Business

What Is an Adjustable Rate Mortgage? Your 2026 Guide

An adjustable rate mortgage, commonly called an ARM, is a home loan where the interest rate stays fixed for an initial period and then adjusts periodically based on market conditions. That initial fixed period typically runs 3, 5, 7, or 10 years, after which your monthly payment can rise or fall depending on where benchmark rates move. ARMs differ fundamentally from fixed-rate mortgages, which lock your rate for the entire loan term. About 90% of homebuyers prefer fixed-rate mortgages over ARMs. That statistic tells you ARMs are not for everyone, but they can be the right tool for the right borrower.

What is an adjustable rate mortgage and how does it work?

An ARM has two distinct phases. The first is the initial fixed period, where your interest rate does not change. The second is the adjustment period, where the rate resets at regular intervals based on a market index plus a lender margin.

The initial fixed period is the most predictable part of the loan. Common initial fixed periods run 3 to 10 years, after which the rate can adjust every 6 or 12 months. A 5/1 ARM, for example, holds a fixed rate for five years and then adjusts once per year. A 7/6 ARM fixes the rate for seven years and adjusts every six months after that.

After the fixed period ends, the lender recalculates your rate using a benchmark index plus a set margin. The most widely used benchmark today is the Secured Overnight Financing Rate (SOFR), which replaced LIBOR as the standard index for most ARM products. If SOFR rises, your rate rises. If it falls, your rate falls.

Here is what drives your adjusted rate each period:

- Benchmark index: A market rate like SOFR that reflects current lending conditions

- Lender margin: A fixed percentage added on top of the index, set at loan origination

- Adjustment frequency: How often the rate resets, typically every 6 or 12 months

- Rate caps: Limits on how much the rate can move at each adjustment and over the life of the loan

Rate caps are the built-in protection every ARM carries. Caps limit how much the rate can increase or decrease at the initial adjustment, at each subsequent adjustment, and over the entire loan term. Understanding those caps is the single most important step before signing any ARM agreement.

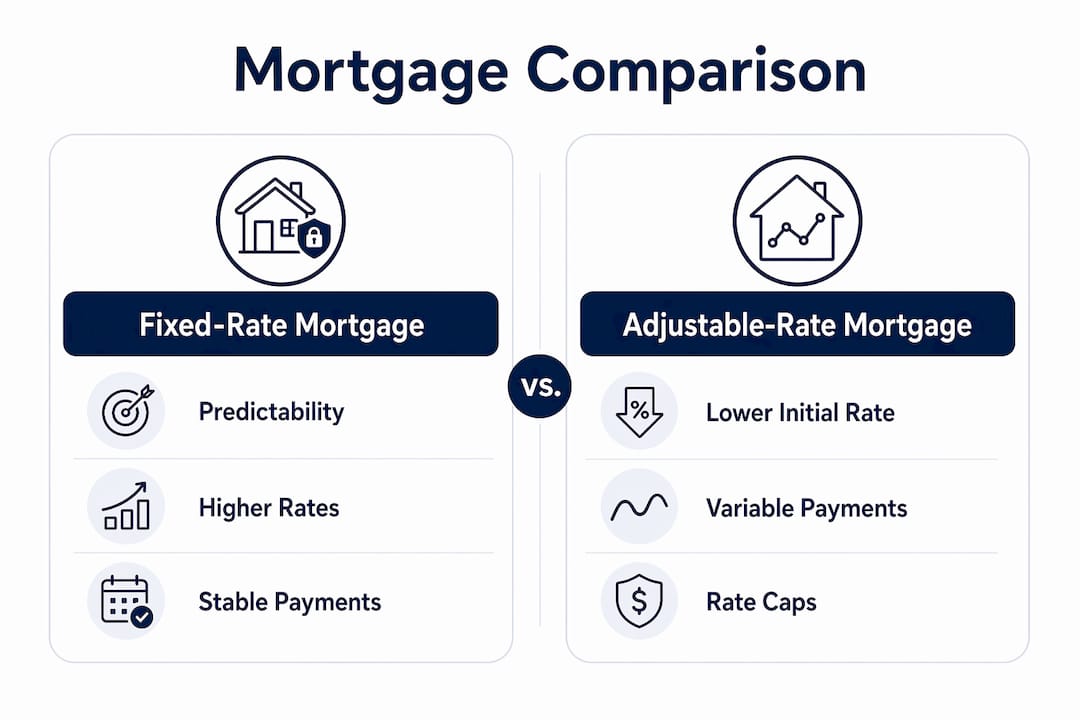

Fixed vs adjustable mortgage: which one fits your situation?

The core difference between a fixed-rate and an adjustable-rate mortgage comes down to predictability versus potential savings. A fixed-rate loan locks your payment for 15 or 30 years. An ARM gives you a lower starting rate in exchange for future uncertainty.

ARMs almost always carry lower initial interest rates than comparable fixed-rate loans. Lower early-term payments make ARMs practical for borrowers who plan to move, sell, or refinance within five years. If you buy a home in Florida knowing you will relocate in four years, paying a higher fixed rate for 30 years makes little financial sense.

The table below compares the two loan types across the features that matter most to most borrowers.

The advantages of fixed rate loans are real. You know your payment on day one and on year 29. That certainty has genuine value, especially for borrowers on tight budgets or fixed incomes. The tradeoff is that you pay for that certainty with a higher rate from the start.

Advantages and risks of adjustable rate mortgages

ARMs carry real financial benefits, but they also carry risks that catch unprepared borrowers off guard. Knowing both sides clearly is the only way to make a sound decision.

The main advantages

Lower initial interest rates and payments on ARMs create meaningful savings, especially when fixed rates are elevated at the time of purchase. If you take out a 5/1 ARM and sell the home in year four, you never experience a single rate adjustment. You captured the lower rate and exited before the risk materialized.

The advantages of adjustable rate mortgages include:

- Lower starting payments: You pay less per month during the fixed period compared to a fixed-rate loan at the same loan amount

- Potential savings in high-rate environments: When fixed rates are high, the ARM discount can be significant over a five-year horizon

- Flexibility for short-term owners: Borrowers who plan to move or refinance within the fixed period avoid adjustment risk entirely

- Qualification advantage: A lower initial rate can help some borrowers qualify for a larger loan amount

The real risks

Payment shock is the most serious risk. If rates rise sharply after your fixed period ends, your monthly payment can jump by hundreds of dollars. Caps on ARMs typically include an initial adjustment cap of 2%–5%, a periodic cap of 1%–2%, and a lifetime cap of commonly 5%. On a $400,000 loan, a 5% lifetime rate increase adds a substantial amount to your monthly payment.

Refinancing is not a guaranteed escape route. Refinancing depends on qualifying factors like credit, income, and home equity. If your home value drops or your income changes, you may not qualify to refinance when you need to most.

Pro Tip: Before you commit to an ARM, calculate your maximum possible payment using the lifetime cap. If that payment would strain your budget, the loan is not the right fit regardless of how attractive the initial rate looks.

Who should consider an adjustable rate mortgage?

An ARM is not a product for every borrower. It fits a specific set of financial situations well and fits others poorly.

The borrowers who benefit most from ARMs share a few common traits:

- Short planned ownership: You expect to sell or move within 5 years, before the adjustment period begins

- Anticipated income growth: You are early in your career and expect your income to rise enough to absorb higher payments later

- Refinancing plan with realistic backing: You have strong equity, stable employment, and good credit, making future refinancing genuinely viable

- High-rate purchase environment: You are buying when fixed rates are elevated and want to reduce your initial cost burden

The borrowers who should be cautious include anyone on a fixed income, anyone with limited savings to absorb payment increases, and anyone whose plan to sell or refinance depends on circumstances outside their control.

Many homebuyers overestimate their ability to predict financial stability over the ARM fixed period. Life changes, job losses, and market downturns disrupt even well-laid plans. Affordability planning for ARMs must incorporate worst-case rate increases rather than focus only on the initial low payment. If the worst-case payment is unmanageable, the ARM is the wrong choice.

The Consumer Financial Protection Bureau (CFPB) recommends that borrowers ask lenders to show them the maximum possible payment before signing. That single number tells you more about your actual risk than any initial rate quote.

Key Takeaways

An ARM delivers real savings during the fixed period, but the risk of payment shock after adjustment makes it unsuitable for borrowers without a clear exit plan or the financial cushion to absorb rate increases.

Why I tell every ARM borrower to run the worst-case numbers first

After working with home loan borrowers across Florida for years, the pattern I see most often is this: a borrower focuses entirely on the initial monthly payment and treats the adjustment period as a distant, abstract problem. It is not abstract. It is a contractual certainty.

The borrowers who use ARMs well are the ones who have already done the math on the maximum payment before they close. They know exactly what their payment looks like if rates hit the lifetime cap. They have confirmed that payment is manageable. Then they proceed with confidence.

The borrowers who struggle are the ones who assumed they would refinance before the adjustment hit. Refinancing sounds simple until your home value drops 10% or your employer downsizes. Refinancing an ARM to avoid payment shock depends on having sufficient home equity, good credit, and stable income at the time. None of those factors are guaranteed.

My honest advice: if you cannot afford the worst-case payment, choose a fixed-rate loan. The lower initial rate on an ARM is only a good deal if you have a real plan, not a hopeful one.

— Chuck Barnes

ARM home loans in Florida with Platinumcapitalfinancial

Platinumcapitalfinancial works with Florida home buyers who want to understand their loan options before committing to one. Whether an ARM fits your situation or a fixed-rate loan makes more sense, the right answer depends on your timeline, income, and risk tolerance.

Platinumcapitalfinancial specializes in ARM loans in Florida and can walk you through the numbers that matter most, including your maximum possible payment after adjustment. If you are also weighing a fixed-rate option, the team can compare both side by side so you make a fully informed choice. Reach out to Platinumcapitalfinancial through the Florida home loan page to start a conversation about which loan structure fits your goals.

FAQ

What is an adjustable rate mortgage in simple terms?

An adjustable rate mortgage is a home loan with an interest rate that stays fixed for an initial period, then changes periodically based on a market benchmark. The rate can go up or down depending on market conditions after the fixed period ends.

How does an ARM work after the fixed period?

After the fixed period, the lender recalculates your rate using a benchmark index like SOFR plus a set margin. The rate then adjusts every 6 or 12 months within the limits set by your rate caps.

What are the main types of adjustable rate mortgages?

The most common ARM types are named by their fixed and adjustment periods: a 5/1 ARM fixes the rate for five years and adjusts annually, while a 7/6 ARM fixes for seven years and adjusts every six months.

Are rate caps on ARMs required?

Rate caps are standard on most ARM products and limit how much your interest rate can increase at the first adjustment, at each subsequent adjustment, and over the life of the loan. The CFPB recommends reviewing all three cap levels before signing.

When does an ARM make more financial sense than a fixed-rate loan?

An ARM makes the most sense when you plan to sell or refinance within the fixed period, when fixed rates are high at the time of purchase, or when a lower initial payment is needed to qualify for the loan amount you require.

Recommended

- What Is a Hybrid Mortgage? Your 2026 Guide

- Adjustable Rate Mortgage (ARM) Loans in Florida

- Should I Get an Adjustable Rate Mortgage in Naples Florida?

- What Happens When an Adjustable Rate Mortgage Adjusts in Naples Florida?

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)