Business

What Is a Mortgage Servicer? Your 2026 Guide

A mortgage servicer is the company responsible for managing your home loan after closing, collecting your monthly payments, maintaining your escrow account, and handling customer support. Understanding what is mortgage servicer means in practice is one of the most overlooked parts of homeownership. Many buyers focus entirely on getting approved and signing papers, then feel blindsided when a company they have never heard of starts sending their mortgage statements. The servicer is your primary point of contact for everything related to your loan account, and knowing how it works protects you from costly mistakes.

What does a mortgage servicer do day to day?

A mortgage servicer manages the daily administration of your home loan, from the moment your first payment is due until the loan is paid off. The lender hands off these responsibilities after closing so it can focus on originating new loans. Your servicer becomes the company you call, write to, and pay every month.

Payment collection and crediting

The servicer receives your monthly payment and applies it to principal, interest, and escrow. One detail most homeowners miss: if you send a partial payment, the servicer does not apply it immediately. Partial payments sit in a suspense account until the full amount accumulates. Your loan can appear delinquent even if you sent money. Reading your monthly statement carefully is the only way to catch this before it becomes a problem.

Escrow account management

Your servicer collects a portion of your property taxes and homeowner’s insurance with each payment and holds those funds in escrow. The servicer then pays those bills on your behalf when they come due. Federal rules require servicers to provide escrow estimates within 45 days of establishing the account and to send you an annual escrow statement. That statement shows every deposit, every disbursement, and any shortage or surplus.

Monthly statements and payoff information

Every billing cycle, your servicer must send a detailed written statement. That statement must show your outstanding balance, the breakdown of your payment, any fees charged, and the status of your suspense account. When you are ready to pay off the loan, the servicer provides a payoff statement with the exact amount needed. After payoff, the servicer must refund your escrow balance within 20 days.

Pro Tip: Set a calendar reminder to review your annual escrow statement the week it arrives. Shortages increase your monthly payment, and catching them early gives you time to plan.

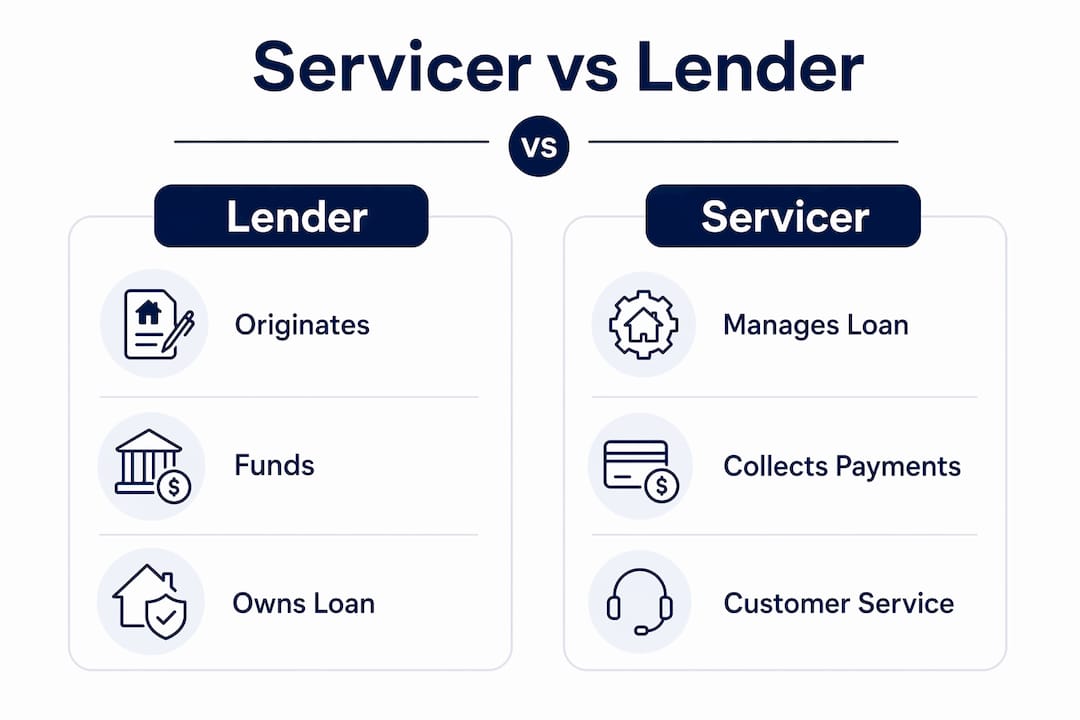

How is a mortgage servicer different from a lender?

The lender originates and funds your loan. The servicer manages it afterward. These two roles are often held by different companies, which confuses many homeowners. Outsourcing servicing lets lenders free up capital and focus on writing new loans, while servicers specialize in account management and earn a fee based on the outstanding loan balance.

There is also a third party in this picture: the investor. The investor owns the loan’s cash flows and bears the credit risk. The servicer acts as the intermediary between you and that investor, collecting your payments and passing them through.

Servicing rights can be sold or transferred at any time without changing your loan terms. Your interest rate, balance, and repayment schedule stay exactly the same. Only the company you send payments to changes.

Pro Tip: When your servicer changes, update your autopay immediately. Sending a payment to the old servicer after the transfer date can trigger a late fee even if the funds eventually reach the right place.

What federal rules protect you in 2026?

Federal regulations set clear standards for how servicers must treat you. The Consumer Financial Protection Bureau enforces most of these rules, and servicers who violate them face formal complaints and penalties.

- Written statements every billing cycle. Your servicer must send a detailed statement for each billing period. That statement must include your payment breakdown, outstanding balance, and any suspense account funds. Federal rules require timely communication about payment status.

- Hardship evaluation before foreclosure. If you fall behind, your servicer must evaluate your hardship application and offer available relief options before starting foreclosure proceedings. Servicers follow mandated protocols for this process. Skipping straight to foreclosure without this step violates federal law.

- Escrow account disclosures. Servicers must provide an initial escrow estimate within 45 days and an annual statement every year. If your escrow account runs short, the servicer must notify you and give you time to make up the difference.

- Servicing transfer notices. When your loan transfers to a new servicer, you must receive formal written notice at least 15 days before the change takes effect. That notice must include the new servicer's contact information and payment instructions.

- Recordkeeping obligations. Servicers must maintain records for at least one year after payoff or after a servicing transfer. That requirement protects you if a dispute arises about payment history or escrow balances.

These protections exist because the relationship between a borrower and a servicer is not equal. You have limited choices about who services your loan. Federal rules compensate for that imbalance by holding servicers to strict standards.

How should you interact with your mortgage servicer?

Proactive communication is the single most effective tool you have when managing your loan. Early borrower communication is the most important factor in securing hardship options and avoiding foreclosure. Waiting until you are three months behind dramatically narrows your options.

Here are the practices that protect you most:

- Contact your servicer before missing a payment. Call as soon as you know a payment will be late. Servicers have hardship programs, forbearance options, and repayment plans that are only available to borrowers who ask early.

- Update your payment method immediately after a transfer. When your loan moves to a new servicer, you have 60 days of protection from late fees. Use that window to update autopay, not as a reason to delay.

- Read every monthly statement. Check the suspense account line. If money is sitting there and not being applied, call your servicer to understand why.

- Request a payoff statement in writing. If you are refinancing or selling, get the payoff amount in writing with a specific good-through date. Verbal quotes are not binding.

- Track your escrow refund after payoff. If you pay off your loan and the escrow refund does not arrive within 20 days, send a written error notice. That triggers a formal investigation.

Pro Tip: Keep a dedicated folder, physical or digital, for every piece of correspondence from your servicer. If a dispute ever arises, your paper trail is your strongest defense.

One thing most homeowners do not realize: you can file a formal complaint with the Consumer Financial Protection Bureau if your servicer violates any of these rules. That complaint goes on record and requires a response. It is a real enforcement tool, not just a suggestion box.

Key Takeaways

A mortgage servicer manages your loan account after closing and is governed by federal rules that protect your rights as a homeowner.

What I have learned after years of watching borrowers navigate this

Most homeowners I work with are surprised when their loan servicer is a different company from the lender who approved them. That surprise is understandable. You spend months building a relationship with a loan officer, and then the first statement arrives from a company you have never heard of. The confusion is real, and it causes real problems.

The biggest mistake I see is borrowers who ignore servicing transfer notices because they look like junk mail. That notice contains your new payment address and account number. Missing it and sending a payment to the old servicer can damage your credit even if you did everything else right.

The second thing most people miss is the suspense account. A borrower sends $900 when the payment is $1,050, thinking they are making progress. The servicer holds that $900 in suspense. The next statement shows a missed payment. The borrower panics. The fix is simple: always pay the full amount, and always read the statement line by line.

Escrow is the third area where I see homeowners lose money. When you refinance or sell, that escrow balance is yours. Servicers are required to return it within 20 days. If you do not track it, it can slip through the cracks. Set a reminder. Send a written notice if the deadline passes.

Treat your servicer as a financial partner, not an adversary. They have programs to help you. They have rules they must follow. Knowing both sides of that relationship puts you in a much stronger position.

— Chuck Barnes

Working with Platinumcapitalfinancial on your Florida home loan

Understanding your mortgage servicer is one piece of the larger picture. Choosing the right loan structure from the start shapes everything that follows, including how your escrow is set up, what your monthly statement looks like, and what options you have if life gets complicated.

Platinumcapitalfinancial works with home buyers and homeowners across Florida to find loan options that fit their actual situation, not just their credit score. Whether you are buying your first home, refinancing an existing loan, or exploring Florida home loan options, the team at Platinumcapitalfinancial can walk you through every step. Getting the loan right at closing means fewer surprises once a servicer takes over. Reach out to Platinumcapitalfinancial to talk through your options with a licensed Florida mortgage broker.

FAQ

What is a mortgage servicer in simple terms?

A mortgage servicer is the company that manages your home loan after closing. It collects your payments, maintains your escrow account, and handles customer service on your loan.

Who is my mortgage servicer and how do I find out?

Your servicer’s name appears on your monthly mortgage statement. You can also check the Consumer Financial Protection Bureau’s mortgage lookup tool or contact your original lender.

Can my mortgage servicer change without my permission?

Yes. Servicing rights transfer without requiring your approval, but the servicer must notify you in writing at least 15 days before the change. Your loan terms do not change.

What happens if my mortgage servicer makes an error?

Send a written error notice to your servicer. Federal rules require the servicer to investigate and respond. You can also file a complaint with the Consumer Financial Protection Bureau if the issue is not resolved.

Does my mortgage servicer own my loan?

No. The servicer administers the loan but does not own it. The investor or lienholder owns the loan’s cash flows. The servicer acts as the intermediary between you and that investor.

Recommended

- What Is a Mortgagee? a Guide for Homebuyers

- What Is a Mortgage Lien? Your 2026 Homeowner Guide

- What is mortgage origination? Florida homebuyer's guide

- What Is Mortgage Insurance? A Homebuyer's Guide

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)