Mortgage News

Florida Homestead Exemption: Benefits, Rules, and How to Apply

The Florida homestead exemption is defined as a property tax benefit that reduces assessed value by up to $50,000 on a qualifying primary residence. Florida homeowners who claim it typically save between $600 and $1,500 per year in property taxes, depending on their county’s millage rate. Beyond the tax break, the exemption triggers the Save Our Homes cap and creditor protections that can shield your home’s value for decades. If you are buying or already own a home in Florida, understanding what is Florida homestead exemption means understanding one of the most powerful financial tools available to you.

What is the Florida homestead exemption and who does it apply to?

The Florida homestead exemption is a constitutional benefit that cuts the taxable assessed value of your primary residence. The first $25,000 reduction applies to all property taxes, including school taxes. The second $25,000 applies only to non-school taxes, covering assessed values between $50,000 and $75,000. That distinction matters because school taxes represent a significant portion of your total tax bill.

The exemption applies only to your primary residence in Florida. You cannot claim it on a vacation home, rental property, or second home. Florida law also prohibits claiming a homestead exemption in another state at the same time. This is a firm rule, and counties do cross-check records.

Who qualifies for the Florida homestead exemption?

Qualifying for the Florida homestead exemption requires meeting several clear conditions. You must hold legal or beneficial title to the property and occupy it as your permanent residence as of january 1 of the tax year you are applying for. U.S. citizens and permanent residents with valid immigration status are eligible. Non-permanent residents do not qualify.

The core eligibility requirements are:

- Legal or beneficial title to the property as of january 1

- Permanent Florida residency with the home as your primary address

- Valid U.S. citizenship or permanent resident status

- No active homestead exemption claimed in any other state or county

- Form DR-501 filed with your county property appraiser by march 1

Documentation typically required includes a Florida driver’s license or ID, vehicle registration, voter registration, and proof of Social Security number. Some counties also ask for a utility bill or bank statement showing the property address.

Pro Tip: File as early as possible after moving in. Many Florida counties now accept pre-filing applications before the january 1 residency date, which removes the risk of missing the march 1 deadline.

What benefits beyond tax savings does the homestead exemption provide?

The tax reduction is the most visible benefit, but the Florida homestead exemption delivers three additional protections that compound in value over time.

The Save Our Homes cap

Once your exemption is approved, the Save Our Homes cap limits annual increases in your property’s assessed value to 3% or the Consumer Price Index, whichever is lower. In a hot real estate market like Miami-Dade, Collier County, or Palm Beach, this cap can save homeowners tens of thousands of dollars over a decade. Without it, your assessed value could rise as fast as the market, sending your tax bill sharply higher each year.

Portability makes the Save Our Homes benefit even more powerful. When you sell your Florida homestead and buy another one in Florida, you can transfer up to $500,000 of your accumulated savings to the new property. You have two years from the date you sell to apply for portability. This is a major advantage for homeowners who have built up years of assessment savings and want to move without losing them.

Creditor protection

The Florida homestead exemption provides strong protection against forced sale by most creditors. A civil judgment creditor generally cannot force the sale of your primary residence to collect a debt. This protection is automatic under the Florida Constitution once you establish residency. You do not need to file a separate form to activate it.

“The homestead tax exemption and the constitutional creditor protection operate independently. The exemption requires formal filing while creditor protection applies automatically once residency is established.” — LegalClarity

The protection has real limits. It does not apply to IRS liens or federal tax debts. Mortgages, property tax liens, mechanic’s liens, and money obtained through fraud are also exceptions. Knowing what is and is not covered prevents a false sense of security.

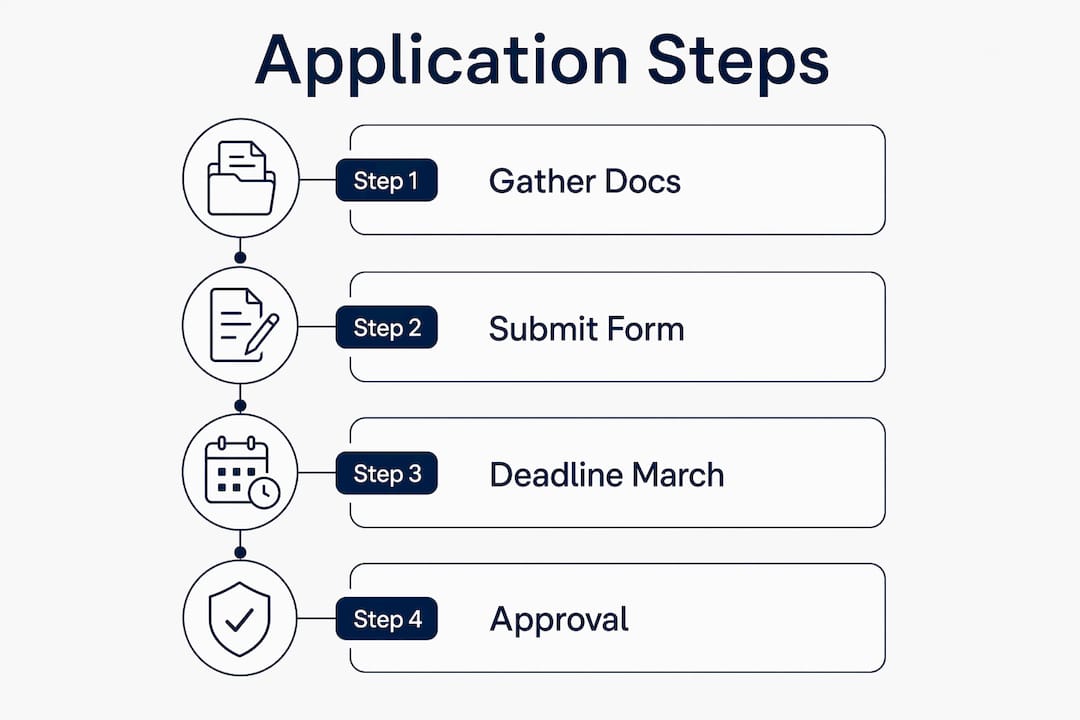

How to apply for Florida homestead exemption

The application process is straightforward when you follow the steps in order.

- Confirm your eligibility. Verify you hold title and occupy the property as your primary residence as of january 1 of the tax year.

- Gather your documents. Collect your Florida driver's license or state ID, Social Security number, Florida vehicle registration, and voter registration card if applicable.

- File Form DR-501. Submit this form to your county property appraiser's office. The filing deadline is march 1. Most counties now accept online applications through their official property appraiser websites.

- Apply for portability if moving. If you are transferring a Save Our Homes benefit from a prior Florida homestead, file Form DR-501T at the same time.

- Confirm your approval. Check your county property appraiser's website or wait for your TRIM (Truth in Millage) notice in august to confirm the exemption appears on your record.

Missing the march 1 deadline is a common and costly mistake. Some counties allow late filing or appeals to the Value Adjustment Board, which charges a $15 filing fee. Approval depends on documented extenuating circumstances and varies by county.

Pro Tip: Set a calendar reminder for january 2 each year. If you moved into a new Florida home in the prior year, that reminder gives you two full months to gather documents and file before the march 1 cutoff.

Once approved, the exemption renews automatically each year. You do not need to refile unless your status changes.

Common limitations: renting, trusts, bankruptcy, and property sales

The exemption is not permanent by default. Several common scenarios can trigger its loss, and the penalties include retroactive tax bills.

Renting is the most common trap. Renting your homestead for more than 30 days in a calendar year can cost you the exemption for that entire tax year under Florida Statute 196.061. Renting for more than one year requires notifying your county property appraiser and may result in permanent loss until you reapply.

Additional limitations to know:

- Trust ownership requires careful review. Revocable living trusts often preserve the exemption, but irrevocable trusts or title transfers to LLCs typically do not.

- Bankruptcy protection has a federal ceiling. The 1,215-day federal rule limits homestead protection for newer Florida residents who have not rolled over equity from a prior Florida homestead.

- Unreported changes carry real financial risk. Incorrect or unreported changes can lead to retroactive tax bills and penalties going back multiple years.

- Property sales reset the assessment cap entirely. The new buyer starts fresh with a market-rate assessed value.

Proactively notifying your county property appraiser about any ownership or residency changes is the single best way to avoid penalties.

Key Takeaways

The Florida homestead exemption reduces your property’s assessed value by up to $50,000, saves most homeowners $600 to $1,500 annually, and provides creditor protection and a long-term assessment cap through Save Our Homes.

What I have learned after years of watching Florida homeowners use this exemption

Most homeowners file once and forget it. That is fine when nothing changes. The problem is that life changes constantly, and the exemption does not forgive inattention.

The Save Our Homes cap is the most undervalued part of this entire benefit. In Collier County and Miami-Dade, where property values have climbed sharply over the past decade, homeowners who filed early and held their homes have seen their assessed values frozen far below market. A neighbor who bought the same model home two years later pays dramatically more in taxes. That gap grows every year you stay. The long-term advantage of the Save Our Homes provision is not theoretical. It is real money, compounding quietly in the background.

The creditor protection piece is where I see the most dangerous misconceptions. Homeowners assume the exemption creates a complete legal shield around their property. It does not. Federal tax liens cut right through it. If you owe the IRS, your Florida homestead is not safe. That is a hard truth worth knowing before you rely on this protection as part of any financial plan.

My strongest advice is this: treat the exemption like a financial account. Check it once a year. If you rent a room, change your title, move to a trust, or go through a divorce, notify your county property appraiser immediately. The retroactive penalties for unreported changes are not small. Proactive notification is the cheapest insurance you will ever buy.

— Chuck Barnes

How Platinumcapitalfinancial helps Florida homeowners with home financing

Buying or refinancing a home in Florida involves more than just the purchase price. Understanding how the homestead exemption affects your property taxes can change your monthly budget calculations significantly.

Platinumcapitalfinancial works with Florida homeowners and buyers across Collier County and beyond to find home loan options that fit their financial picture. Whether you are purchasing your first primary residence and planning to file for the exemption, or refinancing an existing home to take advantage of lower rates, the team at Platinumcapitalfinancial can walk you through loan structures that align with your goals. Reach out to Platinumcapitalfinancial to get started with a Florida mortgage broker who understands the local market.

FAQ

What is the Florida homestead exemption in simple terms?

The Florida homestead exemption is a property tax benefit that reduces your home’s assessed value by up to $50,000, lowering your annual tax bill. It applies only to your primary residence in Florida.

When is the deadline to apply for the Florida homestead exemption?

The filing deadline is march 1 of the tax year. You must file Form DR-501 with your county property appraiser and meet the january 1 residency requirement.

Can you lose the Florida homestead exemption?

Yes. Renting your home for more than 30 days per year, selling the property, or failing to report ownership changes can all result in losing the exemption and facing retroactive tax penalties.

What is the Save Our Homes cap and how does it work?

The Save Our Homes cap limits annual increases in your property’s assessed value to 3% or the Consumer Price Index, whichever is lower. It activates automatically after your homestead exemption is approved.

Does the Florida homestead exemption protect against all creditors?

No. The exemption protects against most civil judgment creditors, but it does not shield your home from IRS liens, mortgage lenders, property tax liens, or mechanic’s liens.

Recommended

- Florida homebuyer advantages: essential tips for first-time buyers

- Florida homebuyer grants: your guide to down payment help

- Florida Home Loan Approval Workflow: 2026 Guide

- How to Apply for a Mortgage in Florida: 2026 Guide

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)