Business

How a mortgage broker benefits Florida homebuyers

Most Florida homebuyers assume walking into their local bank is the fastest, simplest way to get a mortgage. That assumption can cost you thousands of dollars and months of frustration. A mortgage broker acts as your personal advocate in a complex lending market, with a fiduciary duty to borrowers that banks simply do not share. In Collier County especially, where home prices remain competitive and inventory moves fast, having someone in your corner who understands local lending inside and out can make the difference between getting your dream home and watching it go to another buyer.

Table of Contents

- What exactly does a mortgage broker do?

- Benefits of using a mortgage broker in Florida

- How mortgage brokers simplify the home loan process

- Choosing the right mortgage broker in Collier County

- Why most Florida homebuyers underestimate the power of mortgage brokers

- Get expert help for your Florida mortgage journey

- Frequently asked questions

Key Takeaways

What exactly does a mortgage broker do?

A mortgage broker is not just a go-between who hands your paperwork from one desk to another. That “middleman” myth is one of the most damaging misconceptions in the Florida housing market. Brokers are licensed professionals who work for you, not for a bank or a lender.

Here is what a broker actually handles on your behalf:

- Evaluates your financial profile and matches it to the most suitable loan products

- Submits your application to multiple lenders simultaneously, saving you weeks of legwork

- Negotiates interest rates and loan terms on your behalf

- Translates confusing loan documents into plain language you can actually act on

- Coordinates with title companies, appraisers, and underwriters throughout the process

- Keeps your closing on track so deadlines do not slip

Understanding the buyer’s broker role helps illustrate how fiduciary duty separates brokers from bank loan officers. A bank loan officer is employed by the bank. Their job is to sell you that bank’s products. A broker, on the other hand, has a legal obligation to act in your best financial interest, which means recommending a loan that fits your situation, not one that earns the lender the highest margin.

“Mortgage brokers have a fiduciary duty to borrowers, which means they are legally required to prioritize your interests above their own commission or a lender’s preferences.” This is a protection you simply do not get when you walk directly into a bank branch.

First-time buyers in Collier County often feel overwhelmed by the sheer volume of mortgage terminology. Terms like “points,” “loan-to-value ratio,” “debt-to-income ratio,” and “escrow impounds” can feel like a foreign language. A broker’s job is to cut through that noise and explain exactly what you are agreeing to before you sign anything. If you want mortgage help in Collier County from someone who actually knows the local market, a broker is your clearest path forward.

Benefits of using a mortgage broker in Florida

Once you understand the mortgage broker’s responsibilities, the major benefits they can provide become clear, especially for buyers in Collier County.

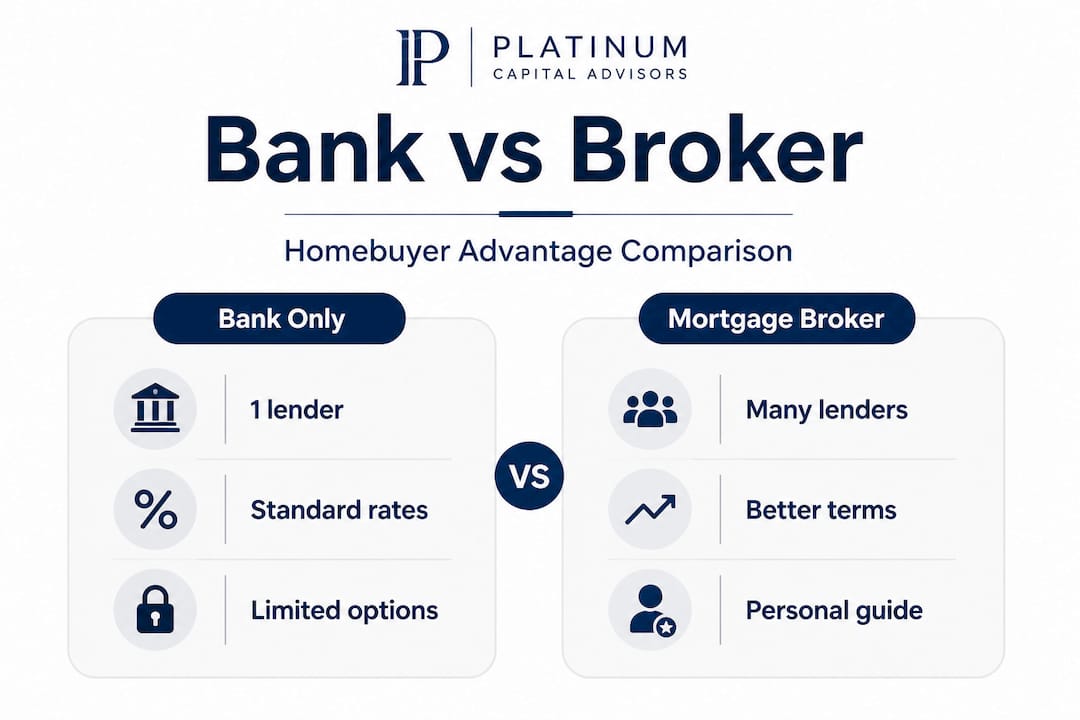

Brokers can access exclusive mortgage access through wholesale lenders that are not available to the general public, apply to multiple lenders, negotiate terms, and streamline paperwork for buyers at every stage of the process. This single advantage changes everything about your shopping experience.

Here is a direct comparison so you can see how the two routes stack up:

For buyers new to Collier County or purchasing their first home anywhere in Florida, the broker route removes several painful guessing games. Local rules around flood zones, homestead exemptions, and property insurance requirements in Southwest Florida are not things most buyers know off the top of their heads. An experienced broker who focuses on mortgage lending in Naples will already have those answers ready before you even ask.

Here are the most concrete benefits, numbered so you can use them as a checklist:

- More loan options. A broker can shop dozens of wholesale lenders in one pass, something no bank branch can match.

- Better rate potential. Because brokers bring lenders volume business, they often unlock pricing that retail customers never see.

- Faster pre-approval. Submitting one package to multiple lenders speeds up the comparison process dramatically.

- Expert navigation of Florida-specific programs. State assistance programs and county-level grants require specific knowledge to access correctly.

- Less paperwork stress. Your broker handles document requests, follow-ups, and condition clearances so you can focus on finding your home.

- Lower risk of costly errors. Missed documents or miscalculated income can sink an approval. Brokers catch those issues before they become problems.

Pro Tip: Before your first broker meeting, gather your last two years of tax returns, two months of bank statements, your most recent pay stubs, and a list of your monthly debts. Showing up prepared cuts your pre-approval timeline significantly and shows lenders you are a serious buyer.

The pitfall of skipping a broker is not just inconvenience. It is real money left on the table. A quarter-point difference in your interest rate on a $450,000 home loan adds up to tens of thousands of dollars over a 30-year term. That is a gap a broker can often close with a single negotiation call.

How mortgage brokers simplify the home loan process

Having seen how brokers open access and negotiate for you, it is equally important to understand how they simplify each step of getting a loan.

The mortgage process has a reputation for being exhausting, and not without reason. Most first-time buyers are blindsided by the sheer volume of documents required. Pay stubs, W-2s, tax returns, bank statements, employment verification letters, asset documentation, explanation letters for any unusual deposits. The list is long. Miss one item and your closing can be delayed by weeks.

Brokers who provide help with mortgage paperwork handle all of that correspondence and follow-up on your behalf. They know exactly what each lender requires before the application goes in, which prevents the back-and-forth that eats up so much time when buyers go it alone. According to the guide on Florida mortgage brokering, brokers handle applications to multiple lenders and streamline paperwork specifically to serve first-time buyers more effectively.

Here is how the timeline typically compares:

Pro Tip: Before signing any loan document, confirm three things: the interest rate matches what was quoted, the loan term is what you agreed to, and there are no prepayment penalty clauses hidden in the fine print. Your broker should walk you through each of these before you ever pick up a pen.

Common mistakes first-time buyers avoid with a broker’s support include:

- Applying to lenders that do not match their credit profile, which wastes time and generates unnecessary credit inquiries

- Underestimating closing costs, which in Florida typically run between 2% and 5% of the loan amount

- Choosing the lowest advertised rate without reading the full terms, which can include expensive origination fees that offset any savings

- Missing rate lock deadlines while waiting for a better offer that never materializes

- Forgetting to account for Florida-specific costs like title insurance, documentary stamp taxes, and mandatory flood insurance in many Collier County zip codes

Every one of these mistakes has a dollar amount attached to it. A broker who knows the local market catches them before they land in your lap.

Choosing the right mortgage broker in Collier County

After learning how brokers support your loan process, the next essential step is choosing a broker you can truly trust in Collier County.

Not all brokers are equal. Some are highly specialized and deeply connected in the Florida market. Others are generalists who dabble in every state and do not know the difference between a Naples flood zone map and a standard property disclosure. Here is how to tell the difference.

Questions to ask before you commit to a broker:

- How long have you been working with buyers specifically in Collier County?

- Which lenders do you work with most often, and why?

- How are you compensated, and will you show me that in writing?

- What loan programs are you currently seeing the best results with for buyers in my situation?

- Can you provide references from recent Florida closings?

Signs of a trustworthy, experienced broker in Florida:

- They explain their compensation structure clearly, without prompting

- They ask detailed questions about your finances before recommending anything

- They can name specific Collier County lenders and programs from memory

- They are licensed in Florida (you can verify this through the Nationwide Multistate Licensing System, or NMLS)

- They set realistic expectations about timelines and rates instead of making promises that sound too good

Red flags to walk away from:

- A broker who cannot explain how they are paid

- Pressure to decide quickly without time to review documents

- Quotes that seem unrealistically low compared to current market rates

- No verifiable Florida license or NMLS number

- Vague answers about which lenders they work with

The fiduciary duty that brokers owe to borrowers is only meaningful when you choose a broker who actually upholds it. Local knowledge matters enormously in Collier County. A broker familiar with the Naples market understands which lenders move quickly on condos in East Naples, which programs work best for buyers relocating from out of state, and which neighborhoods carry flood zone designations that affect your loan options.

Why most Florida homebuyers underestimate the power of mortgage brokers

Here is a perspective that rarely gets said plainly: the advice “just go to your bank” is not bad advice because banks are incompetent. It is bad advice because it assumes your situation fits neatly into one institution’s criteria. For most Florida buyers in 2026, that assumption is almost never true.

Collier County’s market has changed dramatically since 2020. Population growth, rising insurance costs, shifting flood zone designations, and increased demand from out-of-state buyers have created a lending environment where what worked five years ago does not always work today. Banks tightened their requirements during that period. Wholesale lenders, the ones brokers access, often moved faster and created more flexible programs in response.

We have seen buyers with solid credit, good income, and healthy down payments get turned away from their longtime bank simply because the property type or income structure did not fit that bank’s narrow criteria. A broker with local mortgage expertise would have identified three alternative lenders within 24 hours who were perfectly comfortable with that loan profile.

The uncomfortable truth is that most buyers do not know what they do not know. They assume one rejection means they are not ready. It often means they went to the wrong lender for their situation. A broker fixes that problem before it becomes a story you tell at closing about how close you came to losing the house.

In 2026, with interest rates still volatile and Collier County inventory moving at a pace that rewards prepared buyers, working without a broker is a genuine disadvantage. The buyers who move fastest and close cleanest are almost always the ones who had a broker organize their financial profile before they ever made an offer.

Get expert help for your Florida mortgage journey

Navigating Florida’s mortgage market on your own means leaving money, time, and options behind. If you are serious about buying in Collier County or anywhere in Southwest Florida, working with specialists who know the local lending landscape changes the outcome.

Platinum Capital Financial’s team of Naples mortgage specialists is built for exactly this market. Whether you are a first-time buyer still figuring out how pre-approval works, or a relocating buyer trying to understand Florida’s unique insurance and flood zone requirements, the trusted Collier County brokers at Platinum Capital Financial can match you to the right loan program and walk you through every step. Reach out today to review your options, get pre-approved, or simply ask the questions you have been putting off. The right conversation now can save you thousands at closing.

Frequently asked questions

Do I pay extra fees for using a mortgage broker in Florida?

Mortgage brokers are typically compensated by lenders, not borrowers, so most buyers do not pay out-of-pocket fees, but always ask your broker to show you their compensation structure in writing before you proceed.

Can a mortgage broker really get me a better deal than my bank?

Yes, because brokers can access wholesale lenders not available to the public and negotiate terms directly, they often secure better rates or more favorable conditions than a retail bank branch will offer.

Is a mortgage broker involved throughout the entire home loan process?

Yes, brokers support you from the initial application all the way to closing, managing paperwork and lender communication so you are never left wondering what happens next.

What should I look for when choosing a mortgage broker in Collier County?

Prioritize a broker with direct Collier County experience, transparent fee explanations, and a verifiable fiduciary duty to borrowers backed by a current Florida NMLS license.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)