Mortgage News

How to Submit Mortgage Paperwork: 2026 Guide

Submitting mortgage paperwork means delivering accurate financial, personal, and property documents to your lender so they can evaluate your loan application. The mortgage application process is more structured than most homebuyers expect. Lenders follow federal disclosure timelines, which means approval typically takes 30–60 days from the date you apply. Knowing how to submit mortgage paperwork correctly, and in the right order, is the single biggest factor in whether your closing stays on schedule.

What documents do you need for mortgage approval?

The mortgage documentation checklist falls into three categories: financial records, personal identification, and property documents. Missing even one item triggers a re-request from your lender, which adds days or weeks to your timeline.

Financial documents

Standard financial documents include the following:

- Pay stubs from the last 30 days

- W-2 forms for the past two years

- Federal tax returns for the past two years

- Bank statements covering the last 60 days, including all pages

- Investment and retirement account statements if you are using those funds for a down payment

Self-employed homebuyers face a longer list. Lenders require year-to-date profit and loss statements, 1099 forms, and sometimes two years of business tax returns. This is because lenders need to verify income stability, not just a single paycheck.

Property documents

Lenders require property-related documents such as the signed purchase agreement, the appraisal report, and proof of title. These confirm the home’s value and that ownership can legally transfer to you. Without them, underwriting cannot proceed.

Organization tips

Label every file clearly before you upload it. Use a naming format like “LastName_W2_2024” so your loan officer can find documents instantly. Group related files into folders by category: income, assets, and property.

Pro Tip: Scan documents at 300 DPI or higher. Blurry or low-resolution files are one of the most common reasons lenders send re-requests.

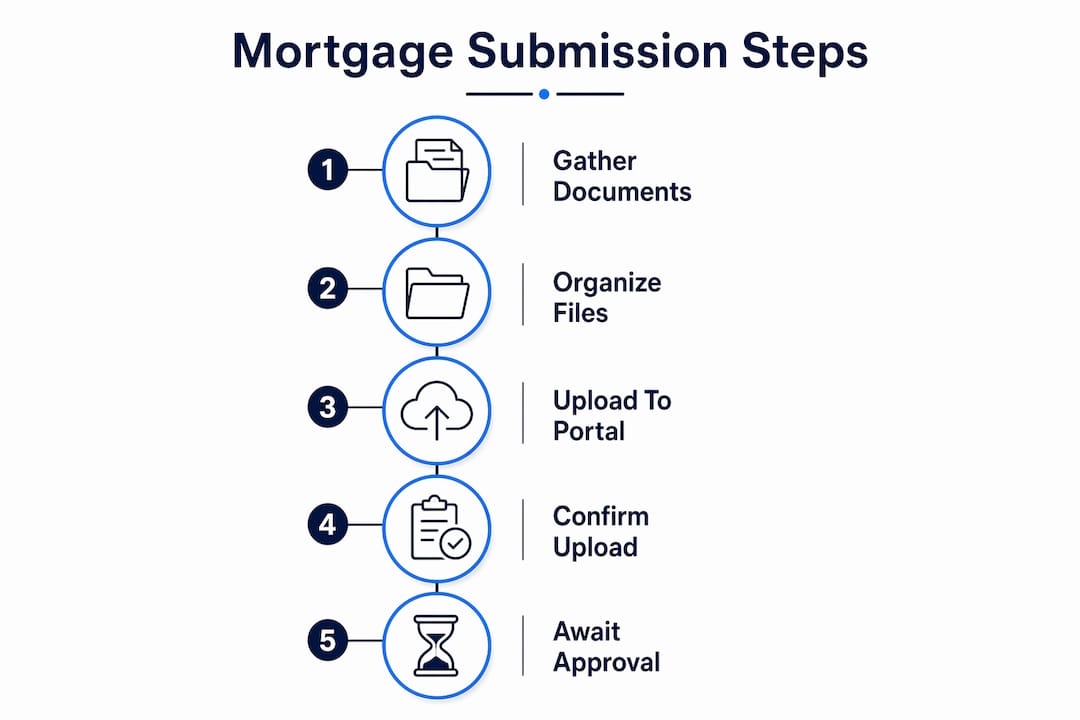

How and where to submit your mortgage paperwork

The method you use to send documents matters as much as the documents themselves. Secure lender portals are the fastest and most reliable option. Submitting through a secure portal reduces errors and accelerates processing compared to email or physical mail.

Here is what to do when submitting documents:

- Use the lender's secure portal whenever one is available. It creates a time-stamped record of every upload.

- Avoid email for sensitive documents unless your lender specifically requests it and uses encrypted email.

- Submit PDFs, not screenshots. Screenshots cut off edges and omit metadata that underwriters need.

- Include every page of multi-page documents. All pages of bank statements, even blank ones, must be included.

- Confirm receipt after every upload. Send a quick message to your loan officer asking them to verify the files came through.

Physical mail is the slowest option and creates no digital audit trail. Reserve it only if your lender has no portal and does not accept email.

Pro Tip: After uploading, download your own copies from the portal to confirm the files are not corrupted. A file that uploads successfully can still open as blank if it was damaged during transfer.

What is the step-by-step mortgage submission process?

The mortgage application process follows a predictable sequence. Knowing each step helps you respond quickly and avoid surprises.

- Complete the Uniform Residential Loan Application. This is Fannie Mae Form 1003, the standardized form used by lenders across the country. It covers your income, assets, debts, and the property you want to buy.

- Sign the required disclosures. Signatures confirm accuracy and give the lender legal consent to pull your credit report. Depending on your lender, you sign electronically or in person.

- Receive your Loan Estimate. Federal law requires lenders to send this within three business days of your application. It outlines your estimated interest rate, monthly payment, and closing costs.

- Respond to underwriting requests. Underwriters review every document and often ask follow-up questions. Respond within 24–48 hours. Delays here are the most common reason closings get pushed back.

- Receive your Closing Disclosure. Lenders must deliver this at least three days before closing. It shows your final loan terms and closing costs. Review it carefully against your Loan Estimate.

The table below shows the typical timeline from application to closing.

One timing detail most homebuyers overlook: pre-approval letters typically expire within 10 days. If your closing date shifts, check whether your pre-approval is still valid before you submit final documents.

Common mistakes when submitting mortgage paperwork

Incomplete or illegible documents are the leading cause of re-requests during underwriting. Every re-request adds time to your closing. The good news is that most mistakes are completely avoidable.

“Treating documentation as a continuous process, with regular updates and open dialogue, is what separates borrowers who close in 30 days from those who wait 60.” — Mortgage professionals consistently report this as the defining factor in fast closings.

Watch for these specific errors:

- Submitting outdated documents. Bank statements and pay stubs older than 30 days after your pre-approval date are often rejected. Refresh them before final submission.

- Missing pages. A 12-page bank statement submitted as 10 pages raises a red flag. Lenders assume the missing pages contain something problematic.

- Illegible files. Photographed documents taken in poor lighting fail quality checks. Use a flatbed scanner or a dedicated scanning app on your phone.

- Ignoring follow-up requests. A lender's request for additional documents is not optional. Ignoring it stops your file from moving forward entirely.

- Changing your financial situation mid-process. Opening a new credit card, making a large purchase, or changing jobs between application and closing can require a full re-underwrite.

The simplest quality check: open every file yourself before uploading. If you can read it clearly on your screen, your underwriter can read it too.

Key Takeaways

Submitting mortgage paperwork correctly requires organized, complete, and current documents delivered through your lender’s secure portal, with fast responses to every follow-up request.

What I have learned after watching hundreds of mortgage files move through underwriting

Most homebuyers treat the mortgage application as a single event. They gather documents, submit them, and wait. That mindset is what causes delays.

The homebuyers I have seen close fastest treat the process as an ongoing conversation. They check their email daily. They respond to lender requests the same day. They keep a folder of updated financial documents ready to send at a moment’s notice. That level of preparation is not excessive. It is exactly what the process requires.

One thing I tell every homebuyer: your loan officer is your ally, not a gatekeeper. If you do not understand a request, call and ask. A two-minute phone call prevents a three-day delay. Lenders want your file to close. They are not looking for reasons to reject you. They are looking for complete information.

Digital tools have made submission easier, but they have also raised lender expectations. Uploading a blurry photo of a document used to be acceptable. Now, with secure portals and scanning apps widely available, lenders expect clean, complete files on the first submission. Meet that expectation and you will spend far less time in underwriting limbo.

The homebuyers who struggle are almost always the ones who go quiet after the initial submission. Stay visible. Stay responsive. The mortgage application process rewards people who treat it like a job, not a waiting game.

— Chuck Barnes

Working with Platinumcapitalfinancial on your Florida home loan

Platinumcapitalfinancial works with Florida homebuyers every day to get mortgage files organized, submitted, and approved without unnecessary back-and-forth. The team provides personalized document checklists tailored to your loan type, whether you are buying your first home, refinancing, or purchasing an investment property.

When you work with a Florida mortgage broker through Platinumcapitalfinancial, you get direct access to secure submission portals and a loan officer who reviews your documents before they go to the lender. That pre-review catches missing pages, outdated statements, and labeling errors before they cause delays. If you have questions about FHA loan eligibility or any other loan type, the team can walk you through the specifics for your situation.

FAQ

What documents are needed for mortgage approval?

Standard documents include W-2s for two years, federal tax returns, recent pay stubs, 60 days of bank statements, and property documents like the purchase agreement and appraisal report. Self-employed applicants also need profit and loss statements and 1099 forms.

How long does mortgage approval take after submitting paperwork?

Mortgage approval typically takes 30–60 days from the date of application, depending on how quickly you respond to lender requests and how complete your initial submission is.

What is the easiest way to submit mortgage forms?

The easiest and fastest method is uploading documents directly through your lender’s secure online portal. Portals create a time-stamped record and allow your loan officer to access files immediately.

Why do lenders ask for all pages of bank statements?

Including all pages, even blank ones, gives underwriters a complete picture of your account activity. Missing pages trigger re-requests and delay your file.

What happens if I submit outdated mortgage documents?

Documents older than 30 days after pre-approval are often rejected by underwriters. You will need to provide updated versions, which restarts that portion of the review and can push your closing date back.

Recommended

- How to Apply for a Mortgage in Florida: 2026 Guide

- Mortgage Pitfalls to Avoid in Florida: 2026 Guide

- Step-by-Step Home Loan Florida: 2026 Guide

- The Role of Mortgage Documents in Home Loans

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)