Business

FHA 203k Loan Reality Check: Today’s Rates, Approval Guidelines, Qualification Rules, and Lender Limits

Buying a home that needs repairs can feel overwhelming, especially when renovation costs are added on top of the purchase price. This is where FHA 203k loans come into the conversation. These loans are designed to help buyers purchase or refinance a property and include renovation costs in a single mortgage.

Despite their usefulness, FHA 203k loans are often misunderstood. Many borrowers focus only on rates and miss the approval rules, lender limits, and qualification details that determine whether the loan actually works for their situation. Understanding what is a 203k loan, how fha 203k loan rates today compare to standard FHA loans, and what lenders truly require can help buyers avoid delays and surprises.

This explanation provides a clear reality check on how FHA 203k loans work in today’s market.

What is a 203k loan

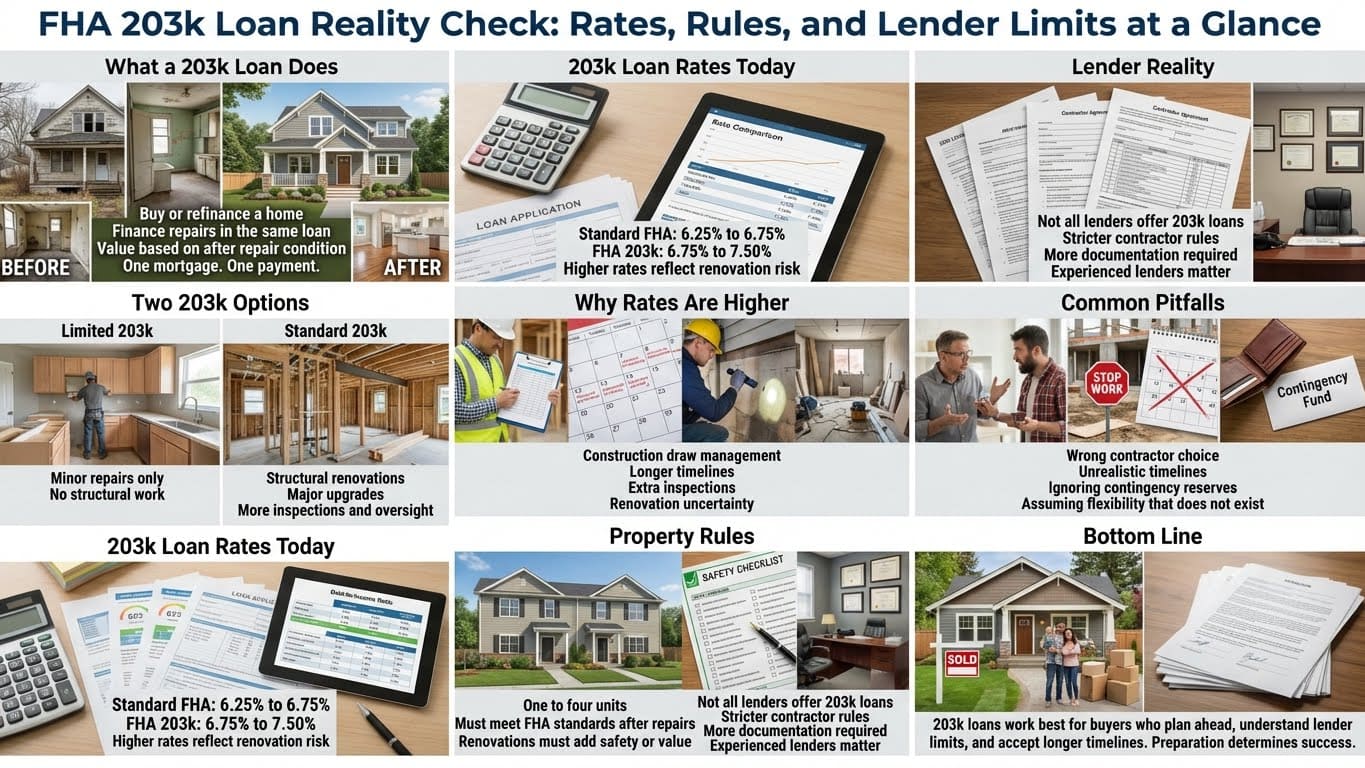

An FHA 203k loan is a government backed mortgage that allows borrowers to finance both the purchase or refinance of a home and the cost of renovations in one loan. Instead of taking out a separate construction loan or personal loan, everything is rolled into a single FHA mortgage.

People often ask what’s 203k loan or what is a 203k loan because it works differently from traditional financing. The loan amount is based on the home’s value after repairs are completed, not just the current condition.

Types of FHA 203k loans

There are two main versions of the FHA 203k program.

Limited 203k loan

This option is designed for minor repairs and improvements.

Typical uses include:

- Flooring replacement

- Painting

- Appliance upgrades

- Roof repairs without structural changes

There is a cap on renovation costs, and structural changes are not allowed.

Standard 203k loan

This option is used for major renovations.

It allows:

- Structural repairs

- Room additions

- Foundation work

- Plumbing and electrical upgrades

Standard 203k loans require more documentation and oversight.

203k loan rates today

Many buyers ask about 203k loan rates and how they compare to standard FHA mortgages. FHA 203k loans typically carry slightly higher interest rates due to the added complexity and risk involved.

Actual fha 203k loan rates today depend on credit score, loan size, down payment, and market conditions. Rates can change daily.

Why 203k loan rates are higher

The rate difference exists because:

- Renovation risk is higher than move in ready homes

- Lenders manage construction draws

- Additional inspections are required

- Timelines are longer

While rates are higher, the ability to finance renovations may offset the cost compared to separate loans.

Requirements for FHA 203k loan approval

Understanding requirements for fha 203k loan approval is essential before applying.

Borrower requirements

Most lenders expect:

- Minimum credit score around 580

- Stable income history

- Acceptable debt to income ratio

- Ability to cover down payment and closing costs

Stronger credit profiles may qualify for better pricing.

Property requirements

The property must:

- Be a primary residence

- Meet FHA minimum property standards after renovation

- Be one to four units

- Have repairs that add value or safety

Investment properties are not allowed.

FHA 203k loan guidelines lenders follow

The fha 203k loan guidelines are more detailed than standard FHA loans.

Key rules include:

- Renovation work must begin shortly after closing

- Work must be completed within a set timeframe

- Funds are held in escrow and released in draws

- Inspections are required before each draw

For standard 203k loans, a HUD approved consultant is required to oversee the project.

Qualification for 203k loan

Qualification for a 203k loan is based on the after improved value of the property.

Lenders calculate:

- Purchase price or current value

- Renovation budget

- Contingency reserve

- Fees and permits

The final loan amount must fall within FHA loan limits for the county.

Debt to income and affordability

Even though renovation costs are included, lenders still review affordability carefully.

They evaluate:

- Total monthly mortgage payment

- Property taxes and insurance

- Mortgage insurance

- Existing debts

Just because renovations are financed does not mean affordability rules are relaxed.

FHA 203k loan lenders and lender limits

Not all lenders offer FHA 203k loans. This is one of the biggest obstacles borrowers face.

Why lender availability is limited

Many lenders avoid 203k loans because:

- Processing is time intensive

- Staff training is required

- Construction oversight adds risk

As a result, fha 203k loan lenders may have:

- Higher minimum credit score requirements

- Lower loan to value limits

- Stricter contractor approval rules

Working with an experienced lender reduces friction.

Contractor and renovation rules

Borrowers cannot do all work themselves.

Lenders require:

- Licensed and insured contractors

- Detailed bids and timelines

- Clear scope of work

DIY labor is usually limited and must follow lender rules.

Renovation escrow and draw process

Renovation funds are not given directly to the borrower.

The process includes:

- Funds placed in escrow at closing

- Contractor completes approved phase

- Inspection confirms work completed

- Funds released to contractor

This protects both borrower and lender but adds steps to the timeline.

Common mistakes borrowers make

Many FHA 203k loans fail due to avoidable mistakes.

Common issues include:

- Choosing contractors unfamiliar with 203k rules

- Underestimating renovation timelines

- Ignoring contingency requirements

- Assuming lender flexibility that does not exist

- Shopping for homes without lender pre review

Preparation is critical.

When a 203k loan makes sense

FHA 203k loans work best when:

- Homes need meaningful repairs

- Buyers plan long term ownership

- Renovation costs add clear value

- Inventory of move in ready homes is limited

They are less effective for cosmetic only projects with tight timelines.

Realistic expectations for timelines

203k loans take longer than standard mortgages.

Typical timelines:

- Pre approval and planning takes longer

- Closing may take additional weeks

- Renovation completion can take months

Borrowers must plan housing needs accordingly.

Working with the right guidance

Because of complexity, many buyers seek lenders who understand both FHA rules and renovation financing. Firms like Platinum Capital Advisor work with borrowers to evaluate whether a 203k loan truly fits the purchase and renovation goals before moving forward.

Later in the process, experienced advisory support helps borrowers navigate lender conditions, contractor coordination, and draw schedules without unnecessary delays. This kind of guidance can reduce stress and improve outcomes without pushing borrowers toward unsuitable financing.

Frequently asked questions

What is a 203k loan

It is an FHA loan that includes purchase or refinance plus renovation costs.

Are 203k loan rates higher

Yes. Rates are usually higher than standard FHA loans.

Can first time buyers use 203k loans

Yes. Many first time buyers qualify.

Are contractors required

Yes. Most work must be done by approved contractors.

Is the process complicated

It is more detailed than standard loans but manageable with preparation.

Final perspective

FHA 203k loans offer a powerful solution for buyers willing to take on renovation projects, but they are not simple or fast. 203k loan rates today, lender guidelines, qualification rules, and renovation oversight all influence whether the loan works as intended.

Borrowers who understand the full structure and prepare for the added complexity are far more likely to succeed. A realistic approach focused on affordability, timelines, and lender requirements helps turn a fixer upper into a long term asset rather than a financial burden.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)