Business

Florida first-time homebuyer mortgage guide: your roadmap

Buying your first home in Florida is one of the most exciting financial decisions you’ll ever make, but the mortgage process can stop even the most motivated buyers in their tracks. Between decoding loan types, gathering mountains of paperwork, and comparing offers from multiple lenders, it’s easy to feel like the system was designed to confuse you. The good news is that it doesn’t have to be that way. This guide walks you through the most important steps, from choosing the right loan to signing your closing documents, so you can move forward with clarity and confidence.

Table of Contents

- Understanding your mortgage options as a first-time homebuyer

- Preparing for your mortgage application: requirements and documents

- Comparing mortgage offers: how to get the best deal

- Navigating closing and next steps: from approval to move-in

- Florida homebuyer wisdom: why modeling your FHA costs matters most

- Next steps: connect with Florida mortgage experts

- Frequently asked questions

Key Takeaways

Understanding your mortgage options as a first-time homebuyer

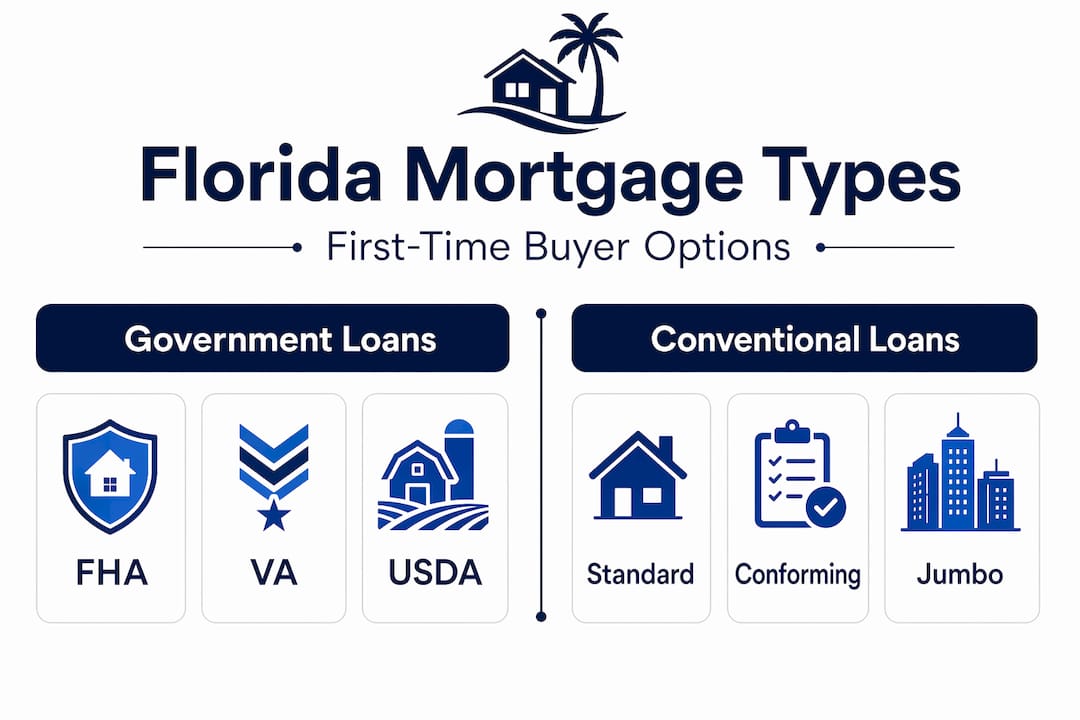

Before you start touring homes or talking to real estate agents, you need to understand what loan options are actually available to you. Florida first-time buyers generally have access to four main types of mortgages, and each one fits a different financial situation.

Conventional loans are not backed by the federal government. They typically require a credit score of at least 620 and a down payment of at least 3% to 5%. These loans are a strong option if your credit history is solid and you want to avoid the long-term cost of government-backed mortgage insurance.

FHA loans, backed by the Federal Housing Administration, are the most popular choice for first-time buyers in Florida. They allow credit scores as low as 580 with just 3.5% down, and even scores down to 500 with a 10% down payment. The tradeoff is mortgage insurance. FHA MIPs are paid in two parts: an upfront premium of 1.75% of the loan amount at closing, plus an annual premium paid monthly, and both are required regardless of your credit score.

VA loans are reserved for veterans, active duty service members, and eligible surviving spouses. They require no down payment and no private mortgage insurance, making them incredibly cost-effective for those who qualify.

USDA loans are designed for buyers purchasing in eligible rural areas of Florida. They also require no down payment and offer competitive interest rates, but there are income limits and geographic restrictions to meet.

Here’s a quick comparison to help you see the differences at a glance:

One thing many buyers miss is that Florida has specific county loan limits for FHA loans. For example, some South Florida counties have higher FHA loan limits than rural central Florida counties, which affects how much you can borrow. If you’re exploring Naples Florida mortgage options, those regional differences matter more than you might think.

Pro Tip: When evaluating an FHA loan, don’t just look at the interest rate. Factor in both the upfront MIP (1.75% of your loan amount) and the ongoing annual premium, because these costs significantly affect your true monthly payment and total loan cost.

Preparing for your mortgage application: requirements and documents

With a clear sense of the loan types available, the next step is preparing the necessary requirements and documentation. Lenders need to verify that you can actually afford the loan, and they do that through a detailed review of your financial profile.

Here are the key documents you will typically need to gather:

- Proof of income: Two years of W-2s, recent pay stubs (usually 30 days), and federal tax returns

- Employment verification: Contact information for your employer or, if self-employed, two years of business tax returns and a year-to-date profit and loss statement

- Credit information: Lenders will pull your credit report, but you should review it yourself first for errors

- Asset statements: Two to three months of bank statements for checking, savings, and any investment accounts

- Debt disclosures: A complete list of recurring monthly debts including car loans, student loans, and credit card minimums

- Identification: Government-issued photo ID and your Social Security number

- Residency documentation: Proof of Florida residency if required by state assistance programs

Here’s how lenders use each document type:

Follow these steps to prepare your documents efficiently:

- Pull your free credit reports from all three bureaus and dispute any errors at least 60 days before applying.

- Gather two full years of tax returns and W-2s from your records or request transcripts from the IRS.

- Print or download 60 to 90 days of bank and investment account statements.

- Create a running list of all monthly debts with balances and minimum payments.

- Organize everything in a dedicated folder (digital or physical) so you can hand it to any lender quickly.

Pro Tip: Your FHA MIP duration is directly tied to your down payment size. The annual premium duration depends on down payment, meaning if you put 10% or more down, you only pay annual MIP for 11 years. If you put down less than 10%, you pay annual MIP for the entire life of the loan. Before finalizing your down payment amount, model both scenarios with your lender to understand the true cost difference over time.

Comparing mortgage offers: how to get the best deal

Once your documents are ready, it’s time to shop for the best mortgage deal by comparing offers from multiple lenders. Many first-time buyers make the mistake of going with the first lender they talk to, which can cost them thousands over the life of the loan.

The most important tool in this process is the Loan Estimate. When you formally apply with a lender, they are required by federal law to provide a standardized Loan Estimate within three business days. This three-page document gives you an apples-to-apples view of what each lender is actually offering, so you can compare clearly without being misled by verbal quotes.

Getting at least three Loan Estimates is widely recommended because it reveals how much variation there can be between lenders, even on the same loan type. In some cases, the difference in total costs between the best and worst offer can exceed $10,000 over the life of a 30-year mortgage.

Here’s what to focus on when reviewing each Loan Estimate:

- Interest rate vs. APR: The interest rate is your base cost. The annual percentage rate (APR) includes fees and gives you the true cost of borrowing.

- Origination charges: These are lender fees for processing your loan. Some lenders charge 1% or more of the loan amount; others charge much less.

- Discount points: Some lenders advertise low rates but charge points upfront to achieve them. One point equals 1% of your loan amount paid at closing to lower your rate.

- Closing costs: These include title insurance, appraisal fees, prepaid interest, and government recording fees. Florida closing costs typically run between 2% and 5% of the purchase price.

- Estimated monthly payment: Make sure you understand what's included, some estimates bundle taxes and insurance and some don't.

“The Loan Estimate is your single best tool for comparing mortgage offers fairly. Every lender is required to use the same format, so side-by-side comparison becomes straightforward.”

You can also use the Loan Estimate comparison process to negotiate. If Lender A offers a better rate but Lender B has lower fees, you can share that information and ask each lender to sharpen their pencil. This kind of leverage is only possible when you have multiple estimates in hand.

Pro Tip: Apply with all your chosen lenders within a 14 to 45 day window. Credit bureaus typically treat multiple mortgage inquiries during this period as a single hard pull, which minimizes the impact on your credit score.

Navigating closing and next steps: from approval to move-in

Having compared offers and chosen your mortgage, understanding the closing process is critical to avoid mistakes and ensure a smooth transition into your new Florida home.

Here are the key steps from mortgage approval to closing day:

- Conditional approval: Your lender approves the loan pending verification of specific conditions, such as a home appraisal or updated pay stubs.

- Home appraisal: The lender orders an independent appraisal to confirm the home's value supports the loan amount.

- Underwriting review: The underwriter examines all your documents, the appraisal, and the property details. Respond to any requests for additional information promptly.

- Clear to close: Once underwriting is complete and all conditions are met, you receive a "clear to close" notification.

- Closing disclosure review: At least three business days before closing, you'll receive a Closing Disclosure. Compare it line by line with your original Loan Estimate.

- Final walkthrough: Walk through the home one last time to confirm it's in the agreed-upon condition.

- Closing day: You'll sign all documents, pay your closing costs and down payment, and receive the keys.

Common pitfalls to avoid during the closing process:

- Making large purchases or opening new credit accounts before closing, as this can change your debt-to-income ratio and potentially void your approval

- Switching jobs after your loan is approved, which can trigger a re-verification of employment and delay closing

- Wiring closing funds without verifying the account details directly with your title company, since wire fraud is a real and growing threat

- Skipping a thorough review of the Closing Disclosure before signing

As the first-time homebuyer checklist guide reminds us, getting at least three official Loan Estimates upfront means you’ll already have a solid benchmark to spot any unexpected changes in your final closing costs. If numbers shift, ask questions immediately.

Florida homebuyer wisdom: why modeling your FHA costs matters most

Here’s something most mortgage guides won’t tell you: the difference between a smart FHA loan decision and a costly one often comes down to a single number, your down payment percentage, and whether it clears the 10% threshold.

We’ve worked with Florida buyers who scraped together a 3.5% down payment and celebrated getting into a home quickly, only to realize years later that they committed to paying annual MIP for the full life of their loan. That’s potentially 30 years of extra monthly costs that quietly drain thousands of dollars from their household budget. Modeling both upfront MIP and annual MIP duration before signing anything is one of the most financially impactful things a first-time buyer can do.

The uncomfortable truth is that lenders don’t always walk you through this scenario proactively. They’re focused on getting you qualified. Your job is to ask the harder questions.

Mistakes we see Florida first-time buyers make repeatedly:

- Assuming FHA is always cheaper than conventional without running total cost comparisons

- Not asking lenders to model MIP scenarios for different down payment amounts

- Focusing only on the monthly payment and ignoring total loan cost over 10 or 20 years

- Overlooking the opportunity to refinance out of an FHA loan once equity builds, which could eliminate the annual MIP entirely

Our perspective: treat your FHA loan decision like a business case. Build out two or three scenarios. What does it cost if you put 3.5% down? What if you wait six months and save for 10%? What if you go conventional with 5% down and accept PMI that automatically cancels at 20% equity? The answers will surprise you, and they’ll lead you to a smarter decision.

Pro Tip: Ask your lender to provide a side-by-side cost comparison showing total MIP paid under 3.5%, 5%, and 10% down payment scenarios before you commit to any FHA loan.

Next steps: connect with Florida mortgage experts

You now have a solid foundation for navigating the Florida first-time homebuyer mortgage process, from choosing the right loan type to avoiding closing day mistakes. But reading about mortgages and actually securing the best one for your situation are two different things.

Working with an experienced Florida mortgage broker means you get personalized guidance on loan options, help preparing your application, and expert support in comparing real lender offers. At Platinum Capital Financial, we specialize in helping Florida buyers, including first-time buyers across Naples, Southwest Florida, and beyond, find mortgage solutions that fit their financial goals. Whether you’re still exploring your options or ready to submit a Naples Florida mortgage application, our team is ready to walk you through every step with clarity and no pressure.

Frequently asked questions

How much do I need for a down payment on an FHA loan in Florida?

The minimum down payment for an FHA loan is 3.5%, but putting at least 10% down is a smart move because it limits your annual MIP to 11 years instead of the full loan term.

Do I have to pay mortgage insurance on a conventional loan?

Mortgage insurance is required on conventional loans if your down payment is less than 20%, but unlike FHA loans, it can be canceled automatically once your equity reaches 20% of the home’s original value.

What should I look out for during closing?

Review your Closing Disclosure carefully against your original Loan Estimate and confirm that all fees and costs match what was agreed upon before you sign anything. As the first-time homebuyer checklist advises, understanding closing costs in advance is essential for avoiding unwanted surprises.

How can I compare mortgage offers effectively?

Request standardized Loan Estimates from lenders at no fewer than three different institutions so you can compare interest rates, fees, and closing costs side-by-side using the same document format.

Recommended

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)