Business

ARM or Fixed Rate in Florida The Answer Depends on How Long You Will Really Stay

Choosing between an adjustable rate mortgage and a fixed rate mortgage is not a theoretical exercise for Florida homebuyers. It is a practical decision shaped by how long you expect to own the property, how Florida housing markets behave, and how interest rate risk interacts with insurance costs, taxes, and migration patterns. Many borrowers approach the decision by asking which loan is cheaper today. That question alone often leads to the wrong answer.

Florida presents a unique environment. Homeownership turnover is higher than the national average due to job relocation, retirement migration, and second home usage. Property insurance volatility and tax considerations also affect long term affordability. Because of these factors, the right choice between an ARM and an FRM depends less on predicting future rates and more on honestly assessing how long you are likely to stay in the home.

The keyword arm vs frm captures the core of this decision, but the comparison only becomes useful when time horizon is placed at the center of the analysis.

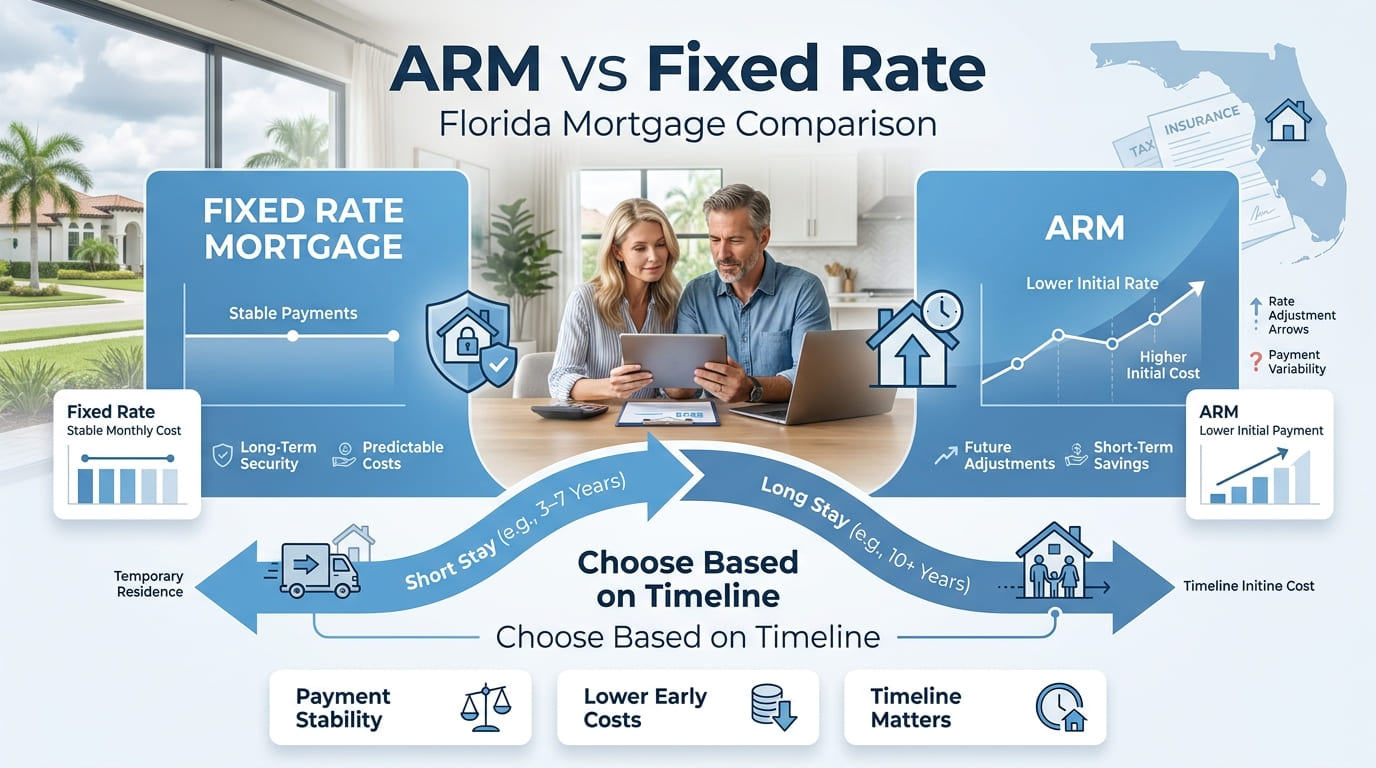

Understanding the structural difference between ARM and fixed rate mortgages

A fixed rate mortgage carries the same interest rate for the full loan term. Payments remain stable for principal and interest regardless of market rate changes. This structure transfers interest rate risk away from the borrower and onto the lender.

An adjustable rate mortgage begins with a fixed introductory period followed by periodic rate adjustments. The rate resets are tied to a published index plus a margin. Most ARMs include caps that limit how much the rate can increase at each adjustment and over the life of the loan.

The key point is not that one loan is safe and the other is risky. The real difference is when and how interest rate risk appears. With an ARM, the borrower accepts uncertainty after the fixed period ends. With a fixed rate mortgage, the borrower pays for certainty from the first payment forward.

Why Florida ownership duration matters more than rate forecasts

Florida homeowners tend to move sooner than they initially expect. Retirees may downsize. Investors may sell when rental regulations or insurance costs change. Primary residents may relocate due to employment or family needs. These patterns matter because most ARMs are designed around an initial fixed period that aligns with common ownership timelines.

If you sell or refinance before the first rate adjustment, the future variability of an ARM never materializes. In that case, the borrower benefits from a lower initial rate without experiencing adjustment risk.

If you remain in the property beyond the fixed period, the ARM becomes a variable rate loan. At that point, the decision shifts from short term savings to long term exposure.

Common ARM structures used in Florida

The most common ARM structures in Florida are 5 year, 7 year, and 10 year fixed periods followed by annual adjustments.

A 5 year ARM offers the lowest initial rate but the shortest window before adjustment. A 7 year ARM balances initial savings with a moderate fixed period. A 10 year ARM closely resembles a fixed rate loan for borrowers who expect to stay around a decade but not longer.

Understanding these structures helps clarify why the arm vs frm decision is fundamentally a timing question.

Numeric comparison using a realistic Florida purchase example

Assume a Florida home purchase price of 450000 with a loan amount of 360000 after down payment. The borrower qualifies for both loan types.

Assumptions are illustrative and not predictions.

The monthly difference between the 30 year fixed and the 7 year ARM is 149. Over 7 years that totals approximately 12516 in payment savings before any adjustment occurs.

The question becomes whether that savings justifies the uncertainty beyond year 7.

What happens if you sell before the ARM adjusts

If the borrower sells the home in year 5 or year 6, the ARM functions as a discounted fixed rate loan. There is no adjustment exposure, and the borrower keeps the full benefit of the lower rate.

In Florida, this scenario is common among relocation buyers, early retirees testing a location, and investors repositioning capital.

For these borrowers, choosing a fixed rate mortgage often means paying a premium for protection they never use.

What happens if you stay beyond the fixed period

If the borrower remains in the home past the initial fixed term, the ARM begins adjusting based on the index and margin.

For example, a 7 year ARM with a 2 percent annual cap and a 6 percent lifetime cap could adjust upward gradually rather than all at once. Even so, the payment could eventually exceed the original fixed rate option.

The risk is not just higher payments. It is payment uncertainty during periods of insurance increases, tax reassessments, or broader economic stress.

In Florida, where insurance premiums can rise sharply year to year, compounding variability can strain household budgets.

Cause and effect relationship between time horizon and loan choice

Shorter expected ownership reduces interest rate risk exposure. Longer expected ownership increases it.

The longer you stay, the more valuable payment certainty becomes. The shorter you stay, the more valuable initial rate savings become.

This is the core logic behind arm vs frm decisions, regardless of market forecasts.

How Florida specific factors influence the decision

Florida property insurance costs are volatile. Flood risk, wind coverage, and carrier exits can change total housing costs quickly. A fixed rate mortgage stabilizes one component of the payment, which may be valuable when other costs are unpredictable.

On the other hand, Florida attracts many part time residents and transitional buyers. These borrowers often overestimate how long they will keep the property. For them, ARMs frequently align better with actual behavior than stated intent.

Tax homestead benefits can also influence duration. Once established, some homeowners are more likely to stay longer due to assessment caps. In these cases, locking a fixed rate may better match long term ownership incentives.

Common misconceptions about ARMs in Florida

Many borrowers believe ARMs always become unaffordable. That is not accurate. Adjustment caps limit how quickly rates can rise, and many borrowers refinance or sell before reaching maximum adjustments.

Others assume fixed rate mortgages are always safer. In reality, paying a higher rate for decades can carry opportunity costs if the borrower exits early.

Some believe ARMs are only for high risk borrowers. In practice, ARMs are often used by high credit borrowers managing cash flow intentionally.

When a fixed rate mortgage tends to make more sense

A fixed rate mortgage generally aligns better when you expect to stay in the home long term, plan to age in place, or prioritize payment predictability above short term savings.

It also makes sense when your budget has limited flexibility or when housing costs already include volatile components such as insurance or association fees.

When an ARM tends to make more sense

An ARM often aligns better when ownership is likely to be under 7 to 10 years, when income is expected to grow, or when the borrower plans to refinance based on future life changes rather than rate movements.

It can also be appropriate when preserving cash flow matters more than locking a long term rate.

Frequently asked questions

Is an ARM risky in Florida due to hurricanes and insurance costs

The risk comes from combining adjustable payments with volatile insurance premiums. Borrowers should evaluate total payment flexibility rather than focusing only on the mortgage rate.

Can I refinance an ARM before it adjusts

Refinancing is possible but depends on credit, income, home value, and market rates at that time. It should be viewed as an option, not a guarantee.

Do ARMs adjust suddenly or gradually

Most ARMs adjust gradually due to annual and lifetime caps. The structure limits extreme payment shocks but does not eliminate variability.

Does arm vs frm choice affect resale value

Loan type does not affect resale value directly. It affects cash flow and affordability during ownership.

Are ARMs only for investors or second homes

No. Many primary residence buyers use ARMs strategically based on expected tenure.

Grounded concluding perspective

The decision between an adjustable rate mortgage and a fixed rate mortgage in Florida is less about predicting interest rates and more about understanding personal timelines. The most financially sound choice is often the one that matches how long you will realistically stay, not how long you hope to stay.

When borrowers align loan structure with actual behavior, they reduce regret and improve financial outcomes. Florida markets reward realism over optimism.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)

.svg)

.svg)

.svg)