Business

What Changes in the Approval Process When Naples Buyers Move From Conforming to Jumbo

In Naples, many buyers structure their home purchase around conforming loan limits long before they sign a contract. This decision is often framed as a rate choice or a qualification issue, but in practice it reflects a deeper understanding of how mortgage approvals function once a loan crosses certain thresholds. Buyers with strong income and assets frequently choose to stay within conforming limits even when they could qualify for a larger loan.

The reason is not fear of rejection or lack of access to jumbo financing. It is the recognition that the approval process itself changes once a loan moves outside standardized frameworks. Understanding those changes requires stepping back from surface comparisons and examining how lenders evaluate risk, documentation, and liquidity under different loan categories.

This analysis focuses on what actually changes in the approval process when Naples buyers move from conforming to jumbo loans and why that change influences borrower behavior.

Why conforming loan limits matter in practice

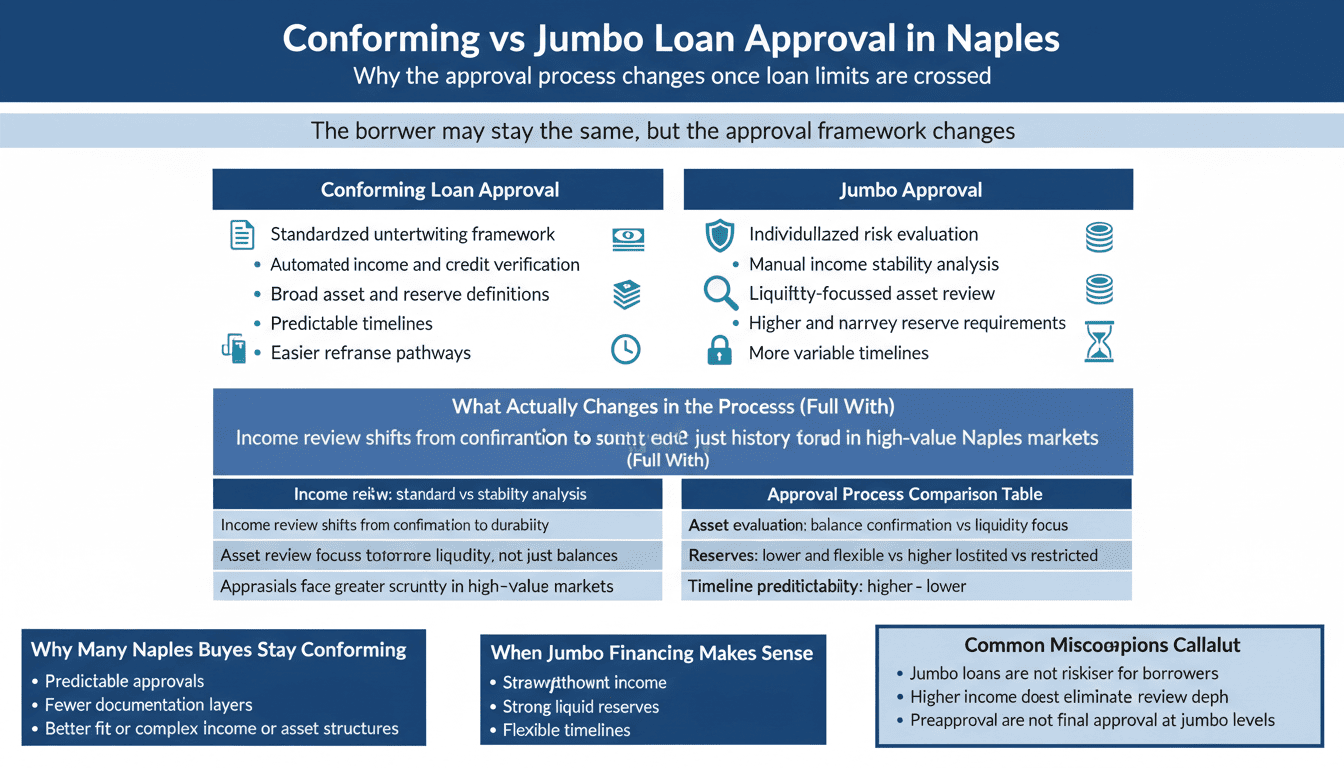

Conforming loans are designed to operate within a uniform approval system. Income documentation, asset verification, credit review, and appraisal standards follow established guidelines that lenders apply consistently. This structure allows approvals to rely heavily on automated systems and standardized tolerances.

When a loan exceeds conforming limits, it no longer fits entirely within that standardized system. The loan becomes subject to additional internal review because the lender is assuming a different type of exposure. The borrower may remain the same, but the loan is no longer treated as a standardized product.

This distinction explains why loan limits act as a practical boundary for many buyers. Staying within conforming limits keeps the approval process predictable and efficient.

Income evaluation becomes analytical rather than confirmatory

For conforming loans, income review is largely about confirmation. The lender verifies that income meets ratio requirements using accepted documentation such as pay stubs, tax returns, or standardized business income calculations. Once validated, the review typically ends.

In jumbo approvals, income is examined with greater depth. Lenders assess not only whether income qualifies but also how stable and repeatable it is under different conditions. Variable income, self employment earnings, and investment derived income receive closer scrutiny.

In Naples, where many buyers are business owners, retirees, or individuals with complex income structures, this shift matters. The approval process moves from checking boxes to evaluating durability.

Asset review shifts toward liquidity analysis

Conforming loan asset review focuses on verifying funds needed for closing and required reserves. Once balances are documented and acceptable, the review is largely complete.

Jumbo loans introduce a different lens. Lenders examine asset composition, liquidity, and accessibility. Large balances held in brokerage accounts, retirement funds, or trusts may be evaluated differently based on withdrawal restrictions and market sensitivity.

This change is particularly relevant in Naples, where buyers often hold significant net worth outside of traditional cash accounts. The approval process seeks to understand how those assets function during stress scenarios, not just their current value.

Reserve requirements increase and narrow

Conforming loans typically require limited reserves, often calculated as a few months of the full housing payment. These reserves are defined broadly and include a wide range of acceptable assets.

Jumbo loans generally require more reserves and apply stricter definitions. Lenders may require 6 to 12 months of housing payments held in specific asset types. Certain assets may be discounted or excluded altogether.

For buyers transitioning from conforming to jumbo financing, this is one of the most common friction points. The requirement is not about wealth level. It is about liquidity reliability.

Credit evaluation becomes more conservative

Credit review under conforming guidelines relies heavily on automated underwriting systems. Credit scores, payment history, and utilization are assessed within standardized tolerances.

In jumbo approvals, credit history is reviewed more manually. Lenders place greater emphasis on depth, consistency, and recent behavior. Isolated late payments, high utilization, or recent credit activity may prompt additional review even when scores are strong.

This conservative approach reflects the lender’s need to reduce uncertainty on larger loan balances rather than a judgment about borrower quality.

Appraisal review reflects market depth concerns

Conforming appraisals benefit from broad comparable data and standardized review processes. The goal is to confirm value within an established market framework.

Jumbo appraisals often face additional scrutiny, particularly in higher priced segments of Naples where comparable sales are fewer. Lenders may require additional appraisal review or more conservative valuation assumptions.

This step can extend timelines and introduce variability that buyers may not experience at the conforming level.

Documentation volume and timelines change

The conforming loan process is designed for speed and consistency. Once core documentation is submitted, approvals often progress with minimal additional requests.

Jumbo loans are reviewed in layers. Manual underwriting, secondary reviews, and internal risk assessments are more common. Additional documentation requests may appear later in the process as deeper analysis occurs.

This difference explains why buyers accustomed to conforming transactions often perceive jumbo approvals as slower even when no issues exist.

Approval process comparison in practical terms

This comparison highlights that the change is procedural rather than personal.

Why many Naples buyers stay within conforming limits

Buyers who understand these approval mechanics sometimes choose to increase down payments or adjust purchase structures to remain within conforming limits. This decision is not about avoiding jumbo loans entirely. It is about aligning the transaction with a simpler approval framework.

For buyers with complex income or asset structures, the predictability of conforming approvals can outweigh the benefits of higher leverage. For others, the choice reflects timing considerations or documentation preferences.

The key point is that staying conforming is often a strategic choice rather than a constraint.

When moving to jumbo is appropriate

Jumbo financing can be well suited for buyers with straightforward income, liquid asset profiles, and flexible timelines. Retirees with documented asset based income and buyers with diversified liquid holdings often navigate jumbo approvals smoothly.

The transition becomes easier when documentation is prepared early and expectations align with the review process.

Common misconceptions clarified

Some buyers assume jumbo loans are inherently riskier for borrowers. In reality, the increased scrutiny reflects lender exposure, not borrower instability.

Others believe higher income guarantees easier jumbo approval. Complexity, not income level, usually drives review depth.

Another misconception is that preapproval guarantees final approval. At the jumbo level, full approval often reveals requirements not visible early in the process.

Frequently asked questions

Does moving to a jumbo loan change interest rate treatment

Rates are influenced by market conditions and lender appetite, but approval mechanics operate independently of rate pricing.

Can a buyer switch back to conforming during underwriting

Yes, if the loan amount is reduced below limits through price adjustment or increased down payment.

Are jumbo loans harder to qualify for

They are more detailed to qualify for, not necessarily more difficult for prepared borrowers.

Why do jumbo approvals feel unpredictable

They involve more manual review and individualized analysis.

Should buyers avoid jumbo loans when possible

The decision should reflect documentation comfort, liquidity structure, and transaction timeline.

Grounded concluding perspective

When Naples buyers move from conforming to jumbo loans, the approval process changes because the loan exits a standardized system and enters a more individualized risk evaluation framework. The borrower does not become riskier. The loan becomes less uniform.

Buyers who understand these mechanics can make informed choices about loan structure, timing, and documentation. In many cases, the decision to remain within conforming limits reflects a preference for predictability rather than a limitation in qualification.

Understanding how approvals function at different loan levels supports better planning and reduces friction throughout the transaction.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)