Business

What Is the Home Loan Process: A 2026 Guide

Understanding what is home loan process really involves can save you weeks of frustration and thousands of dollars in avoidable mistakes. Most first-time buyers assume the worst: a mountain of paperwork, mysterious approvals, and a process that feels completely out of their control. The truth is different. The home loan process follows a predictable sequence of stages, and once you know each one, you stop reacting and start planning. This guide walks you through every major step, from getting your finances ready to sitting at the closing table, with practical tips built for 2026 buyers.

Table of Contents

- Key Takeaways

- What is home loan process: the full picture

- Getting financially ready before you apply

- Submitting your application: what lenders actually check

- Underwriting and property assessment: the two-track review

- From sanction letter to closing day

- My take on what first-time buyers consistently get wrong

- Ready to start your home loan process in Florida?

- FAQ

Key Takeaways

What is home loan process: the full picture

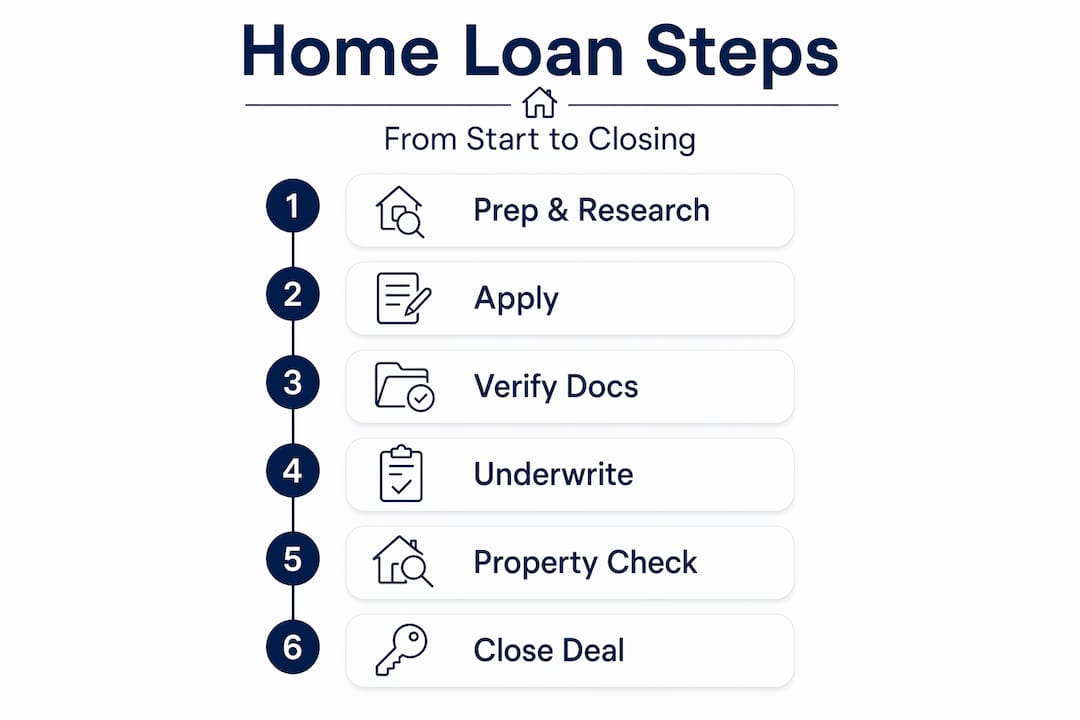

The home loan process is a structured sequence of financial, legal, and administrative steps that a lender uses to verify your eligibility, evaluate the property, and release funds. Think of it less like a bureaucratic obstacle course and more like a two-part story: one part is about you and your finances, the other is about the home you want to buy. Both sides have to check out before the money moves.

For most buyers in Florida, the process runs through six core stages: preparation and research, formal application, document verification, underwriting and property assessment, loan sanction, and finally closing. Each stage builds on the one before it. If you skip steps or cut corners early, you will feel it later in the form of delays, extra paperwork, or even a rejected application.

Understanding home financing at this level gives you real power. You know what to prepare, what to expect, and where the bottlenecks typically happen. That changes your entire experience as a buyer.

Getting financially ready before you apply

Most people jump straight to house hunting, then scramble to figure out their finances. Flip that sequence, and you will be ahead of 80% of buyers from day one.

Start with your credit score. A score of 750 or above is generally the threshold for securing the most favorable loan terms as of 2026. Scores below that do not disqualify you, but they will affect your interest rate and how much you can borrow. Pull your credit report early, dispute any errors, and avoid opening new credit accounts for at least six months before applying.

Next, get honest about your budget. Your monthly mortgage payment should include principal, interest, property taxes, insurance, and any homeowners association fees. A useful rule of thumb is to keep your total housing costs under 28% of your gross monthly income. Calculate this before you fall in love with a specific price point.

Here is a basic document checklist to have ready before you start the home loan application steps:

- Government-issued photo ID and Social Security number

- Two years of federal tax returns

- Recent pay stubs covering the last 30 days

- Two to three months of bank and investment statements

- Proof of any additional income sources (rental income, freelance work)

- Employment verification letter from your current employer

Pro Tip: Get pre-approved, not just pre-qualified. Pre-qualification is a quick estimate based on self-reported numbers. Pre-approval involves actual document review and carries real weight with sellers in competitive Florida markets.

Submitting your application: what lenders actually check

Once you are financially prepared, you submit your formal loan application. This is where the home loan application steps shift from personal preparation to lender verification.

Your lender will review three main areas. First, your identity: every document must match exactly. Document mismatches across personal details are the primary cause of processing delays, so double-check that your name, address, and identification numbers are consistent across every form you submit. One typo can send your file back to square one.

Second, your income and employment. Lenders want to see stability. They will review your pay stubs, W-2 forms, and federal tax returns. Self-employed borrowers face extra scrutiny and typically need two full years of business tax returns plus a profit and loss statement.

Third, your assets and liabilities. Bank statements show lenders that you have the funds for a down payment and closing costs, and that those funds were not borrowed last week. Large unexplained deposits raise flags and trigger additional documentation requests.

AI-driven verification tools are now accelerating document review and credit assessment at many lenders. But do not let that make you sloppy with your paperwork. AI finds inconsistencies faster than humans did, it does not overlook them.

Pro Tip: Organize all your documents into clearly labeled digital folders before you apply. When a lender requests a specific item, you want to respond within 24 hours. Slow responses are one of the most controllable causes of closing delays.

Underwriting and property assessment: the two-track review

This is the stage where many first-time buyers feel the most anxiety, and it is also the most misunderstood part of the home loan approval process. Underwriting is not a single check. It is two distinct evaluations running in parallel.

Your financial profile under the microscope

The underwriter reviews your full financial picture: your debt-to-income ratio, credit history, employment stability, and overall capacity to repay. Underwriting evaluates both your capacity to repay and the collateral security provided by the property, independently. Even if your finances are spotless, a problem with the property can still block your loan.

The debt-to-income ratio is one of the most critical numbers here. Most conventional loans require your total monthly debt payments, including the new mortgage, to stay below 43% of your gross income. Some loan programs allow higher ratios with compensating factors like a larger down payment or significant cash reserves.

The property gets its own evaluation

The property you want to buy goes through two separate checks: legal due diligence and technical valuation. Legal clearances involve a title search to confirm the seller has clear ownership, checking for any existing liens or encumbrances, and verifying that no legal disputes are attached to the property.

The technical valuation confirms market value, construction quality, and compliance with local building codes. In Florida, this matters especially for flood zone designations and hurricane-resistant construction standards, both of which affect insurability and therefore lender approval.

Pro Tip: Order your own title search early and ask your real estate agent if the property has been involved in any recent legal proceedings. Discovering a title issue after the lender’s review is ordered costs you both time and money.

From sanction letter to closing day

Once underwriting clears both tracks, your lender issues a sanction letter. This document defines your approved loan amount, interest rate, repayment tenure, and any conditions you must meet before disbursement. The sanction letter is typically valid for six months, so read it carefully and act within that window.

Here is what happens between sanction and closing:

- Review the sanction letter in detail. Confirm the interest rate type (fixed or adjustable), the loan amount, and any conditions attached. If something does not match your expectations, address it with your lender before signing anything.

- Sign the loan agreement. This is the legally binding contract. Set up your automatic payment instructions at this stage to avoid missed payments.

- Secure homeowners insurance. Homeowners insurance is mandatory and is typically paid through an escrow account as part of your monthly mortgage payment. Shop for coverage before closing so you can show proof at the table.

- Avoid major financial changes. Final underwriting reviews your credit and finances again right before closing. Taking on new debt, quitting your job, or making large purchases during this window can delay or derail your closing.

- Review the closing disclosure. You must receive this document at least three business days before closing. Compare it line by line against your loan estimate.

- Close and receive your keys. On closing day, you sign the final documents, pay closing costs, and the property transfers to your name.

Pro Tip: Lock your interest rate as soon as you get a number you are comfortable with. Rates can shift between application and closing, and a rate lock protects you from market movements during that window.

My take on what first-time buyers consistently get wrong

I have worked with a lot of buyers over the years, and I keep seeing the same blind spots. The biggest one is underestimating how much the property’s legal history matters. Everyone obsesses over their credit score, and yes, it matters. But I have watched perfectly creditworthy borrowers get derailed because the property had an unresolved lien from a previous owner’s contractor dispute. That is not a credit problem. That is a due diligence problem, and no one warned them to check for it.

The second thing I see is people treating document submission as a one-time event. In my experience, lenders will come back with follow-up requests, sometimes several rounds of them. The buyers who close on time are the ones who stay organized, respond fast, and never lose track of what they submitted and when.

I will also say this about the AI tools that lenders are increasingly using: they are genuinely useful for speed, but they surface inconsistencies that used to slip through. That means a small name discrepancy that might have been overlooked five years ago now triggers an automatic flag. Prepare your documents like they will be scrutinized by a very detail-oriented algorithm. Because they will be.

Staying financially quiet between approval and closing is harder than it sounds. I have seen buyers celebrate by financing new furniture for the home they have not technically closed on yet. That purchase shows up in the final credit pull, raises the debt-to-income ratio, and suddenly the file needs re-underwriting. Do not do this. Wait until after you have the keys.

- Chuck Barnes

Ready to start your home loan process in Florida?

If you are buying in Collier County or anywhere in the Naples area, Platinumcapitalfinancial works with first-time buyers every day to make the steps in mortgage processing clear and manageable from day one.

At Platinumcapitalfinancial, you get local expertise in Florida’s market conditions combined with access to multiple lender programs, so you are not stuck with a one-size-fits-all option. Whether you are still in the preparation stage or ready to apply, the team can walk you through your eligibility and match you to the right loan for your situation. Check out the mortgage loan options available for Naples and Collier County homebuyers, and get started with a simple online inquiry today. The right guidance early in the process is the single biggest factor in a smooth closing.

FAQ

What is the home loan process, step by step?

The home loan process runs through six key stages: financial preparation, formal application, document verification, underwriting and property assessment, loan sanction, and closing. Each stage requires specific documentation and decisions from both the borrower and the lender.

How long does mortgage approval take?

Most mortgage approvals take between 30 and 60 days from application to closing, depending on the lender, loan type, and how quickly borrowers respond to document requests. Complex cases or title issues can extend this timeline.

What credit score do I need for a home loan?

A credit score of 750 or above is generally the benchmark for the best loan terms in 2026. Lower scores may still qualify for certain loan programs but typically result in higher interest rates.

What happens after mortgage approval?

After approval, you receive a sanction letter, sign your loan agreement, purchase homeowners insurance, and prepare for closing. Avoid major financial changes during this period, as final underwriting reviews your credit before closing day.

Why do home loans get delayed?

The most common cause is document mismatches in personal information across submitted files. Other frequent causes include title issues found during legal due diligence and slow borrower responses to lender follow-up requests.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)