Business

Mortgage Pre Approval for Florida Homebuyers Explained

Most Florida homebuyers use the terms “prequalification” and “pre-approval” interchangeably. That’s a costly mistake. Knowing what is mortgage pre approval and how it differs from a simple prequalification estimate can determine whether a seller takes your offer seriously or passes it over entirely. This guide breaks down the mortgage pre approval process from start to finish, explains the real benefits of mortgage pre approval, and gives you a clear roadmap for getting pre approved for a mortgage in Florida, whether you’re buying your first home or refinancing an existing one.

Table of Contents

- Key takeaways

- What mortgage pre approval means and how it works

- Pre-approval vs. prequalification: key differences

- Benefits of mortgage pre approval for Florida buyers

- What mortgage pre approval does not guarantee

- How to prepare and apply for mortgage pre approval in Florida

- Why pre-approval can make or break your Florida homebuying experience

- Ready to get pre-approved with Platinumcapitalfinancial?

- FAQ

Key takeaways

What mortgage pre approval means and how it works

Mortgage pre approval is a formal evaluation by a lender that tells you how much you can borrow and on what terms, before you make an offer on a home. It is not a guarantee of a loan. It is a conditional commitment based on what the lender has verified at a specific point in time.

Here is what the mortgage pre approval process actually looks like, step by step:

- Submit a formal application. You fill out a Uniform Residential Loan Application, also called a Form 1003, and give the lender permission to pull your credit report.

- Provide supporting documents. The lender needs proof of income (pay stubs from the last 30 days, W-2s from the last two years), tax returns, two to three months of bank statements, and a government-issued ID.

- Undergo credit verification. The lender runs a hard credit pull to assess your credit score, debt-to-income ratio, and payment history. Many loan programs accept credit scores around 620 and down payments as low as 3%, so do not assume you are disqualified before you apply.

- Lender reviews your financial profile. The underwriter or loan officer looks at your employment stability, monthly debts, and how much you have in savings relative to the loan amount you are requesting.

- Receive your pre-approval letter. Once approved, the lender issues a letter that includes your name, the approved loan amount, the interest rate, the loan type (FHA, conventional, VA, etc.), and the conditions you must still meet before closing.

According to Zillow, 94% of mortgage buyers get pre-approved before purchasing a home. That figure alone tells you this is not optional in today’s market. It is the baseline.

On timing: lenders typically issue a pre-approval letter within one to two business days after you submit a complete application. The letter itself is generally valid for 60 to 90 days, which gives you a realistic window to search for homes and make offers.

Pro Tip: Apply for pre-approval before you start attending open houses. Walking into a showing without a letter puts you in a weak position if you find a home you want immediately.

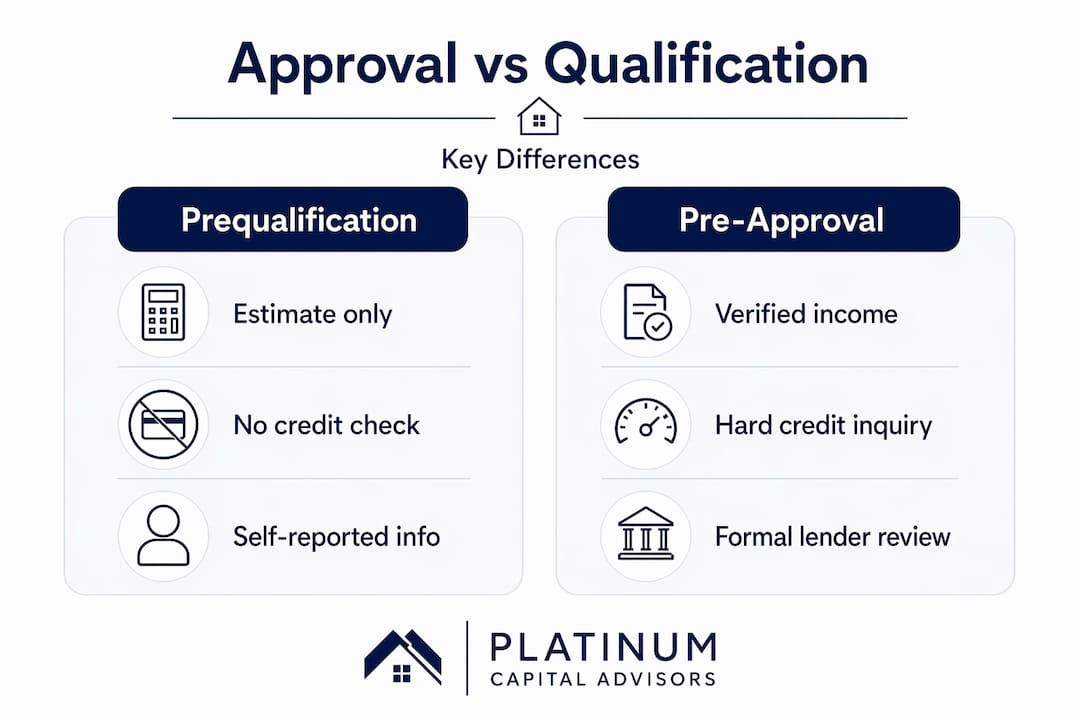

Pre-approval vs. prequalification: key differences

These two terms sound similar but represent very different levels of commitment from a lender. Understanding why mortgage prequalification is not the same as pre-approval protects you from a false sense of readiness.

Prequalification is an informal estimate. You provide basic financial information verbally or through a quick online form, and the lender gives you a ballpark figure of what you might qualify for. No credit check is run. No documents are verified. The estimate is based entirely on what you say about your income, debts, and assets.

Pre-approval, by contrast, involves the lender actually verifying your financials and performing a credit check. That distinction is the difference between a lender saying “you seem like you could afford this” versus “we have checked your records and you qualify up to this amount under these conditions.”

Here is a side-by-side comparison to make that concrete:

Pre-approval is more formal and reliable than prequalification because the lender has actually done the work of confirming what you say is true. When a seller in Naples or Miami receives two competing offers and one buyer has a prequalification while the other has a pre-approval letter, the pre-approved buyer wins almost every time.

The benefits of mortgage prequalification are not zero. It is a useful first step to understand roughly where you stand before committing to the full application. But if you are actively searching for a home in Florida, you need a pre-approval letter, not a prequalification estimate.

Benefits of mortgage pre approval for Florida buyers

Florida’s real estate market moves fast in many counties, especially in Southwest Florida areas like Naples and Collier County. Getting pre-approved before you start seriously searching is one of the most practical decisions you can make.

Here are the real benefits of mortgage pre approval that go beyond the obvious:

- You shop with a real number, not a guess. Getting preapproved early helps you set a clear budget, reduces time wasted on homes you cannot afford, and prevents delays at closing. Knowing your ceiling means you stop touring homes that would stretch your finances past comfort.

- Sellers take you seriously. In a competitive Florida market, a pre-approval letter shows the seller you are not a tire-kicker. Verified financing capability leads sellers to prioritize your offer over unverified buyers.

- You catch problems early. If your credit report has an error, a collections account, or a higher debt-to-income ratio than expected, you find out during pre-approval, not on the day you are supposed to close. That gives you time to fix things before it derails a deal.

- You negotiate from strength. Sellers who receive an offer backed by a pre-approval letter know the deal is far less likely to fall through due to financing issues. That confidence can actually give you more leverage on price or terms.

- Refinancers benefit too. If you are refinancing an existing Florida property, pre-approval confirms your updated financial profile qualifies for the new loan terms you are targeting.

Pro Tip: If you are buying in a high-demand area like Naples or Sarasota, ask your lender whether they offer same-day pre-approval for qualified applicants. Speed matters when multiple buyers are competing for the same listing.

What mortgage pre approval does not guarantee

Understanding what does mortgage pre approval mean also requires knowing what it does not cover. This is where many buyers get tripped up, sometimes expensively.

A pre-approval is not a final loan commitment. Final mortgage approval happens after the pre-approval, once the lender reassesses your financial status closer to closing. Several things can change between receiving your letter and getting to the closing table.

Watch out for these common pitfalls:

- Taking on new debt. Financing a car, opening a new credit card, or making a large purchase on credit between pre-approval and closing can increase your debt-to-income ratio enough to void your pre-approval.

- Changing jobs or losing income. Employment stability is a core part of what lenders evaluate. A job change, even a lateral one, can trigger a full re-verification of your financial profile.

- Large, unexplained deposits. If you suddenly move significant sums of money into your accounts without a paper trail, underwriters may flag it and delay or deny the final loan.

- Letting your letter expire. Pre-approval letters are valid for 60 to 90 days. If your home search extends past that window, you will need to reapply. In some cases, your financial situation or interest rates may have shifted, changing your terms.

- Making inaccurate statements on your application. Your lender will verify everything you submit. Any significant changes in financial situation can nullify the pre-approval when the final review happens near closing.

The safest rule from the moment you receive your letter until closing: do not make any major financial moves without consulting your lender first.

How to prepare and apply for mortgage pre approval in Florida

Preparing well before you submit your application makes the process faster and improves the likelihood of a favorable outcome. Here is how to approach the steps for mortgage pre approval as a Florida buyer or refinancer.

- Check your credit report first. Pull your free annual report from AnnualCreditReport.com and review it for errors. Dispute any inaccurate items before applying. Even a small score improvement can open up better loan programs.

- Gather your financial documents. You will need two years of tax returns, the last two W-2s or 1099s (if self-employed), recent pay stubs, two to three months of bank statements, and documentation of any other assets such as investment accounts.

- Calculate your debt-to-income ratio. Add up all your monthly debt payments and divide by your gross monthly income. Most lenders want this figure below 43%, though some programs allow higher with compensating factors.

- Work with a lender who knows Florida. Local market knowledge matters when structuring a loan for Florida-specific considerations, including flood zone disclosures and homeowners association requirements in certain communities.

- Time your application strategically. Do not apply six months before you plan to buy. Given that pre-approval letters are valid for 60 to 90 days, apply when you are genuinely ready to search and make offers.

Exploring your Florida mortgage loan options with a broker who specializes in the state's specific market can also give you access to loan programs that a national lender may not actively offer to Florida buyers.

Why pre-approval can make or break your Florida homebuying experience

I have worked with a lot of buyers in Florida, and the pattern I see most often is this: the ones who skip pre-approval or rely on a prequalification letter end up losing the homes they wanted. Not because they were not financially qualified. Because they were not ready when it mattered.

I remember a first-time buyer in Collier County who found the perfect property and waited three days to get pre-approved while another buyer with a letter in hand made an offer the same afternoon. The home was gone before the paperwork even came through. That is not a rare story. It is a Tuesday in Florida real estate.

What I have also seen is buyers who discover during pre-approval that a common myth about credit score requirements was holding them back. They assumed they needed a 740 credit score and 20% down. They had neither, so they never applied. When they finally did, they qualified under an FHA program with significantly lower requirements.

My take: get pre-approved before you think you are ready. The worst outcome is learning what you need to fix. The best outcome is that you are already holding the letter when the right home comes up. That gap between “I think I can afford this” and “I have a letter that proves it” is exactly where deals are won or lost in Florida.

Ready to get pre-approved with Platinumcapitalfinancial?

Understanding the mortgage pre approval process is the foundation. But having the right lending partner to guide you through it in Florida makes everything smoother.

Platinumcapitalfinancial is a mortgage broker serving buyers and refinancers across Florida, with a focus on Naples and Collier County. Whether you are a first-time buyer trying to understand your budget or a homeowner exploring refinancing options, the team at Platinumcapitalfinancial walks you through every step, from document collection to your final pre-approval letter. Working with a local specialist means faster responses, familiarity with Florida’s market conditions, and loan programs suited to your actual situation. Start your pre-approval process today by visiting Platinumcapitalfinancial’s mortgage loan page.

FAQ

What does mortgage pre approval mean?

Mortgage pre approval means a lender has reviewed your income, credit, assets, and debts and has conditionally agreed to lend you a specific amount. It is not a final loan guarantee but a verified indication of your borrowing capacity.

How long does mortgage pre approval take in Florida?

Lenders typically issue pre-approval letters within one to two business days after receiving a complete application, though having all documents ready upfront speeds up the process.

How is pre-approval different from prequalification?

Prequalification is an informal estimate based on self-reported information with no credit check, while pre-approval involves verified financials and a formal credit inquiry, making it far more credible to sellers.

Can a pre-approval be revoked before closing?

Yes. Significant financial changes such as taking on new debt, changing jobs, or making large unexplained deposits between pre-approval and closing can lead to the lender withdrawing their conditional commitment.

What credit score do I need to get pre-approved in Florida?

Many loan programs accept credit scores around 620, and some government-backed programs go lower. You do not need perfect credit to qualify, which is a common misconception that delays many Florida buyers from even starting the process.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)