Business

USDA vs VA Loans in Naples Two Zero Down Options With Very Different Rules

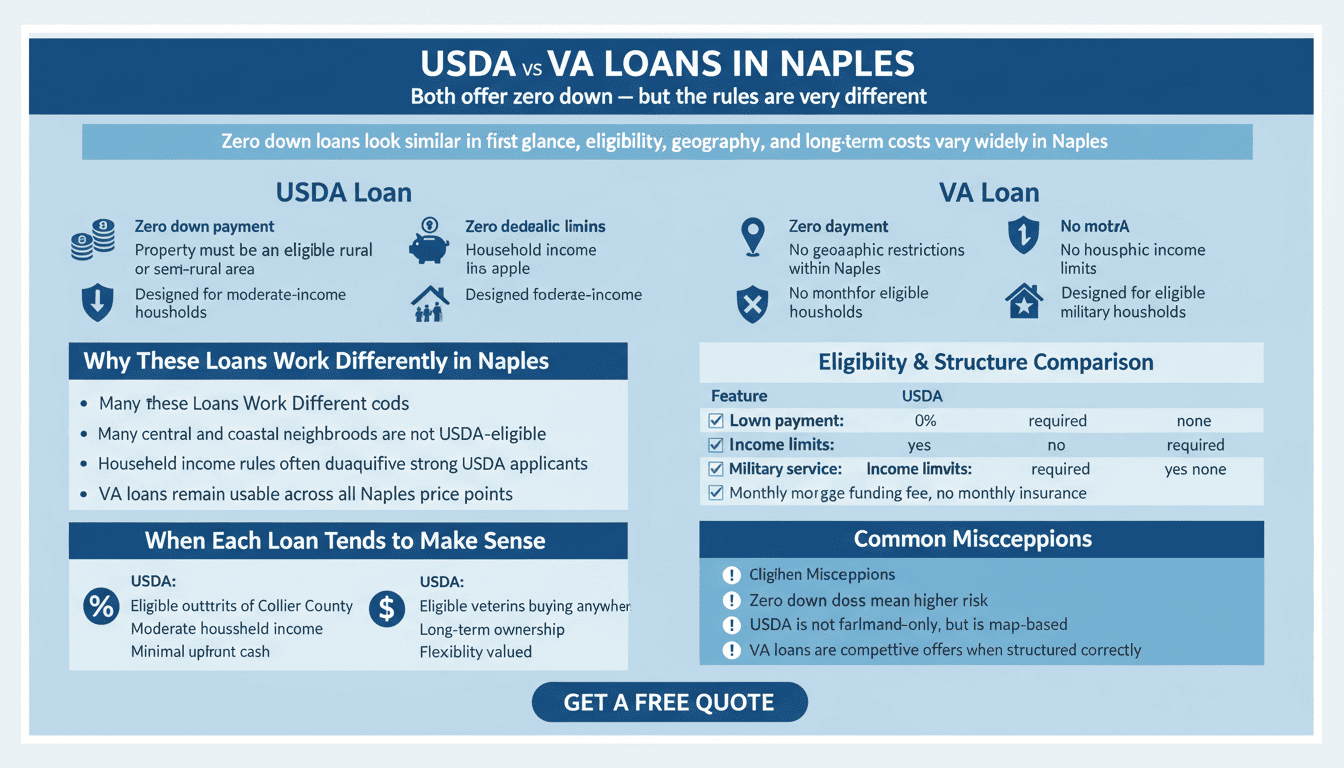

In Naples, zero down mortgage options attract buyers who are focused on preserving cash rather than stretching monthly budgets. Many households relocating to Florida, veterans transitioning to civilian life, or first time buyers entering the market notice USDA and VA loans because both allow home purchases without a down payment. At a glance, the programs appear similar. In practice, they operate very differently.

The confusion comes from focusing on what these loans have in common instead of what separates them. In Naples, where property values change rapidly by neighborhood and household income structures vary widely, those differences directly affect eligibility, approval timelines, and long term affordability. Understanding how USDA and VA loans work in real conditions is more important than simply knowing they are zero down.

The purpose behind each program shapes the rules

USDA loans were created to support homeownership in designated rural and semi rural areas for moderate income households. The program prioritizes location and household income over individual borrower profile. Eligibility depends on where the property is located and how much income the entire household earns, including adults who may not be on the loan.

VA loans were created to support military households by reducing long term borrowing costs and providing stability after service. Eligibility is tied to service history rather than income limits or property geography. This difference in mission explains why VA loans function with fewer location restrictions and more flexibility in higher cost markets like Naples.

How Naples geography limits USDA access

Naples challenges many assumptions about USDA loans. While Florida includes many USDA eligible areas, most central and coastal Naples neighborhoods do not qualify due to population density and development patterns. Eligibility is determined at the address level, not by city name, which means small boundary changes can make or break eligibility.

Even when a property qualifies geographically, household income limits apply. USDA counts income from all adults living in the home, regardless of whether they are borrowers. In Naples, where households may include retirees, working family members, or combined income arrangements, this rule alone often disqualifies otherwise strong applicants.

Why VA loans operate differently in Naples

VA loans do not impose geographic limits. Eligible borrowers can use VA financing anywhere in Naples as long as the property meets appraisal and safety standards. There are no household income caps imposed by the program itself, although lenders still assess debt obligations and residual income to ensure sustainability.

This structure gives VA borrowers significantly more flexibility in Naples. Higher priced neighborhoods, central locations, and properties near employment or medical centers remain accessible without the layering of income restrictions tied to USDA loans.

Eligibility and structural differences that matter

Seen together, these differences explain why USDA and VA loans should not be treated as interchangeable tools even though both offer zero down financing.

Income treatment changes approval outcomes

USDA income calculations surprise many borrowers. A non borrowing spouse, adult child, or co resident relative can push household income over the limit even when the primary borrower’s income appears modest. This creates denial scenarios that feel counterintuitive to applicants.

VA loans assess income differently. The focus is on residual income, meaning how much money remains after housing and major obligations are paid. This framework often benefits borrowers with stable income streams, pensions, or disability compensation, which are common among military households relocating to Florida.

Long term cost structure differences

USDA loans include an upfront guarantee fee and an annual fee that functions similarly to mortgage insurance. The annual fee remains for the life of the loan unless the borrower refinances. Over long ownership periods, this ongoing cost becomes meaningful even though it appears small monthly.

VA loans charge an upfront funding fee that can be financed into the loan. In exchange, there is no monthly mortgage insurance. For borrowers who plan to remain in the home long term, this structure often results in lower total borrowing costs despite the larger upfront fee.

This is why evaluating only upfront fees leads to incomplete conclusions.

USDA vs conventional loans in Naples

When comparing USDA vs conventional loans, the primary difference is not interest rate. It is access and structure. Conventional loans allow low down payments but require private mortgage insurance until equity is established. That insurance can eventually be removed.

USDA loans reduce upfront cash requirements but lock in ongoing insurance costs. In Naples, where prices are higher, many borrowers exceed USDA income limits before they ever compare program costs. For those who qualify, the choice often comes down to short term affordability versus long term efficiency.

Borrower protections and risk considerations

VA loans include some of the strongest borrower protections available. These include limits on closing costs, no prepayment penalties, and more flexible loss mitigation options during hardship. In Florida markets where insurance and taxes fluctuate, these protections carry practical value.

USDA loans also include borrower protections but operate within stricter compliance rules. Income recertification and program oversight reduce flexibility over time. Borrowers should view USDA as structured assistance rather than an adaptable financing tool.

Common misconceptions addressed clearly

Zero down does not mean higher default risk. Payment sustainability depends on income stability and total housing cost, not down payment size alone.

USDA loans are not limited to farmland, but they are limited by map boundaries.

VA loans are not slower or weaker offers when structured properly, even in competitive Naples markets.

When USDA loans tend to make sense in Naples

USDA loans tend to align best with moderate income households purchasing in eligible outskirts of Collier County where prices are lower and household income falls within limits. They work well for buyers prioritizing minimal upfront cash and stable employment.

They are less effective for higher income households or buyers seeking central or coastal Naples locations.

When VA loans tend to make sense

VA loans often provide the most flexibility for eligible borrowers purchasing anywhere in Naples. They offer long term cost efficiency, strong protections, and fewer structural barriers.

For veterans planning to stay in the home long term, VA loans frequently deliver the most stable financial outcome.

Frequently asked questions

Can I qualify for both USDA and VA loans

Some borrowers may qualify for both, but USDA eligibility depends on property location and household income.

Are USDA loans harder to get than VA loans

They are harder geographically and income wise. VA loans are harder only in terms of service eligibility.

Do these loans allow rental or second homes

No. Both programs require owner occupancy.

Which loan is cheaper long term

VA loans are often cheaper long term due to the absence of monthly mortgage insurance.

Can either loan be refinanced later

Yes, subject to credit, equity, and market conditions.

Grounded concluding perspective

In Naples, USDA and VA loans share a zero down feature but diverge sharply in how they handle income, geography, and long term cost. Treating them as equivalent options leads to confusion and missed opportunities.

Borrowers who understand the intent behind each program and how those rules interact with Florida housing realities make stronger, more confident decisions. Zero down is only the starting point. Structure determines the outcome.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)