Business

Why Commercial Loan Rates Feel So Different From Residential Mortgages in Florida

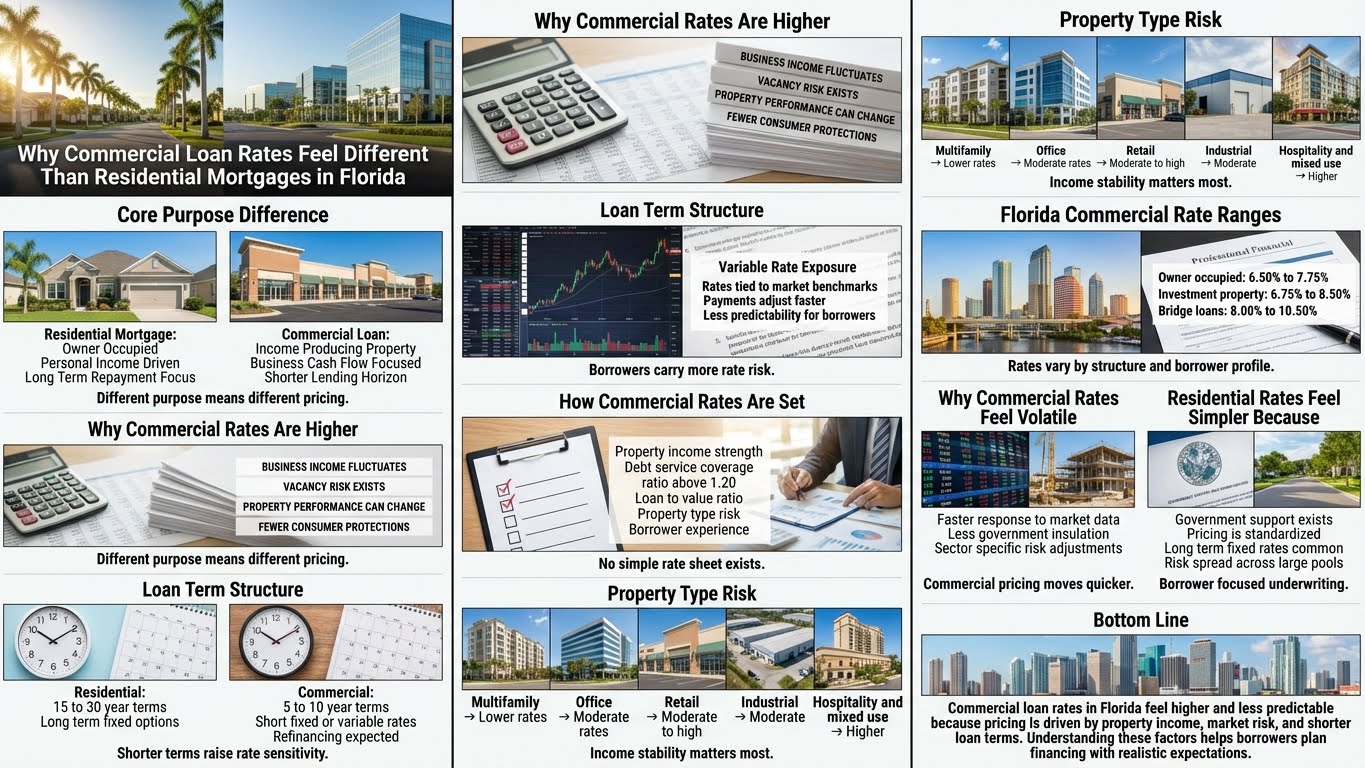

Buyers and investors in Florida are often surprised when they compare residential mortgage rates with commercial loan rates. Even when market conditions seem similar, commercial loans interest rates often feel higher, more variable, and harder to predict. This difference is not accidental. Commercial and residential loans are built on very different risk models, underwriting rules, and pricing structures.

Understanding why mortgage commercial loans are priced differently helps property owners, investors, and business operators make better borrowing decisions. This explanation breaks down how commercial loans real estate pricing works, why rates fluctuate more than home loans, and what Florida borrowers should realistically expect in 2026.

The basic difference between residential and commercial loans

Residential mortgages are designed for owner occupied homes. Commercial loans are designed for income producing property or business related real estate.

Residential mortgage purpose

Residential loans focus on:

- Borrower income stability

- Personal credit history

- Owner occupancy

- Long term repayment

Commercial loan purpose

Commercial loans focus on:

- Property income potential

- Business cash flow

- Market risk

- Shorter lending horizons

Because the goals differ, the pricing models also differ.

Why commercial loan rates are higher

Many Florida borrowers notice that commercial loans rates are often higher than residential mortgage rates. Several reasons explain this.

Higher lender risk

Commercial loans carry more risk for lenders.

Reasons include:

- Business income can fluctuate

- Vacancy risk exists

- Property performance can change

- Fewer consumer protections apply

Residential loans benefit from government support programs and standardized guidelines. Commercial loans do not.

Shorter loan terms

Most residential mortgages are structured over 30 years. Commercial loans typically use shorter terms such as 5 years, 7 years, or 10 years.

Even when amortization extends longer, the rate is usually fixed only for a short period.

Shorter terms increase rate sensitivity and refinancing risk, which raises pricing.

Variable rate structures

Many commercial loans real estate products use variable rates tied to market benchmarks.

These benchmarks move more frequently than residential mortgage pricing models.

As a result:

- Payments can change faster

- Rates feel less predictable

- Borrowers bear more interest rate risk

Less standardized underwriting

Residential mortgages follow standardized rules.

Commercial underwriting is more flexible but also more complex. Each loan is priced based on:

- Property type

- Location

- Tenant strength

- Lease terms

- Borrower experience

- Market conditions

This customization leads to wider rate ranges.

How commercial loan rates are calculated

Commercial rates are not pulled from a simple rate sheet.

Instead, lenders evaluate multiple factors.

Debt service coverage ratio

One of the most important metrics is the debt service coverage ratio.

This measures whether property income can support loan payments.

Typical expectations include:

- A ratio above 1.20

- Stronger ratios for higher risk property types

Lower coverage often means higher rates.

Loan to value ratio

Commercial loans typically require more equity.

Higher loan to value means:

- Higher lender risk

- Higher interest rates

- More conservative terms

Lower loan to value often improves pricing.

Property type risk

Not all properties are priced equally.

Property stability matters more than property value alone.

Borrower experience

Experienced investors often receive better pricing.

Lenders prefer borrowers with:

- Proven management history

- Strong financial statements

- Prior successful projects

First time investors often pay higher rates.

Why residential mortgage rates feel simpler

Residential mortgages feel simpler because:

- Government backing exists

- Long term fixed options are common

- Pricing is standardized

- Risk is spread across large pools

Borrowers qualify primarily based on personal income and credit rather than property performance.

Commercial loan rate ranges in Florida

Commercial pricing varies widely depending on loan type and structure.

Typical commercial loan rate ranges

Rates shift based on market conditions and borrower profile.

Why commercial loan rates feel more volatile

Commercial rates move faster than residential rates.

Reasons include:

- Tighter link to market benchmarks

- Less government insulation

- Faster lender response to economic data

- Sector specific risk adjustments

This volatility can feel uncomfortable for borrowers used to residential mortgages.

Commercial loans rates calculator limitations

Many borrowers search for a commercial loans rates calculator hoping for clarity.

While calculators can provide estimates, they cannot account for:

- Property income quality

- Lease strength

- Market vacancy trends

- Borrower experience

- Negotiated lender terms

Commercial pricing requires lender review.

Florida market factors affecting commercial rates

Local conditions influence current interest rate on commercial loans in Florida.

Key factors include:

- Office vacancy levels

- Retail performance by submarket

- Industrial demand

- Multifamily rent stability

- Local economic growth

Urban and suburban markets may price risk differently.

Why amortization matters

Many commercial loans use long amortization schedules with short rate terms.

For example:

- 25 year amortization

- 5 year fixed rate term

This creates:

- Lower initial payments

- Refinancing exposure later

Borrowers must plan for refinancing well before maturity.

Commercial loans versus residential loans comparison

This explains why pricing feels different.

Business commercial loans and real estate overlap

Some business commercial loans combine operating businesses and property financing.

These loans assess:

- Business financials

- Real estate value

- Cash flow stability

Rates are often higher because both business and property risks are involved.

When commercial loans make sense despite higher rates

Commercial loans still make sense when:

- Property income exceeds costs

- Appreciation potential exists

- Business growth supports debt

- Tax strategies favor ownership

Higher rates do not always mean poor returns.

Common borrower mistakes

Mistakes that increase cost include:

- Underestimating vacancy risk

- Ignoring refinancing timelines

- Overleveraging properties

- Assuming residential pricing logic applies

- Failing to stress test cash flow

Education reduces these risks.

How borrowers can improve commercial loan pricing

Borrowers may improve terms by:

- Increasing down payment

- Strengthening property income

- Improving tenant quality

- Building reserves

- Demonstrating experience

Preparation improves lender confidence.

Frequently asked questions

Why are commercial loan rates higher

They reflect higher risk and less standardization.

Are commercial loan rates fixed

Often only for short periods.

Can commercial rates go down

Yes, but they change faster than residential rates.

Do all properties qualify for the same rates

No. Property type and income matter.

Is refinancing common

Yes. Many commercial loans expect refinancing.

Final perspective for Florida borrowers

Commercial loan rates feel different from residential mortgages because they are designed for different purposes and risks. In Florida, where market conditions vary by property type and location, commercial pricing reflects income performance, market volatility, and lender exposure.

Borrowers who understand how commercial loans for property are priced, why rates fluctuate, and how lenders evaluate risk are better prepared to choose financing that supports long term success. Commercial loans may feel more complex, but with planning and realistic expectations, they remain powerful tools for property ownership and business growth.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)