Business

Jumbo vs Conventional Home Loans: How Conforming Thresholds Influence Rates and Approval

For many home buyers, the difference between a conventional loan and a jumbo loan becomes clear only after an offer is made. Buyers often focus on home price, down payment, and interest rate, but the loan size itself can quietly determine which financing category applies. This is where the jumbo vs conventional loan decision begins to matter.

The dividing line between these loan types is the conforming loan threshold. Staying under that limit often means lower rates and easier approval. Crossing it changes how lenders price risk and evaluate borrowers. Understanding jumbo vs conforming loan differences helps buyers plan smarter, avoid surprises, and choose the loan structure that fits their long term goals.

What defines a conventional and a jumbo loan

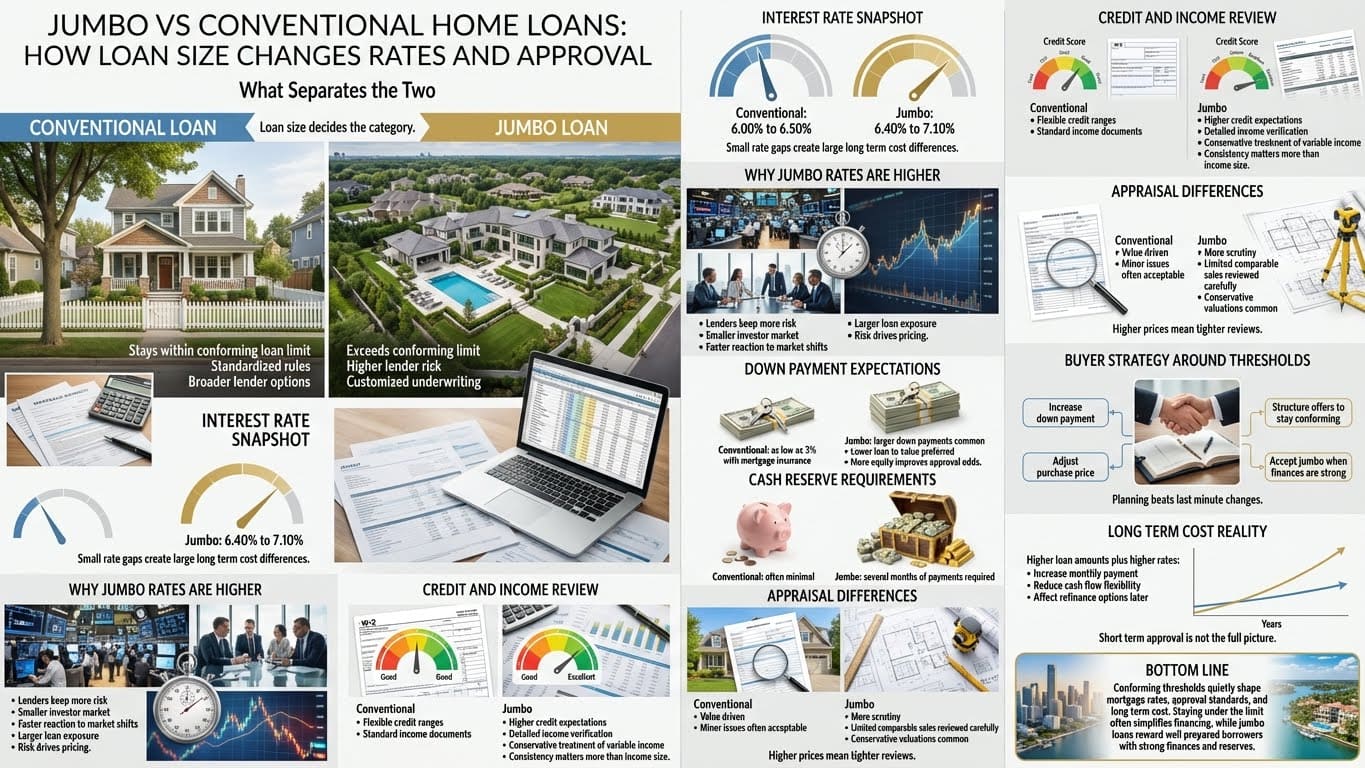

A conventional loan is a mortgage that falls within the conforming loan limit set annually. Loans at or below this threshold are eligible for purchase by major mortgage investors, which helps standardize pricing and guidelines.

A jumbo loan is any mortgage that exceeds the conforming limit. Because these loans cannot be sold in the same way, lenders keep more risk on their balance sheets. That difference shapes rates, approval standards, and borrower expectations.

Why conforming thresholds exist

Conforming thresholds are designed to balance access to credit with market stability. They ensure that standard loan programs serve typical housing needs, while higher priced homes use financing that reflects greater risk.

For buyers, the threshold creates two distinct paths:

- Conforming conventional loans with standardized rules

- Jumbo loans with customized underwriting

Understanding which side of the threshold a purchase falls on is essential before choosing a loan strategy.

How loan size influences interest rates

Interest rate differences are one of the most noticeable outcomes of crossing the conforming limit.

Typical jumbo vs conventional loan rates

The difference may appear small at first glance, but over time it can significantly affect total interest paid.

Why jumbo loan rates are often higher

Several factors explain why jumbo vs conventional loan rates differ.

Higher lender exposure

Conforming loans benefit from a broad secondary market. Jumbo loans remain with the lender or are sold in smaller pools, increasing exposure to loss.

To compensate, lenders charge higher rates.

Market sensitivity

Jumbo rates respond more quickly to market shifts. While conforming rates may remain stable for longer periods, jumbo pricing can change faster based on investor demand and economic data.

Borrower profile expectations

Jumbo borrowers are often expected to demonstrate stronger financial profiles. Even with excellent credit, the size of the loan itself increases perceived risk.

Approval standards: jumbo vs conventional loan

Approval differences go beyond interest rates.

Down payment requirements

Conventional loans may allow:

- Down payments as low as 3 percent

- Mortgage insurance for low down payment borrowers

Jumbo loans typically require:

- Larger down payments

- More equity at closing

- Reduced loan to value ratios

Higher equity lowers lender risk.

Credit score expectations

Conventional loans accept a wide range of credit profiles.

Jumbo loans often require:

- Higher minimum credit scores

- Strong payment history

- Limited recent credit inquiries

Even small credit issues can have greater impact.

Income documentation

Conventional loans rely on standardized income documentation.

Jumbo loans may require:

- More detailed income verification

- Longer employment history

- Business financials for self employed borrowers

- Conservative treatment of variable income

Consistency matters more than income size alone.

Cash reserve requirements

One of the most overlooked differences involves reserves.

Jumbo lenders often require:

- Several months of mortgage payments in reserves

- Verified liquid assets after closing

Conforming loans may have minimal or no reserve requirements for many borrowers.

Appraisal considerations

Appraisal standards also differ.

Conventional appraisal focus

Conventional appraisals emphasize:

- Market value

- Comparable sales

- General property condition

Minor repairs are often negotiable.

Jumbo appraisal scrutiny

Jumbo appraisals may include:

- Additional comparable analysis

- Review of market volatility

- Conservative value conclusions

In higher price ranges, limited comparable sales can complicate valuation.

How thresholds influence buyer behavior

Conforming limits shape how buyers approach pricing and negotiation.

Structuring offers to stay conforming

Some buyers:

- Increase down payment to reduce loan size

- Adjust purchase price targets

- Avoid escalation clauses

- Negotiate seller credits strategically

Staying under the threshold can simplify financing.

When crossing into jumbo makes sense

Not all buyers should avoid jumbo loans.

Jumbo financing may be appropriate when:

- Income is strong and stable

- Cash reserves are ample

- Long term ownership is planned

- Property value justifies the price

- Rate differences are manageable

The key is preparation rather than avoidance.

Long term cost comparison

Short term rate differences do not tell the full story.

Monthly payment comparison example

Higher payments affect cash flow and long term budgeting.

Refinancing considerations

Loan category also affects refinancing options.

Conforming loans:

- Offer broader refinance programs

- Have more lender competition

- Often allow easier rate reductions

Jumbo loans:

- Have fewer refinance options

- Depend more on lender appetite

- May require strong market conditions

Planning for refinancing is part of loan selection.

Common buyer mistakes around thresholds

Buyers often underestimate:

- How close they are to the limit

- That loan amount differs from purchase price

- How mortgage insurance compares to jumbo pricing

- The impact of reserves on approval

- Long term interest cost differences

Awareness reduces friction and disappointment.

How buyers should evaluate jumbo vs conventional loans

Buyers should review:

- Purchase price and loan amount scenarios

- Down payment flexibility

- Monthly payment comfort

- Reserve availability

- Time in the home

- Refinancing expectations

Looking beyond initial approval leads to better decisions.

Jumbo vs conforming loan summary

This summary highlights why thresholds matter.

Frequently asked questions

What is the main difference between jumbo and conventional loans

Loan size relative to the conforming limit.

Are jumbo loans harder to get

They require stronger financial profiles and more documentation.

Do jumbo loans always have higher rates

Often yes, but market conditions can narrow the gap.

Can I refinance a jumbo loan later

Yes, but options depend on rates and lender availability.

Is staying under the conforming limit better

It often simplifies approval and lowers costs.

Final perspective

The difference between jumbo vs conventional loans is not just a technical distinction. Conforming thresholds influence interest rates, approval standards, documentation requirements, and long term flexibility. Buyers who understand where their purchase falls relative to the limit can plan financing that aligns with both affordability and future goals.

Staying under the threshold often provides cost and approval advantages, but jumbo loans can still be a strong option for well prepared buyers. The most successful borrowers evaluate both paths carefully rather than letting loan size dictate decisions at the last minute.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)