is a legitimate issue.

- Check for new damage. Look for holes in walls, stains on carpets, or broken fixtures that were not there during your inspection.

- Confirm the property is empty. The seller should have removed all personal belongings unless specific items were included in the contract.

- Document everything with photos. If you find a problem, photograph it immediately and send the images to your real estate agent.

- Notify your agent right away. Your agent can contact the seller's agent to negotiate a credit, repair, or delayed closing before you sign.

Skipping the walk-through is a mistake that costs buyers money after closing. Post-closing disputes over property condition are difficult and expensive to resolve.

Which documents and items must you bring to closing day?

Arriving at your closing appointment with the wrong documents or missing items can halt the entire process. Every borrower on the loan must bring the following:

- Government-issued photo ID: A driver's license or passport that matches your name exactly as it appears on the loan documents. Expired IDs are not accepted.

- Signed Closing Disclosure copy: Even if you acknowledged it electronically, bring a signed copy as confirmation.

- Proof of homeowner's insurance: A binder or declarations page showing coverage effective on or before the closing date.

- Certified funds: A cashier's check or confirmation of your wire transfer for the exact cash-to-close amount.

- Any additional lender-requested documents: Gift letters, updated bank statements, or verification letters your lender requested in the days before closing.

The table below summarizes what to bring and why each item matters:

Clear-to-close status, typically achieved 1–3 days before closing, signals that your lender has approved all documentation and is ready to fund. Confirm you have reached this milestone before your appointment.

Key Takeaways

Preparing for mortgage closing requires reviewing your Closing Disclosure carefully, securing certified funds in advance, and completing the final walk-through to protect your investment.

What I have learned after watching buyers close on Florida homes

The single biggest mistake I see buyers make is treating the Closing Disclosure like a receipt instead of a contract. By the time you sit down at the closing table, you have already agreed to those numbers. Reviewing it carefully before closing day is your real opportunity to catch errors. I have seen buyers discover incorrect loan terms, wrong interest rates, and fees that were never disclosed. Every one of those issues is fixable before you sign. None of them are easy to fix after.

The wire fraud risk is the part that keeps me up at night. Florida real estate transactions attract sophisticated fraud attempts. I tell every buyer the same thing: call the title company from a number you found on their official website, not from an email. That one habit has protected buyers from losing their entire down payment.

The final walk-through also gets underestimated. Buyers are excited and tired by that point, and they rush through it. I recommend treating it like a second inspection. Take your time, test everything, and photograph anything that looks different from when you made your offer. A 45-minute walk-through has saved buyers thousands of dollars in post-closing repair disputes.

The buyers who close without stress are the ones who start preparing a week out, not the night before. Get your documents early, confirm your funds, verify your instructions, and walk through that property with fresh eyes.

— Chuck Barnes

Platinumcapitalfinancial is here to guide you through closing

Closing on a home in Florida involves more moving parts than most buyers expect. Platinumcapitalfinancial works with homebuyers and real estate investors across Florida to make the process clear and manageable from application through closing day.

Our team reviews your Closing Disclosure with you, explains every fee, and flags anything that does not match your original loan terms. We help you understand your Florida home loan options and confirm your closing costs before your appointment. Whether you are a first-time buyer or an experienced investor, Platinumcapitalfinancial gives you the guidance you need to close with confidence. Reach out to our team today and let us walk you through every step.

FAQ

What is the TRID rule and how does it affect closing?

The TRID rule, issued by the CFPB under 12 CFR 1026.19(f), requires lenders to deliver the Closing Disclosure at least 3 business days before closing. Missing this deadline legally delays your closing date.

How much cash do I need to bring to closing?

Your exact cash-to-close amount appears on page 3 of your Closing Disclosure. Confirm the final number with your lender or escrow agent at least 48 hours before your appointment.

Can I use a personal check at closing?

Personal checks are not accepted at mortgage closings. You must bring a cashier’s check or arrange a wire transfer for the certified amount listed on your Closing Disclosure.

What does clear-to-close mean?

Clear-to-close means your lender has approved all documentation and is ready to fund the loan. This status typically arrives 1–3 days before your closing appointment.

How do I protect myself from wire fraud at closing?

Call the title company directly at a phone number from their official website to verify wiring instructions. Never send funds based solely on instructions received by email.

Recommended

- What Is the Home Loan Process: A 2026 Guide

- Step-by-Step Home Loan Florida: 2026 Guide

- The Role of Mortgage Documents in Home Loans

- How to Negotiate Mortgage Rates and Save Thousands

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)