Mortgage News

What Is Lender Credit? A Clear Guide for Homebuyers

A lender credit is money your mortgage lender gives you to help cover closing costs in exchange for a higher interest rate on your loan. This trade-off is one of the most misunderstood features in home financing. Buyers who understand lender credits can make sharper decisions about upfront cash versus long-term cost. This guide covers how lender credits work, who qualifies, and when they actually make financial sense for Florida homebuyers in 2026.

What is lender credit and how does it work?

A lender credit is a direct offset against your closing costs, paid by the lender in exchange for a higher interest rate on your mortgage. The more credit you accept, the higher your rate goes. That rate increase is permanent unless you refinance later.

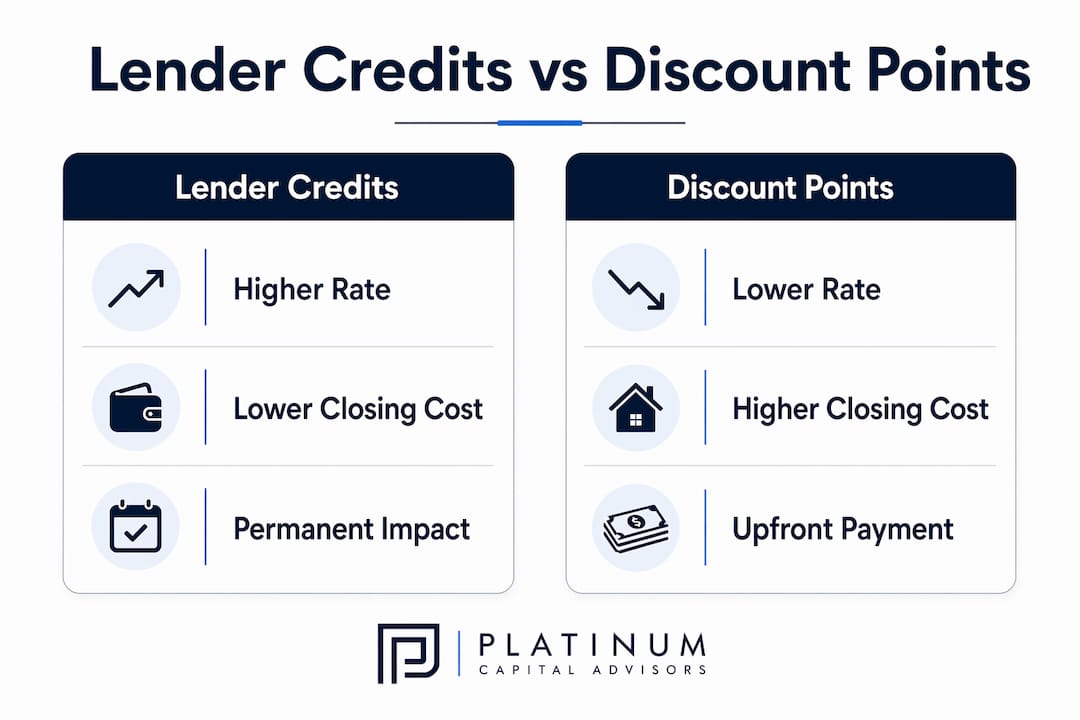

Think of it as the mirror image of discount points. With discount points, you pay money upfront to buy a lower rate. With a lender credit, the lender pays your closing costs and you repay that favor through a higher rate over time. Lender credits and discount points are inverse concepts by design.

One critical boundary: lender credits only apply to bona fide closing costs. They cannot reduce your down payment or pay off debts that affect your debt-to-income ratio. If the credit exceeds your actual closing costs, the lender reduces the credit to match. You do not receive the difference as cash.

How lenders calculate the credit amount

Lenders set a base interest rate using factors like your credit score, debt-to-income ratio, property type, and loan size. They then add a rate increase on top of that base to generate the credit amount. A larger credit requires a larger rate bump.

To qualify for competitive lender credits, most lenders require a 20% down payment and a debt-to-income ratio at or below 45%. These benchmarks reflect standard pricing criteria as of early 2026. Borrowers who fall short of these thresholds may still qualify for credits, but the rate increase will likely be steeper.

Pro Tip: Ask your loan officer to show you the exact rate increase tied to each credit amount. Lenders are required to disclose this on the Loan Estimate form, so you can compare offers side by side.

What are the financial benefits and drawbacks of lender credits?

Lender credits solve a real problem: many buyers have enough income to afford a monthly mortgage payment but not enough cash saved to cover closing costs on top of a down payment. A credit can make homeownership possible without draining your savings account.

The benefits are straightforward:

- Lower cash at closing. You need less money out of pocket on closing day.

- Preserved liquidity. You keep cash available for moving costs, repairs, or an emergency fund.

- Faster access to homeownership. Buyers who are cash-limited can close sooner rather than saving for years.

- Useful for short-term ownership. If you plan to sell or refinance within a few years, you may never pay back the full cost of the higher rate.

The drawbacks are just as real:

Lender credits are not free money. The lender is compensated through a higher interest rate, which increases your total interest paid over the life of the loan.

The rate increase from a lender credit is permanent until you refinance. Every month you hold that loan, you pay a slightly higher payment than you would have without the credit. Over a 30-year mortgage, that difference adds up to thousands of dollars.

A second risk is less obvious. A credit score drop before closing can raise your base rate, which makes the lender credit less effective or even unaffordable. Avoid opening new credit accounts, missing payments, or making large purchases between your application and closing day.

Pro Tip: Run a break-even calculation before accepting any lender credit. Divide the total credit amount by the monthly payment increase. That number tells you how many months it takes before the higher rate costs more than the credit saved.

Lender credits vs closing costs and discount points

Understanding lender credits requires understanding what they sit alongside. Closing costs are the fees you pay to finalize a mortgage. They typically include lender fees, title insurance, appraisal costs, and prepaid items like homeowners insurance. These costs are real and due at closing regardless of whether you use a credit.

Discount points and lender credits occupy opposite ends of the same spectrum:

Discount points make sense when you plan to stay in the home long enough to recoup the upfront cost through lower monthly payments. Lender credits make sense when you need to preserve cash now and expect to sell or refinance before the higher rate costs more than the credit saved.

What lender credits can cover:

- Lender origination fees

- Title and settlement fees

- Appraisal fees

- Prepaid interest and escrow deposits

What they cannot cover:

- Your down payment

- Debt payoff to lower your DTI ratio

- Any cost not classified as a bona fide closing cost

Pro Tip: When comparing loan offers from different lenders, always look at the combination of rate and credits together. A lower rate with no credit may cost less at closing than a higher rate with a large credit, depending on your timeline.

When should you consider using lender credits?

Lender credits are best suited to buyers with limited cash for closing or those who plan to refinance or move within a few years. The math shifts against you the longer you hold the loan at the higher rate.

The borrower profiles that benefit most from lender credits include:

- First-time buyers who have saved for a down payment but have little left for closing costs

- Buyers in high-cost markets like South Florida where closing costs can run several thousand dollars

- Homeowners refinancing who want to reduce out-of-pocket costs and plan to refinance again if rates drop

- Buyers with a near-term move planned who know they will sell within three to five years

The profiles that should think twice include buyers who plan to stay in the home for 10 or more years. For long-term owners, lender credits may not be cost-effective compared to paying closing costs outright or buying points to lower the rate.

When comparing lender offers, request a Loan Estimate from each lender. The Loan Estimate shows the interest rate, monthly payment, and total closing costs in a standardized format. You can see exactly how much credit each lender offers and what rate you are accepting in return.

One common misconception is that a larger credit is always better. A credit that saves you $4,000 at closing but costs you $80 more per month takes over four years to break even. If you sell in year three, you came out ahead. If you stay for 15 years, you paid far more than you saved.

Pro Tip: Coordinate lender credits with seller concessions when possible. In a buyer-friendly market, sellers may also contribute to closing costs. Combining both can significantly reduce your cash needed at closing without stacking rate increases.

Key Takeaways

Lender credits reduce your upfront closing costs but permanently raise your mortgage rate, making them a smart short-term tool and a costly long-term commitment if you stay in the home for many years.

My honest take on lender credits after years in mortgage lending

Lender credits are one of the most frequently misread tools in a mortgage. Clients come in focused on the number at the bottom of the closing disclosure, and a large credit looks like a win. What they miss is the rate column right next to it.

I have seen buyers accept a lender credit that saved them $5,000 at closing, then hold that loan for 12 years and pay back triple that amount through higher monthly payments. The credit was not wrong for them. The timeline was wrong for them. The decision looked good on closing day and looked very different a decade later.

The clients who use lender credits well are the ones who treat them as a tool with a specific job. They know they are moving in four years. They know they plan to refinance when rates drop. They are not guessing. They have a plan, and the credit fits that plan.

My advice: never accept a lender credit without running the break-even math first. If your break-even point is beyond your expected ownership timeline, the credit costs you money. If it falls well inside that timeline, the credit makes sense. The calculation takes five minutes and can save you thousands.

— Chuck Barnes

How Platinumcapitalfinancial can help you structure your home loan

Platinumcapitalfinancial works with homebuyers and families across Florida to find mortgage structures that fit their actual financial situation, not just their closing day budget.

Whether you are weighing lender credits against discount points, comparing loan types, or trying to figure out how much home you can afford in Collier County, Platinumcapitalfinancial has the experience to walk you through the numbers. The team specializes in home loans and refinancing in Florida, with a focus on giving buyers a clear picture of long-term costs before they sign. Check current mortgage rates in Naples to see how today’s rate environment affects your credit trade-off calculation.

FAQ

What is lender credit on a mortgage?

A lender credit is money the lender contributes toward your closing costs in exchange for a higher interest rate on your mortgage loan. It reduces your upfront cash requirement but increases your monthly payment for the life of the loan.

Can lender credits lower my monthly payment?

No. Lender credits increase your interest rate, which raises your monthly payment. They reduce what you pay at closing, not what you pay each month.

Do lender credits affect my interest rate permanently?

Yes. The rate increase from a lender credit is permanent unless you refinance your mortgage. Refinancing resets your rate but also resets your closing costs.

Can I use a lender credit for my down payment?

No. Lender credits apply only to bona fide closing costs. They cannot be used to reduce your down payment or pay off debts that affect your debt-to-income ratio.

Who benefits most from lender credits?

Buyers with limited cash at closing and those who plan to sell or refinance within a few years benefit most. Long-term homeowners typically pay more in total interest than they saved at closing.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)